EdTech App Marketing: User Acquisition Playbook for Learning Apps

EdTech marketing has two buyers, multiple seasons, and a trust barrier higher than any other vertical. Here is the playbook that works for K-12, test prep, and upskilling apps.

What does the Indian EdTech landscape look like in 2026?

The Indian EdTech market in 2026 is structurally bigger but emotionally smaller than its 2021 peak — the addressable audience has expanded with smartphone penetration, but parent and student willingness to trust any single brand has collapsed in the wake of the BYJU's correction. What survives is a healthier, more discerning market that rewards proof over promise.

The fundamentals are still extraordinary. India has 250M+ school-age children, 60M+ college students, and 200M+ adult learners who could materially benefit from upskilling. Smartphone penetration is approaching saturation in metros and accelerating in Tier-2/3 cities — Statista projects India will cross 1.2B smartphone users by 2027, with the majority of net-new users in non-metro markets. Those are exactly the buyers EdTech needs to reach next.

What has fundamentally changed is the trust environment. Parents who watched friends sign multi-year EdTech contracts that delivered less than promised are now slower to subscribe, faster to churn, and more responsive to outcome proof than to brand spend. AppsFlyer's State of App Marketing data on the India education category shows install-to-paid conversion windows lengthening — what used to convert in 7 days now takes 14-30 days on average, with multiple touchpoints required.

Four dynamics shape EdTech marketing in 2026 that did not apply in the previous cycle:

- Free trial → paid conversion replaced full-stack "demo class with counsellor" funnels for most categories. The counsellor-led model still works for high-ticket NEET/JEE coaching but has collapsed elsewhere.

- Vernacular content in Hindi, Tamil, Telugu, Bengali, and Marathi outperforms English by 3-5x in Tier-2/3 cities for the same categories.

- Short-form video (60-90 second explainer reels) replaced webinar-style long-form marketing.

- Parent-influencer marketing emerged as the dominant K-12 trust channel, replacing celebrity endorsements that no longer move conversion.

Across the 300+ apps in our portfolio, the EdTech apps growing profitably in 2026 share one operating discipline: they treat every install as expensive and every minute of post-install engagement as the actual product. That mindset shift — from acquisition obsession to lifecycle obsession — is what separates the survivors from the brands that scaled hard and collapsed.

What are the category economics across EdTech segments?

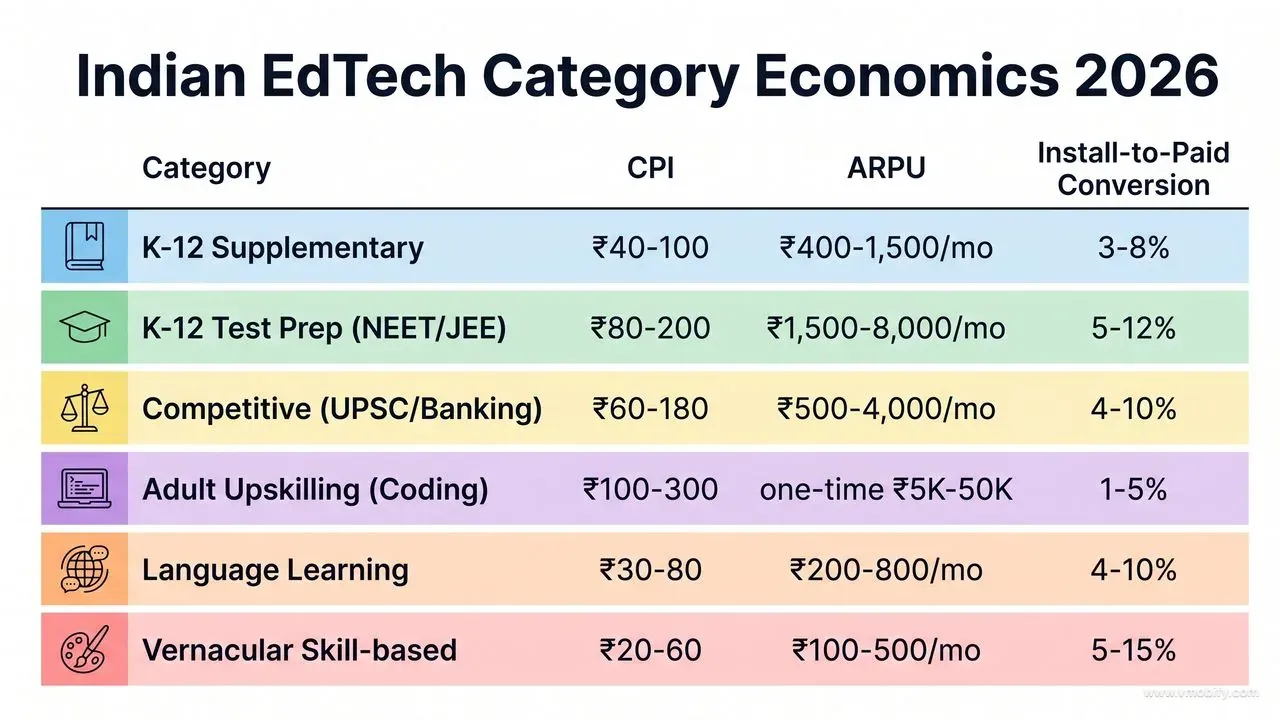

EdTech is not one category — it is at least six, each with 5-10x variance in CPI, ARPU, and conversion rates. Treating it monolithically is the single most common strategic mistake we see new entrants make. Here are the realistic 2026 benchmarks we see across our India EdTech portfolio:

- K-12 supplementary learning: CPI ₹40-100. Subscription ARPU ₹400-1500/month. Install-to-paid conversion: 3-8% in 30 days. Trial-heavy funnel; parent decides; outcome creative wins.

- K-12 test prep (NEET, JEE): CPI ₹80-200. ARPU ₹1500-8000/month. Conversion: 5-12%. High-intent search-driven traffic; counsellor-led funnels still work; teacher brand matters.

- College / competitive exams (UPSC, banking, SSC): CPI ₹60-180. ARPU ₹500-4000/month. Conversion: 4-10%. Mock-test hook converts better than free-class hook; YouTube content marketing dominant.

- Upskilling adult (coding, design, marketing): CPI ₹100-300. Course pricing ₹5K-₹50K one-time. Conversion: 1-5% install-to-enrolment. LinkedIn + YouTube long-form drives most enrolments; Meta drives top-of-funnel.

- Language learning: CPI ₹30-80. ARPU ₹200-800/month. Conversion: 4-10%. Gamified retention drives renewals; freemium-to-paid funnels dominate.

- Skill-based vernacular (cooking, fitness, music): CPI ₹20-60. ARPU ₹100-500/month. Conversion: 5-15%. Highest-volume, lowest-ticket — economics work only with strong retention.

The pattern across these numbers is consistent: lower-ticket categories live or die on retention because each subscriber must renew 6-12 times to amortise the CPI, while higher-ticket test-prep categories tolerate higher CPI because a single paid conversion recovers acquisition cost almost immediately. Picking your channel mix and creative strategy without naming your category economics first is how budgets disappear.

For deeper India CPI benchmarks across all verticals see our India app install cost guide and our vetted CPI network breakdown. AppsFlyer's Performance Index also publishes quarterly India-specific education category data worth tracking against your own numbers.

How do you solve the two-buyer problem (parent vs student)?

K-12 EdTech is the only major mobile vertical where the user and the buyer are different people, in different rooms, looking at different screens, motivated by different things. Successful marketing treats them as two separate funnels that converge inside the app.

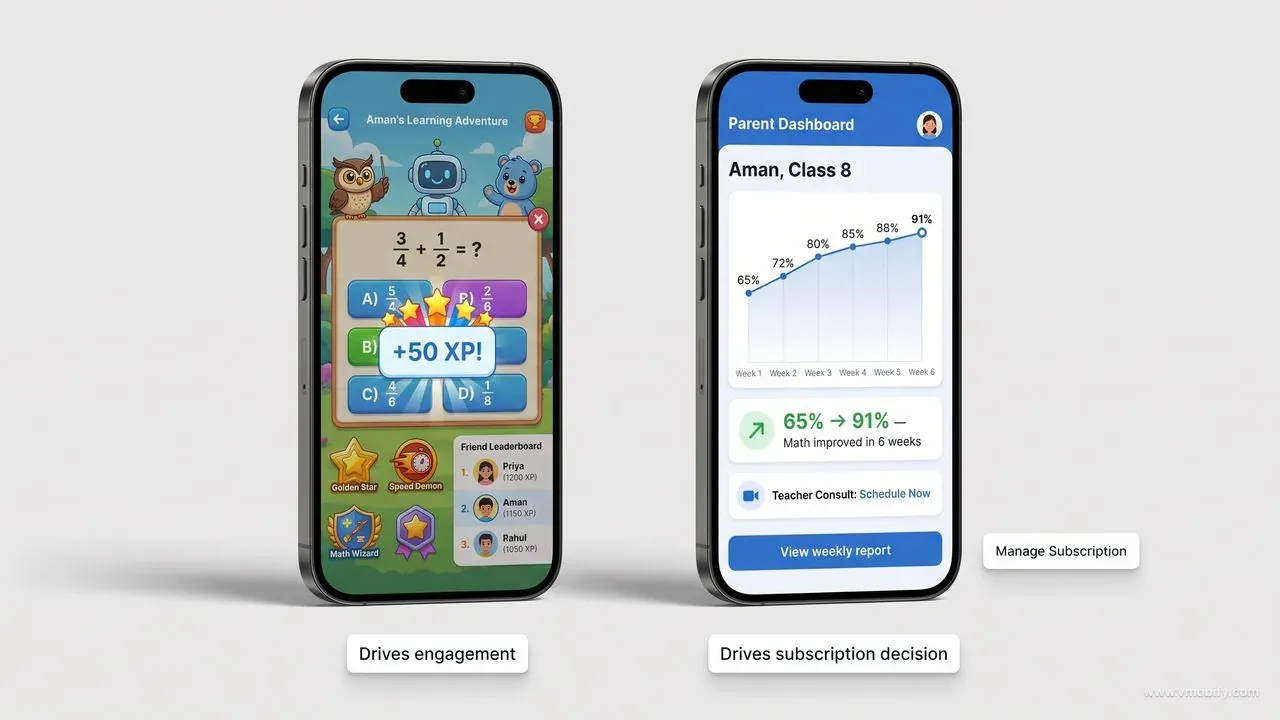

The student is the daily-active user. They care about whether the app is fun, whether their friends use it, whether they get achievement badges, whether the explanations make sense. The parent is the paying user. They care about whether the curriculum aligns with their child's school board, whether grades improve, how much screen-time is involved, and what the teacher credentials look like.

Creative split:

- Student-facing creative: Gamified visuals, characters, achievement badges, friend-leaderboards, "join 50,000 students learning" social proof. Tone is peer-to-peer, not authoritative.

- Parent-facing creative: Outcomes ("Aryan went from 65% to 92% in 6 months"), teacher credentials, structured curriculum alignment, parental controls, weekly progress reports. Tone is consultative, not playful.

Channel split:

- Parents: Facebook, Instagram (parent demographics 28-45), WhatsApp follow-up funnels, parent-influencer YouTube and Instagram content.

- Students: YouTube (kids/teens watch hours daily), Instagram Reels, game-adjacent placements, school-app cross-promotion partnerships.

The bridge that ties these funnels together lives inside the app. The cleanest funnels we have built across our EdTech portfolio do this in two stages: the student installs, completes 1-2 fun activities, and is then nudged to share progress with a parent via WhatsApp deep link. The parent receives a personalised "your child is learning X" message, taps through to a parent-mode demo, and converts in 24-48 hours. Apps that try to convert students directly without involving the parent see paid-conversion rates collapse to 1-2%; apps that bridge cleanly hit 5-8%.

The mechanics matter. Apple's In-App Events can surface parent-mode demo windows and live class slots directly in the App Store, which materially lifts the parent-side conversion rate when paired with parent-targeted Meta retargeting. Google's App Campaigns documentation similarly supports targeting the parent demographic separately for retargeting after a student install event fires.

When does EdTech seasonality peak and how do you plan for it?

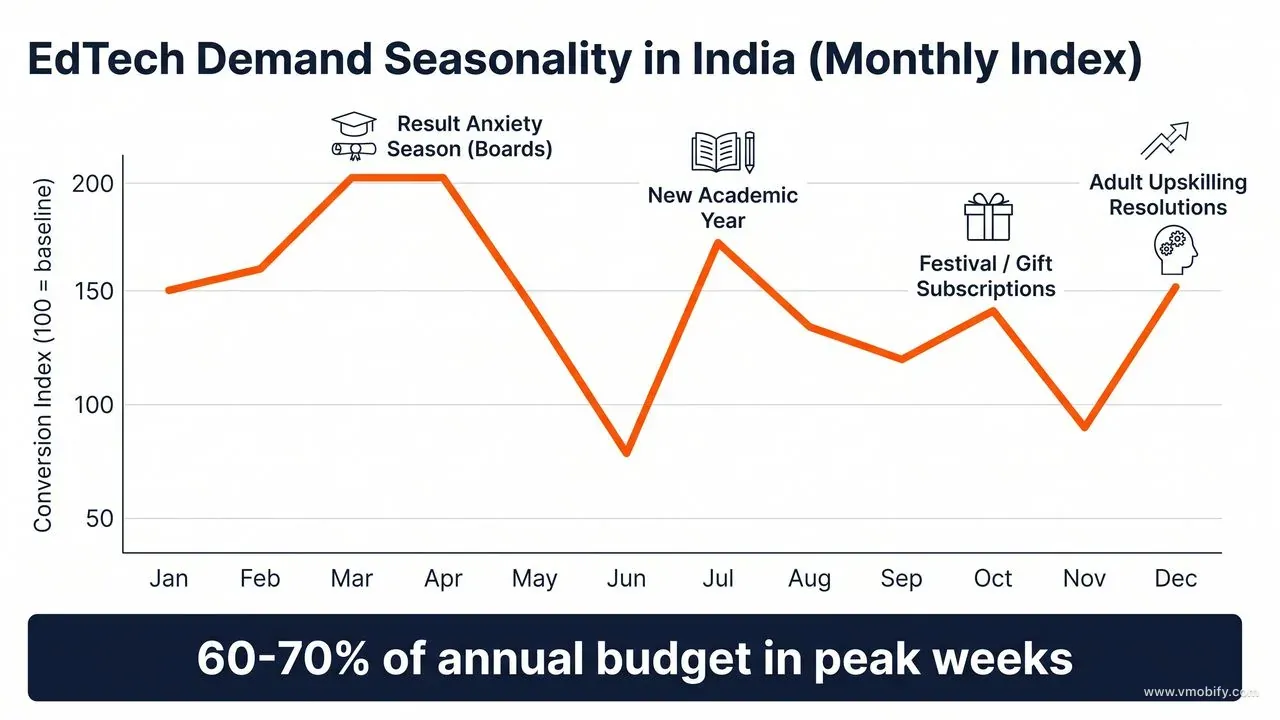

EdTech is the most seasonal vertical in Indian mobile marketing — more seasonal than ecommerce, fintech, or gaming. Planning your annual budget without modelling the calendar is the single fastest way to misallocate spend.

The five seasons that matter:

- March-May — Result-anxiety peak. Board exam results, college entrance results, semester results. Parents and students are at their most receptive to "fix this gap" messaging. K-12 and test-prep conversion rates run 2-3x annual average. CPIs rise 30-50% but conversion compensates.

- June-July — New academic year. Fresh-class enrolment, college joining, parents budgeting for the new school year. Subscription decisions made for the next 12 months. Highest-volume conversion window for K-12 subscription apps.

- August-October — Festival season. Diwali bundled offers, gift subscriptions, "back-to-school" reinforcement. Promotional creative outperforms standard creative. Ecommerce-style discount mechanics work better here than at any other time of year.

- November-December — Pre-board exam panic. K-12 board students entering final preparation. Targeted "100-day countdown" messaging converts at high rates. Test-prep category specifically benefits.

- January-February — New year resolutions. Adult upskilling, language learning, fitness-adjacent learning categories peak. "New year, new skill" creative dominates.

In our portfolio, March-July alone accounts for 50-60% of annual paid conversions for the average K-12 subscription app. That means a flat-monthly-budget allocation systematically over-spends in November-February and under-spends in March-July — destroying ROAS in both directions. The fix is straightforward: model expected category conversion rate by month, allocate budget proportionally, and pre-build creative inventory 30-45 days ahead of each peak so launches do not bottleneck on production.

One operational note: CPIs themselves rise 30-80% during peak seasons because every EdTech advertiser is bidding into the same auction. The teams that win the peak season are the teams whose creative was tested, optimised, and proven during the off-season — they show up at the auction with proven hooks and high relevance scores while competitors are still testing. Meta's Advantage+ documentation is explicit that account-level signal accumulated over months feeds peak-season auction performance — there is no shortcut.

What channel mix actually works for EdTech in India?

The right EdTech channel mix in India 2026 weights heavily toward Meta + Google for paid reach, supplements with parent-influencer for trust, and uses owned WhatsApp + SMS channels for the actual conversion close. Pure paid-only EdTech funnels rarely break even.

The realistic split we run across our EdTech portfolio:

- Meta (Facebook + Instagram) — 35-45% of paid budget. Parent targeting via age + parental status proxies, lookalikes built off existing paying customers (not installers — paying customers). Best-performing format: 30-second teacher-led reel with on-screen captions in regional language. See our Meta App Install Campaigns playbook for setup detail.

- YouTube + Google App Campaigns — 30-40%. Student-facing video, parent-facing testimonials, and crucial search-intent capture for high-intent test-prep keywords. UAC works particularly well for upskilling categories where intent search volume is high.

- Performance influencers — 10-20%. Parent-influencers (mom-bloggers, 50K-500K followers) for K-12; topic-domain influencers (engineering YouTubers for JEE, design YouTubers for upskilling) for everything else. Flat-fee plus CPI top-up structure.

- CPI Networks — 5-10%. Tier-2/3 fills, seasonal velocity bursts ahead of major peaks, defensive bursts when competitors push aggressively.

- WhatsApp + SMS owned channels — separate budget line, but critical. Lead nurture, demo class reminders, drop-off recovery. India EdTech without WhatsApp follow-up loses 40-60% of would-be conversions.

The owned-channel piece is the part most international playbooks miss. India EdTech buyers — especially Tier-2/3 parents — convert on WhatsApp, not on web checkout. The conversion path is: paid impression → app install → WhatsApp opt-in → WhatsApp demo class invite → counsellor message → payment. Apps that skip the WhatsApp middleware see install-to-paid collapse, regardless of how good their paid creative is.

For broader UA channel strategy across verticals see our user acquisition services page and our mass UA strategy guide. For sustained organic visibility that feeds your paid channels see our ASO services.

Which creatives build trust fast in EdTech?

EdTech creative has to clear a higher trust bar than any other vertical because the buyer is risking their child's education or their own career trajectory. Creative that builds trust fast outperforms aspirational brand creative by 2-3x on install-to-paid conversion in our tests.

The five creative formats that consistently win in our portfolio:

- Teacher-led explainer: A real teacher explaining a real concept in 60-90 seconds. Single highest-converting format for K-12 and test-prep. Production cost is low — phone + ring light + decent mic — but the credibility lift is enormous. Parents recognise good teaching when they see it.

- Outcome testimonials: "Aman scored 96% — here is what changed." Real names, real schools, before/after grade evidence. The more specific and verifiable, the better. Generic testimonials ("great app!") perform 3-4x worse than specific outcome testimonials.

- App-walkthrough videos: Show actual lessons, actual progress dashboards, actual doubt-resolution flows. Transparency consistently outperforms promise-heavy creative because parents have seen enough EdTech promises to be cynical about them.

- Free-content hooks: "Download our free formula sheet / mock test / lesson plan" → install → in-app nurture into paid. This funnel typically halves CPI versus direct paid-product pushes and triples install-to-paid conversion because the audience self-selects for genuine interest.

- Parent-anxiety hooks: "Worried about your child's board exam?" High CTR, but use carefully. Overdone, these creatives feel manipulative and erode brand. Best used sparingly during the March-May results-anxiety peak.

Two things to avoid: celebrity endorsements (the BYJU's-era format that no longer converts) and discount-led creative for high-ticket categories (cheapens perceived value and attracts price-shoppers who churn). The teams in our portfolio that win on creative are running 8-15 variants in market simultaneously, killing the bottom quartile every 72 hours, and reinvesting the saved spend into the top quartile. Creative discipline beats creative budget every time.

For broader creative testing protocols see our 72-hour install push guide, which covers creative volume, hook testing, and pause-replace cadence in detail. Adjust's app marketing resources publish useful aggregated benchmarks on creative refresh cadence by vertical.

How do you win in vernacular and Tier-2/3 markets?

The biggest untapped EdTech opportunity in India in 2026 is Tier-2/3 vernacular learners — and most national EdTech brands are still bad at reaching them. The category economics are forgiving (₹20-60 CPI), the audience size is enormous, and competition is materially lower than in metro English-language EdTech.

The four operating principles that separate winning vernacular EdTech strategies from English-language brands trying to localise:

- Vernacular creative is not translated English creative. Re-shoot with regional teachers, regional context examples (cricket and Bollywood references land differently in Tamil Nadu versus Bihar), regional accents. Translated voice-over on English video performs 3-5x worse than native-shot regional video. This is the single most expensive mistake international and national brands make.

- WhatsApp-first funnels: Many vernacular users prefer WhatsApp over in-app messaging — for demo class scheduling, doubt resolution, content delivery. Build the WhatsApp middleware before scaling vernacular paid spend, not after.

- Lower price points: Tier-2/3 willingness-to-pay is materially lower. Lower-priced tiers (₹99-₹299/month) often outperform full-price subscriptions on net revenue because conversion rate climbs faster than ARPU drops. Sub-₹100 micro-subscriptions also unlock UPI auto-debit payments, which churn dramatically less than card-based subscriptions.

- Light APK + low-end device support: Below 30MB APK download, runs smoothly on 2GB RAM Android phones, works on patchy 4G. Non-negotiable for Tier-3 distribution. Apps over 100MB lose 40-60% of would-be installs to download-abandonment in low-connectivity geographies — visible in Play Console install funnel reports.

In our portfolio, the EdTech apps that have crossed 10M+ installs in vernacular markets share one structural decision: they treated each major language as a separate product team — separate creative, separate teachers, separate content, separate WhatsApp funnels — rather than as a translation layer on top of an English product. The economics rewarded that investment.

For organic discovery in vernacular markets, ASO localisation is critical. Apple and Google both index region-specific metadata for region-specific store impressions. Our ASO optimisation guide covers localised metadata, screenshot translation, and review-rate management by locale.

What retention features justify subscription renewals?

EdTech LTV lives or dies on Month-3 and Month-6 retention. A subscriber who renews at month 3 is 2-3x more likely to renew at month 6, and a Month-6 subscriber is the foundation of profitable LTV in every EdTech category. Five product features consistently drive that retention across our portfolio:

- Visible progress tracking: Parents must see their child improving. Weekly reports, score graphs, completed lesson counts, chapter mastery percentages. The progress visualisation is often more important to renewal than the actual learning outcome — parents renew on perceived progress, not measured progress.

- Live or "live-feel" classes: Cohort-based learning models retain dramatically better than self-paced courses. Even pre-recorded content scheduled to release on a fixed cohort schedule retains 30-50% better than fully on-demand. The accountability and social presence drive completion, completion drives renewal.

- Doubt resolution: A 24-hour answer guarantee, even via async text-based resolution, lifts engagement and renewal materially. Parents and students who get stuck and never get unstuck churn at 2-3x the baseline rate. The cost of staffing async doubt resolution is almost always lower than the LTV uplift it produces.

- Achievement system: Badges, streaks, certificates, leaderboards. Proven engagement multipliers for K-12 and language learning. Streaks especially — a 30-day learning streak creates a sunk-cost commitment that delays churn long enough for the value of the product to register.

- Parent dashboard: Separate parent-mode that shows usage, progress, areas needing attention, upcoming live classes. This is the single feature that most directly drives renewal decisions in K-12 because the parent is the renewing buyer and needs ongoing evidence the spend is working.

The retention work is also where most EdTech apps drop the ball. Acquisition teams ship installs to a product that does not retain them; the LTV maths fall apart; the company concludes "paid UA does not work for EdTech" when the actual problem is the post-install product experience. Across the 300+ apps in our portfolio, the strongest predictor of profitable paid growth is Month-3 retention, not CPI. Fix retention first; scale acquisition second.

For deeper retention playbook see our app retention strategy guide. To audit your EdTech UA and retention together, talk to our EdTech team — we run category-specific diagnostics across funnel, creative, channel mix, and post-install product before recommending spend changes. Past EdTech case work lives at our results page.

Frequently Asked Questions

Is BYJU'S-style mass paid UA still viable for EdTech?+

Not at that scale. Modern EdTech UA depends on cohort economics and disciplined LTV math, not brand-driven mass spending. Targeted, retention-led growth has replaced the volume-led playbook of 2020-2022.

Should an EdTech app launch with subscription or one-time pricing?+

For K-12 and ongoing learning: subscription. For test-prep and short-duration upskilling: one-time often converts better and reduces refund disputes. Match pricing model to course duration, not to industry default.

How do I market to parents vs students differently?+

Parents on Facebook, WhatsApp, and YouTube parent-creator content with outcome-focused creative. Students on Instagram and YouTube with gamified, achievement-focused creative. Build a conversion flow inside the app that bridges both within 48 hours of student install.

Are influencer parents effective for K-12 EdTech?+

Very. Parent influencers with 50K-500K followers in education and parenting niches drive among the highest-converting paid placements in Indian K-12 EdTech, with trust signals that paid Meta creative simply cannot match.

What is realistic install-to-paid conversion for EdTech?+

K-12 supplementary: 3-8% in 30 days. K-12 test prep: 5-12%. College/competitive exams: 4-10%. Adult upskilling: 1-5%. Below those ranges usually indicates onboarding, pricing-fit, or creative-trust problems rather than channel problems.

How much does it cost to acquire an EdTech subscriber in India in 2026?+

Blended cost-per-paid-user (not per-install) typically runs ₹500-2000 for K-12 supplementary, ₹1500-5000 for test prep, ₹3000-10000 for adult upskilling. Plan LTV against these CAC ranges, not against raw CPI — CPI alone is a misleading metric in EdTech.

How important is vernacular for EdTech app growth in 2026?+

Critical for Tier-2/3 reach. Roughly 70%+ of remaining EdTech growth headroom in India sits in non-English vernacular markets. Apps that ship native-shot Hindi, Tamil, Telugu, Bengali, or Marathi content outperform translation-only competitors by 3-5x on engagement.

Sources

- AppsFlyer Performance Index — Quarterly India education category benchmarks for CPI, retention, and conversion windows

- AppsFlyer State of App Marketing — Trend data on India EdTech install-to-paid conversion lengthening post-2023

- Statista — India Smartphone Users Forecast — 1.2B+ smartphone users projected by 2027 with growth concentrated in Tier-2/3 markets

- Meta Advantage+ App Campaigns — Account signal accumulation and peak-season auction performance guidance

- Google Ads — App Campaigns Help — UAC targeting, conversion event setup, and demographic split for parent vs student

- Apple In-App Events — Surfacing demo classes and live events directly on the App Store product page

- Adjust Mobile App Resources — Aggregated benchmarks on creative refresh cadence and CPI by vertical

- Statista — India Mobile Internet Usage — Vernacular-language internet usage and Tier-2/3 mobile data trends

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy