Insurance App Marketing: Trust-First Growth for Fintech-Adjacent Apps

Insurance app marketing is a trust game played over weeks. Compliance constraints + high CAC + long decision cycles make it one of the toughest verticals — and one of the most rewarding.

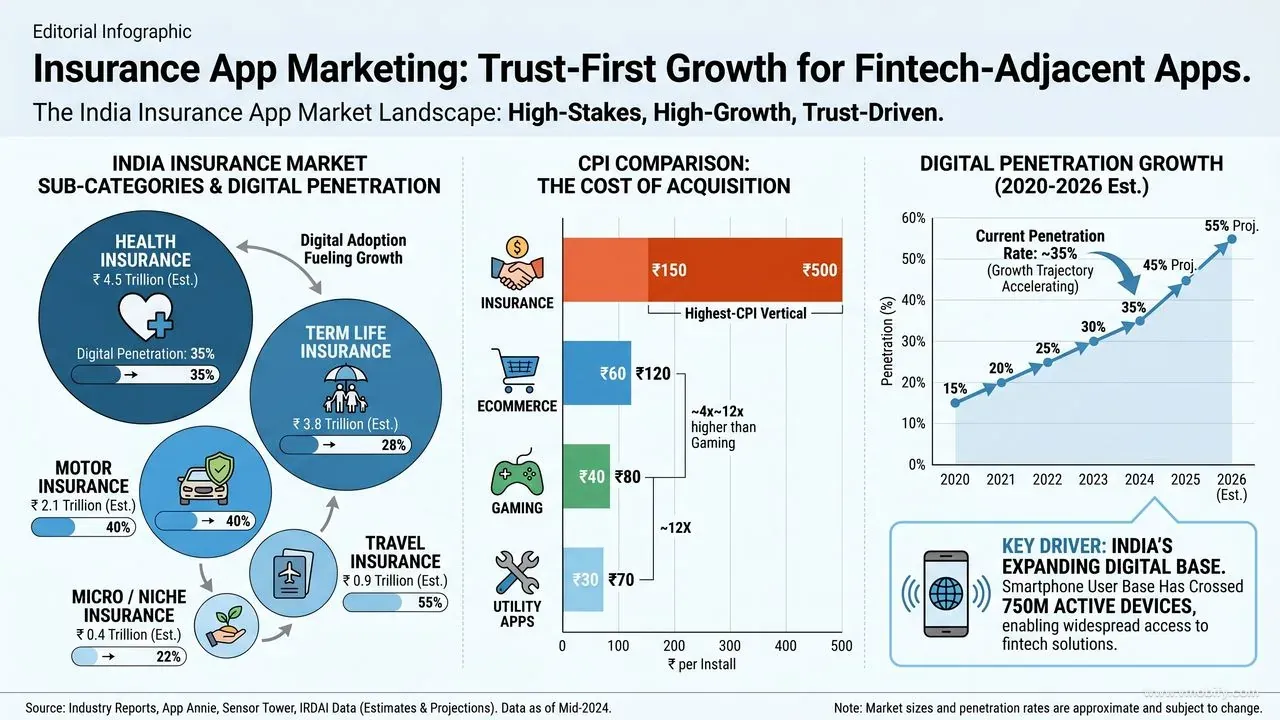

How big is the Indian insurance app market?

Indian insurance app growth has been one of the fintech surprises of the post-2020 decade, with leading platforms now moving tens of billions of rupees in annual premium through pure app channels. PolicyBazaar, Acko, Digit, Onsurity, GoDigit, and a long tail of category-specific apps have transformed what was once a 100% offline agent-driven category into a digital-first funnel for under-40 buyers.

The macro tailwinds are real. India's smartphone base has crossed 750M active devices per Statista's India forecast, household financial penetration is rising in Tier-2/3, and IRDAI's push for digital onboarding and e-KYC has removed most of the structural friction that kept insurance offline through the 2010s. The result: insurance is now the second-fastest-growing fintech subcategory in India after lending.

The categories that matter and the structural differences between them:

- Health insurance — largest by user count, fastest organic growth, most renewal-sensitive.

- Term life insurance — highest single transaction value, longest decision cycle, most lead-handoff to tele-sales.

- Motor insurance — most renewal-driven, lowest CAC, strongest "annual return visit" behaviour.

- Travel insurance — most seasonal (April-June and October-December peaks), cheapest install, lowest LTV per policy.

- Niche / micro-insurance — mobile screen, electronics, cycle, gadget covers. Low ticket, high attach-rate at point-of-sale.

Across our 300+ app portfolio at Vmobify, insurance is consistently in the top 3 most expensive verticals to acquire — comparable to fintech-trading and crypto. But the LTV ceiling is also among the highest in fintech because of multi-year renewals, cross-sell within a household, and the inertia that keeps customers on a familiar app once they have stored their KYC documents and family details.

The competitive structure also matters. The top 4-5 aggregators (PolicyBazaar, Acko, Digit, GoDigit, Onsurity) capture a disproportionate share of branded search and direct app traffic, which means new entrants compete on a narrow set of breakthrough angles: a vertical-specific niche (cyclist insurance, gig-worker health), a product innovation (pay-per-km motor, monthly term life), or a distribution play (employer-bundled, OEM-bundled). Generic "compare and buy" positioning at this point has almost no remaining airspace in the Indian market.

What does insurance app unit economics look like by category?

The five insurance categories operate on radically different economics — confusing them is the single most common reason teams misallocate budget in their first six months. The number to internalise is the gap between CPI and first-policy CAC: most installs do not buy in session 1, and the larger the policy, the longer the gap.

- Health insurance: CPI ₹150-350. First-policy CAC ₹3,000-8,000. Average annual premium ₹15,000-60,000. Renewal rate year-1: 70-85%.

- Term life: CPI ₹200-500. First-policy CAC ₹8,000-25,000. Annual premium ₹8,000-50,000. Renewal rate year-1: 80-90% (because lapse means losing locked-in pricing).

- Motor insurance: CPI ₹80-200. First-policy CAC ₹600-2,500. Annual premium ₹3,000-15,000. Renewal-heavy — most LTV comes after year 1.

- Travel: CPI ₹60-150. First-policy CAC ₹400-1,500. Premium ₹300-3,000 per trip. Repeat purchase rate 25-40% within 12 months.

- Micro-insurance: CPI ₹40-120. First-policy CAC ₹150-500. Premium ₹200-2,000. Often sold as an upsell rather than a primary destination.

The "CPI to CAC" multiple — typically 5-20x across these categories — exists because insurance is not an impulse purchase. AppsFlyer's State of App Marketing reports the same pattern globally: fintech-insurance verticals consistently show the largest funnel drop-off between install and first revenue event of any consumer category, ahead of even loans and trading.

The strategic implication is straightforward. Health and term life campaigns must be measured on 30-60 day cohort policy-issuance rate, not weekly install volume. Motor and travel can be measured weekly because the decision cycle is shorter and tied to a triggering event (RC renewal date, trip booking). We have seen multiple insurance teams burn ₹50L+ in their first quarter optimising for installs and conclude "paid does not work" when the real issue was an attribution window 60 days too short. Get your UA measurement architecture right before scaling spend.

Why is the insurance trust funnel so long?

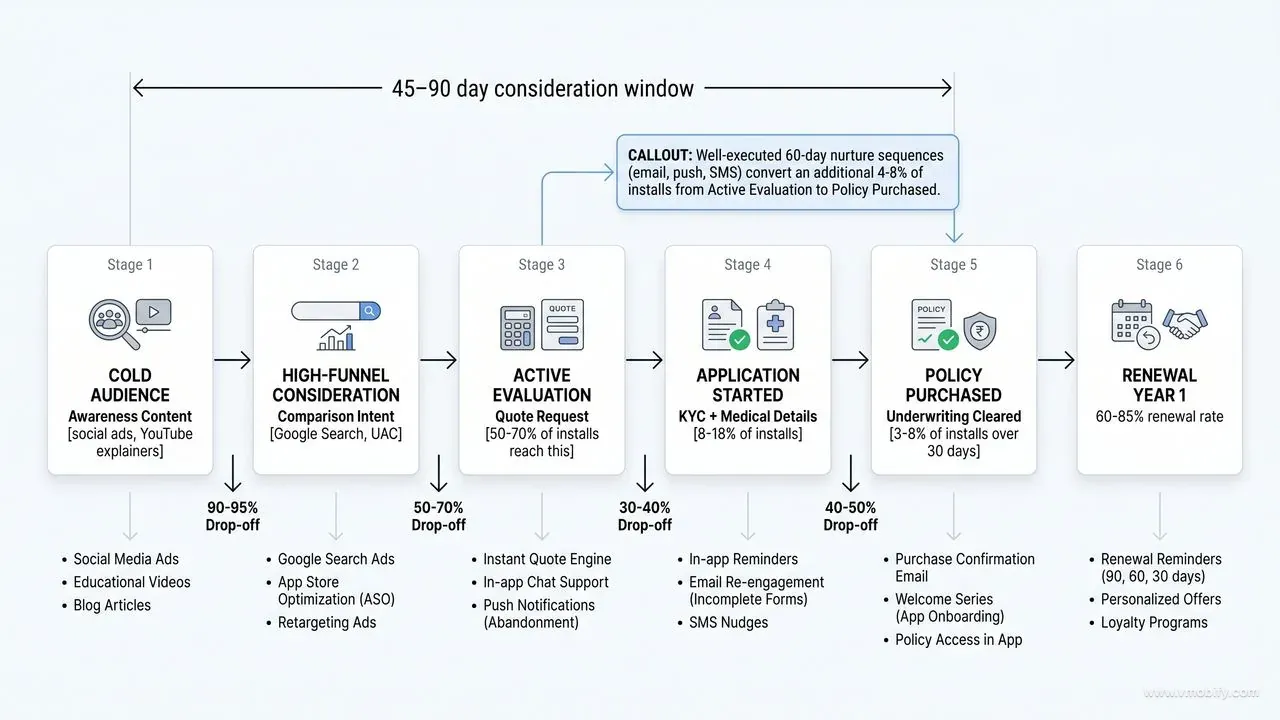

Insurance buying takes 2-8 weeks from first awareness to policy purchase, and the app must hold the user through that entire journey across 6 distinct behavioural stages. Treating it as a single-session funnel — the way you would model a hyper-casual game or an ecommerce app — guarantees wasted spend.

The realistic funnel for a health or term insurance app, measured across our portfolio benchmarks:

- Install: Lowest-friction entry. Free quote, premium calculator, or comparison view as the value promise. 100% of paid traffic enters here.

- First quote generation: 50-70% of installs reach this step in the first session. This is your primary optimisation event for paid channels.

- Comparison view: 30-50% of installs. Strong intent signal — the user is now in active evaluation mode and has shown enough trust to compare insurers.

- Application started: 8-18% of installs. Real buying behaviour. KYC begins, medical questionnaire begins, beneficiary details captured.

- Policy issued: 3-8% of installs over a 30-day window. Underwriting clears, payment processed, policy document delivered.

- Renewal at year 1: 60-85% of issued policies depending on category. This is where insurance UA actually pays back.

Optimise paid channels on at least "quote generated" — preferably "application started." Optimising on install creates expensive useless installs because the algorithms find users who tap and forget. Both Google UAC and Meta Advantage+ explicitly support deep in-app conversion events; Google's App Campaigns documentation is clear that downstream event optimisation outperforms install optimisation for considered-purchase verticals.

The corollary: build a retention layer for the 92-97% of installs that do not buy in 30 days. Push notification sequences ("your free quote is still valid"), email re-engagement with personalised premium drops, and in-app comparison reminders all extend the conversion window meaningfully. In our portfolio, well-executed 60-day nurture sequences convert an additional 4-8% of installs to first policy — often doubling effective campaign ROI.

How do IRDAI and platform compliance shape insurance UA?

Insurance is one of the most heavily regulated ad categories on every major platform — IRDAI rules, Meta and Google certification, and state-level marketing restrictions stack on top of each other, and getting any one wrong can halt your campaigns for weeks. Compliance is not a checklist item; it is the structural constraint that shapes everything from creative concepts to landing-page copy.

- IRDAI marketing guidelines: The Insurance Regulatory and Development Authority of India is strict on claims, benefits language, and mandatory exclusions disclosure. Misleading creatives can trigger regulatory show-cause notices and have led to public penalties against named insurers.

- Meta and Google insurance-category certification: Mandatory for ad delivery. Approval typically takes 1-3 weeks and requires submitting your IRDAI licence, broker registration, and sample creatives for pre-review. New ad accounts running insurance creatives without certification get flagged and paused within hours.

- Forbidden ad claims: "Best insurance", "Guaranteed payouts", "100% claim approval", "No questions asked claims", "Cheapest in India" — all consistently rejected on platform review. Comparative claims against named competitors are similarly blocked.

- Required disclosures: "T&C apply" in legible type, IRDAI licence number, claim settlement ratio with the source/year when stated, and policy term clarity ("for the policy year shown"). These must appear in creative or on the landing page.

- State-level variation: Some states restrict tele-marketing follow-ups under their telecom regulator rules; others restrict certain product types or impose additional disclosure requirements. Maharashtra, Karnataka, and Tamil Nadu in particular have more aggressive consumer-protection enforcement.

The operational implication: build a compliance-pre-approved creative library and an internal review SOP before you scale spend. We have seen entire weeks of paid budget evaporate because a single non-compliant variant tripped an account-wide review on Meta. The teams that scale insurance UA cleanly are the ones with a 5-day creative approval pipeline (legal review + IRDAI compliance check + platform spec audit) built into their workflow.

For app-store-side compliance, both Apple's App Store Review Guidelines and the Google Play Developer Policy have specific financial-services sections that govern claims you can make in store metadata and screenshots. These are separate from ad-platform rules and have caught even well-funded insurance apps off-guard during listing reviews.

Which channels work best for insurance app acquisition?

Insurance UA in India concentrates on five channels, with Google (UAC + Search) dominating because intent keywords capture the high-funnel decision moments that other channels cannot. The optimal allocation across our portfolio for mid-stage insurance apps:

- Google UAC + Search (40-50% of spend): "Term insurance compare", "best health insurance for parents", "car insurance renewal" — high-intent search dominates because users actively researching insurance type the query before they tap an app. UAC layers in-feed and YouTube placements on top of Search for full-funnel coverage.

- Meta (25-35%): Demographic targeting using age bands, life-stage proxies (recent marriage, new parent, home purchase), and income proxies through interest layering. Approved insurance creative only — see compliance section above.

- YouTube (10-15%): Explainer videos, claim-process content, customer testimonials. YouTube is where complex products like term life and family floaters actually get understood before users move to direct response on UAC.

- Influencer / financial creators (5-10%): Personal finance YouTube creators (Pranjal Kamra, Akshat Shrivastava and similar tier) drive disproportionately high-quality conversions because their audiences arrive pre-educated on insurance value. Statista's India influencer market data shows finance creators commanding some of the highest brand-fee rates in the country precisely because of this conversion quality.

- OOH + offline (5-10% for large players): Brand reinforcement, particularly in Tier-2/3 metros where television and outdoor still drive recall. Only viable above ₹5Cr quarterly spend.

The structural mistake we see most often: founders trying to make Meta the primary channel because it is the cheapest CPI. Meta cold traffic for insurance converts to policy at roughly 30-50% the rate of Google Search traffic, because Search captures expressed intent and Meta captures interrupted attention. Cheaper installs that convert worse is not a win. Build your ASO foundation first so organic search inside the stores compounds, then layer Google UAC + Search as the paid backbone, then add Meta + influencer for top-funnel scale.

Apple Search Ads is undervalued for term life and health insurance specifically — iOS users skew higher income and the keyword inventory is less competitive than on Google. Across our portfolio, ASA for insurance regularly returns 2-3x ROAS vs Meta for premium-product variants.

Channel sequencing also matters. New insurance apps that try to launch all five channels in week 1 fragment their data, starve each campaign of conversion volume, and produce noisy signal across the board. The sequence that works: weeks 1-4 Google UAC + Search only (with conversion events firing properly), weeks 5-8 layer in Meta with the proven hooks from Google, weeks 9-12 add YouTube and ASA, then influencer and OOH once you have at least 6 months of cohort LTV data to size the brand investment against. Skipping ahead is the most common reason ₹2-5Cr quarterly insurance budgets produce mediocre payback curves. For category-specific CPI benchmarks across Indian verticals, see our India CPI benchmark guide.

What insurance creative actually converts?

The single highest-converting creative format in insurance is the real claim testimonial — a named customer, a specific claim amount, and the words "they paid" on screen — and it consistently out-converts fear-based creative by 2-4x in our portfolio. Trust is built through proof, not anxiety.

- Outcome / claim testimonials: Real claim stories with names and amounts where IRDAI-compliant. The highest-converting format we have tested across insurance clients. Production cost is moderate; the asset compounds across channels for 6-12 months.

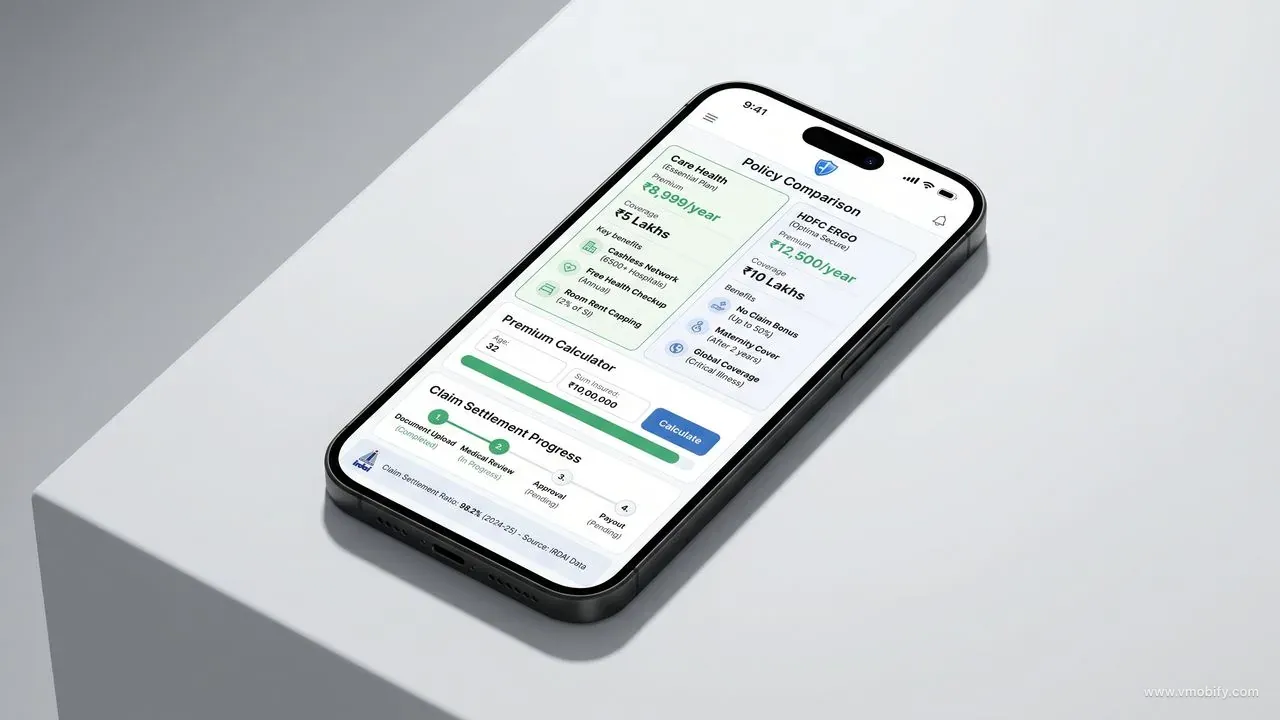

- Comparison demos: "See your premium in 30 seconds" — friction-removal as the hook. Screen recordings showing the quote-generation flow consistently out-perform static comparison charts because they demonstrate the product working.

- Explainer content: "Health insurance for parents above 60", "Term insurance for new fathers", "Bike insurance renewal under ₹2,000" — segmented life-stage targeting in both the targeting layer and the creative messaging. Specificity converts better than generality at every test we have run.

- Trust signals visible in every creative: IRDAI licence number, claim settlement ratio (with year/source), insurer partner logos, customer count. These are non-negotiable for the disclosure-conscious user and double as compliance shields.

- Avoid fear-based creative: "What if you die tomorrow", "Your family will be on the streets" — often gets rejected by both IRDAI and platform reviewers, and converts worse than expected even when approved because it triggers user defensive reactions rather than action.

Production strategy that works at scale: build a library of 8-12 outcome-testimonial videos (30-60 seconds each, vertical and horizontal cuts), supplement with 4-6 explainer videos per audience segment, and refresh hooks every 3-4 weeks. Meta creative fatigues fast for insurance because the audience demographics are narrow; Google UAC creative lasts longer but still benefits from monthly refresh. See our broader playbook on Meta App Install Campaigns for creative testing protocols that transfer directly.

Landing pages matter as much as creative. A user who clicks an ad expecting "instant quote in 30 seconds" and lands on a 9-field form will bounce at 70%+ rates. The teams that win in insurance UA align ad promise with first-screen experience — usually a single-field entry (age or vehicle number) that progressively reveals the quote.

How do you build retention through renewals?

Insurance LTV is renewal-driven — year-1 renewal of 60-85% is the difference between profitable and unprofitable UA, and every renewal point is worth far more than an additional install. Marketing must invest in retention from day 1 of the customer relationship, not bolt it on after year-1 churn becomes visible.

- Renewal reminders at 60 / 30 / 7 days before policy expiry: Push + email + SMS combined. Each channel reinforces the others; single-channel reminders underperform multi-channel by 15-25% in renewal rate across our portfolio benchmarks.

- One-tap renewal flow: Pre-filled payment, no re-KYC for in-policy renewals, saved card or UPI mandate where possible. Every additional step in the renewal flow drops conversion 5-10%; the apps with the smoothest renewal flows hit 85%+ retention.

- Claim experience excellence: The single biggest renewal-rate driver. Customers who successfully claim renew at 90%+; customers who experience friction or denial during claims renew at 25-40%. This makes claims operations a marketing channel, not a back-office function.

- Cross-sell within the app: Health insurance customers shown term insurance after 6 months; motor customers shown travel before the holiday season; term customers shown family floaters at policy anniversary. Cross-sold customers have 30-50% higher 24-month LTV and lower churn because of the compounding switching cost.

- Family portfolio view: Manage all family policies in one app — spouse health, parents' senior plan, kids' education-linked, motor across vehicles. Switching cost compounds; users with 3+ policies in an app renew at near-100% rates.

For tactical retention frameworks that apply across categories, see our app retention strategy guide. The principles transfer, but insurance has the unusual property that retention behaviour is locked in 12 months ahead — what you do during onboarding and the first claim determines whether a renewal lands a year later.

Measurement tip: track 24-month LTV cohorts, not month-by-month revenue. Insurance UA decisions made on first-month revenue alone consistently under-invest in the channels that drive renewal-heavy customers. Adjust's MMP cohort guides show the same pattern across other long-LTV verticals — the apps that win invest based on projected LTV, not booked LTV.

If you are launching an insurance app or scaling an existing one and want a managed UA + retention programme, talk to our team. We have run UA for fintech-adjacent apps across health, motor, and micro-insurance categories — view our case studies for relevant outcomes and detailed measurement frameworks.

Frequently Asked Questions

Is insurance the most expensive vertical for app installs?+

Among the top 3. Fintech-trading and crypto can be higher, but insurance is consistently in the top tier for both CPI and first-policy CAC, with health and term life being the most expensive sub-categories.

How long does insurance UA take to pay back?+

Typically 12-24 months for health and term life. Motor and travel pay back faster (3-9 months) due to lower CAC. Renewal rate is the largest variable — a 10-point renewal-rate improvement can cut payback by 6+ months.

What is the most important metric for insurance UA?+

First-policy CAC and 24-month LTV — and specifically the gap between them, with renewal rate as the main multiplier. Track these as cohort metrics, not monthly aggregates.

Do insurance apps need offline sales support?+

For high-value products (term life, complex health floaters) — often yes. Tele-callers and relationship managers improve conversion by 20-40% on warm leads. For simple products (travel, motor, micro), pure digital flows work without offline support.

Can insurance apps run on TikTok?+

Limited in India — TikTok is unavailable and most short-form spend goes to Instagram Reels and YouTube Shorts. Both platforms enforce strict financial-ad rules; insurance creative requires the same certification as on Meta news-feed.

How long does insurance ad approval take on Meta and Google?+

Initial certification 1-3 weeks. Individual creative approval typically 24-72 hours once the account is certified. Non-compliant creatives can trigger account-wide review that pauses delivery for 5-10 days — build a pre-approval workflow internally.

What is the realistic minimum monthly budget for insurance UA in India?+

For meaningful learning and channel diversification, ₹15-25L per month. Below ₹10L per month, focus spend on Google UAC + Search only — Meta and influencer channels need more volume to produce reliable signal in a long-funnel category.

Sources

- IRDAI — Insurance Regulatory and Development Authority of India — Primary regulator for insurance marketing claims, disclosures, and licensing in India

- AppsFlyer — State of App Marketing — Cross-vertical install-to-revenue funnel benchmarks including fintech-insurance

- Google Ads — App Campaigns Help — Official documentation on deep-event optimisation for considered-purchase verticals

- Apple App Store Review Guidelines — Financial-services section governs claims allowed in insurance app store metadata

- Google Play Developer Policy — Financial-services category rules for insurance app listings and disclosures

- Statista — India Influencer Marketing Market — Indian creator economy growth data — finance creators command premium rates

- Statista — Smartphone Users in India — Smartphone-base forecast underpinning insurance app addressable market

- Adjust — Resources and Cohort Guides — MMP guidance on long-LTV cohort measurement for considered-purchase verticals

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy