Alternative App Stores in 2026: A Multi-Store Distribution Guide

Google Play still drives the volume, but the Galaxy Store, Indus Appstore, Xiaomi GetApps and Huawei AppGallery each open reach and billing economics Play cannot. Here is a 2026 decision framework for which alternative app stores actually earn their place — and which to ignore.

Why should app developers look beyond Google Play in 2026?

You look beyond Google Play in 2026 for three concrete reasons — to reach device audiences Play does not concentrate, to cut the 15-30% billing commission on in-app revenue, and to hedge against a single store owning your entire distribution — not because Play is failing you. Play remains the default on virtually every Android phone and stays your primary volume engine; the case for alternative app stores is additive, not a replacement.

The reach argument is the simplest. A single-OEM store like Samsung's Galaxy Store sits preinstalled on roughly a billion active devices, and India-native stores like the Indus Appstore and Xiaomi GetApps come factory-loaded on millions of handsets that skew Tier-2 and Tier-3. Those storefronts surface your app to people who never open Play to go looking — discovery you cannot buy back later.

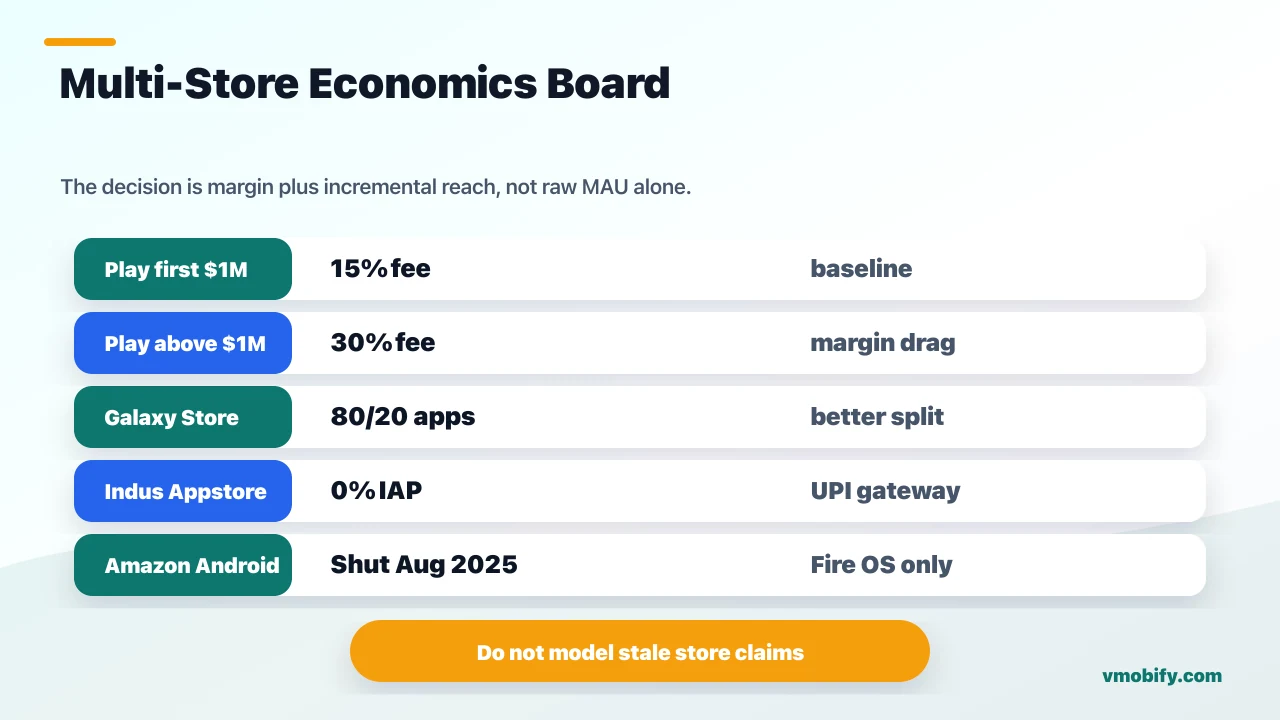

The economics are sharper still. Google Play mandates its own billing on most digital goods, taking 15% on the first $1 million of annual revenue and 30% above it. Several alternative stores undercut that split or waive in-app commission entirely, so for a subscription or in-app-purchase business the saved commission compounds on every renewal. If you run app store optimisation seriously, the store you publish on is now a margin decision, not just distribution.

Across our 300+ apps managed since 2013, the question we field from almost every India-focused client is whether a second or third store is worth the overhead. The honest answer has shifted: for a global, metro-English, ad-monetised app it is often still no, but for an India-first product with in-app revenue it is increasingly yes. This guide gives you the framework to decide which camp you are in.

Which alternative app stores have the most reach?

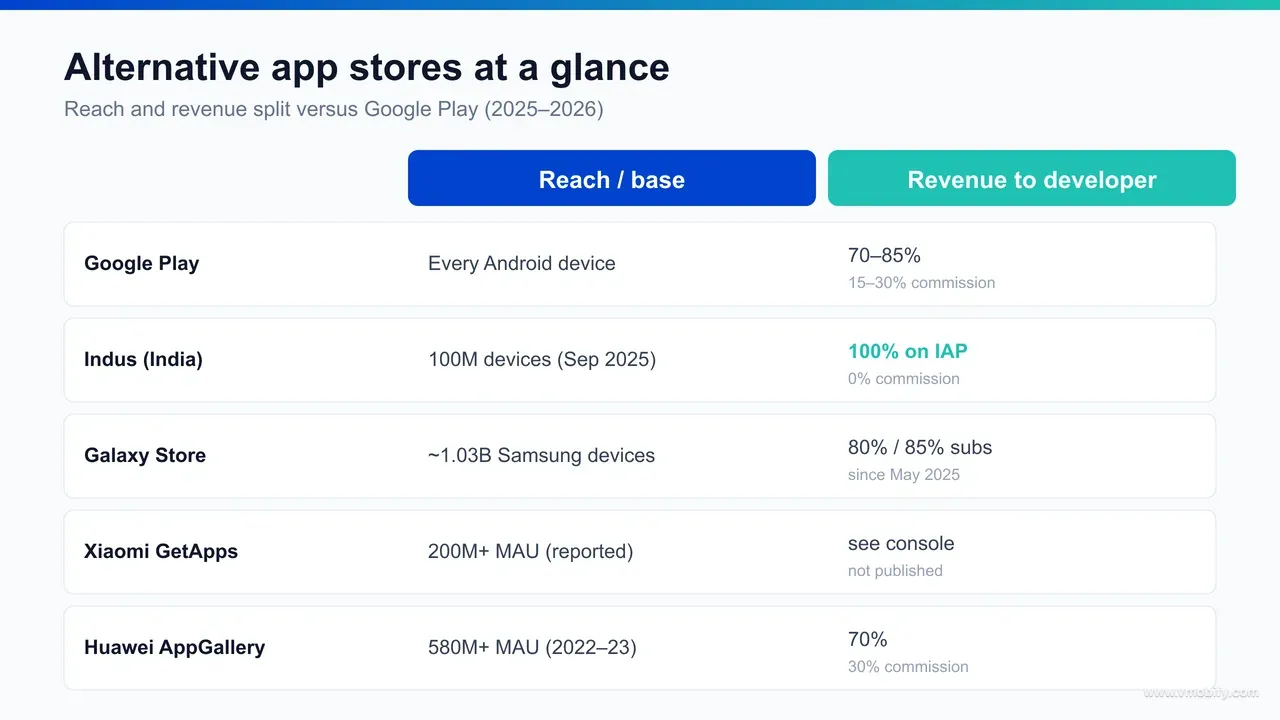

By installed-base reach in 2026 the order is the Samsung Galaxy Store (roughly 1.03 billion active Samsung devices), Huawei AppGallery (580 million-plus monthly active users as of its 2022-23 figure), Xiaomi GetApps (200 million-plus MAU across 59 regions), and the Indus Appstore (100 million India devices as of September 2025) — but raw reach is only useful once you map it to where your audience actually lives. A billion devices in markets you do not sell to is worth less than 100 million devices that are exactly your audience.

The Galaxy Store has the largest single-OEM footprint. Samsung crossed one billion active devices worldwide, and the store ships preinstalled on every one of them, per SamMobile. That makes it the largest addressable base outside the two dominant stores, concentrated in Samsung-strong markets across Europe, Asia and the Americas.

Huawei's AppGallery reported 580 million-plus monthly active users across 170-plus countries with more than six million registered developers — but that headline is a 2022-23 figure, per HuaweiCentral, and the base is heavily China, the Middle East and parts of Europe, with low India relevance after the 2020 sanctions. Xiaomi's GetApps reports 200 million-plus MAU across 59 regions — a secondary figure worth treating as directional — and is strongest in India, Indonesia, Russia and the CIS. The Indus Appstore reached 100 million (10 crore) India devices and 80 million-plus users by September 2025, per PhonePe's milestone announcement, with 70.6% of users in Tier-3 regions — the most India-native footprint of the four.

The lesson is that reach is regional, not global. We have seen apps add a billion-device store and get almost nothing because their users were never on Samsung hardware, while a 100-million India store delivered real installs because the device audience matched exactly. Read every MAU figure with its year and geography attached.

How do revenue splits compare across the major stores?

On revenue splits the Indus Appstore is the most generous (zero commission on in-app purchases with your own gateway), the Galaxy Store now runs 80/20 on apps and games and 85/15 on subscriptions, Huawei AppGallery and most others sit at the standard 70/30, and Google Play takes 15% up to $1M then 30% — so for a monetised app the store you choose is a direct margin lever. Getting these splits right is where multi-store distribution either pays for itself or does not.

The Indus Appstore is the outlier. It charges no commission on in-app purchases and lets you integrate any payment gateway you already use, per PhonePe's developer-platform announcement — which for an India app usually means routing through UPI. For a subscription business escaping even Play's reduced 15% subscription cut is a margin gain that recurs on every renewal, and on Indus that platform take is zero.

The Galaxy Store's 2025 change is the most material shift in this space. As of 15 May 2025, Samsung moved to an 80/20 split on apps and games and 85/15 on subscriptions, up from the old 70/30, per the Samsung Developer newsroom — an explicit play to win game developers, as Engadget reported. On ₹50 lakh of annual in-app revenue, the difference between a 70/30 and an 80/20 split is ₹5 lakh kept rather than handed to the store.

One stale claim to bury before it costs you a planning decision: Huawei AppGallery's "100% first-year revenue" line. That was a promotional offer that expired around 2019-2020; the current standard rev-share is 70/30, the same as most stores. Treat the 100% figure as dead. The pattern across all of these is that the headline split only matters in proportion to how much in-app revenue you actually process — a generous split on a store where your audience does not buy is worth nothing, which is why split and reach have to be read together.

Which alternative app store fits the Indian market best?

For the Indian market the Indus Appstore is the strongest single bet, with Xiaomi GetApps as the natural pairing — together they cover the Tier-2/3, vernacular, price-sensitive device audience that Play reaches but does not concentrate, while Huawei AppGallery and the Galaxy Store are weaker India fits. India is where the alternative-store case is unusually strong, because the device channel and the billing economics both line up.

The Indus Appstore is the most India-native store available. PhonePe owns it, so it carries a payments rail and the muscle to strike preinstall deals — it ships factory-loaded on Xiaomi and Lava handsets, with a Motorola India deal announced in December 2025. Its 100 million-device base skews 70.6% Tier-3, roughly 40% of users navigate in a regional language, and it indexes discovery in English plus 12 Indian languages. Our deep-dive on the Indus Appstore as an India-first distribution play covers the publishing flow and ASO in detail.

Xiaomi GetApps complements Indus rather than competing with it. It is preinstalled across Xiaomi's enormous MIUI base in India, so listing on both Indus and GetApps puts you in front of a large slice of the non-metro Android population that no single store reaches. The two together are the device-channel saturation play for an India-first app — which matters because, as our analysis of India app install trends in 2026 shows, the next 200 million Indian internet users are overwhelmingly Tier-2/3 and vernacular-first.

Huawei AppGallery, despite its 580 million-plus global users, has low India relevance after the 2020 sanctions cut Huawei's handset presence there — we would deprioritise it for an India-only strategy. The Galaxy Store reaches Indian Samsung owners, but that audience skews more metro and English-comfortable, so its India edge is smaller than its global reach suggests. The practical India stack is Play for volume, Indus for vernacular reach and zero-commission billing, and GetApps for MIUI device coverage.

How does alternative-store ASO differ from Google Play ASO?

Alternative-store ASO differs because each store indexes different metadata fields with different weights — some offer dedicated keyword fields Play does not, some weight the app name far more heavily, and several index vernacular search Play ignores — so you cannot copy-paste your Play listing and expect it to rank. The build artefact is the same; the optimisation is not.

Xiaomi GetApps is the clearest example of a store with its own field structure. It offers a dedicated keyword field of roughly 80-100 characters — a surface Play and Apple do not provide — alongside a 50-character title, a one-line subtitle up to 96 characters, and a description up to 4,000 characters, per ASOMobile's GetApps analysis. That keyword field is free ranking real estate you must populate deliberately — nothing in your Play listing maps to it.

Huawei AppGallery weights the app name more heavily than most stores. Its app name supports up to 64 characters and is a top ranking factor, with the Introduction and "New features" fields also indexed, per published AppGallery ASO analyses — far more keyword room than Play's 30-character title. Note that most of these stores do not publish their ranking algorithm, so treat field weights as informed best practice rather than confirmed mechanics; the broad differences between store algorithms are real, as our breakdown of the App Store versus Google Play algorithms explains.

The Indus Appstore adds a dimension Play has no equivalent for: it indexes discovery across 12 Indian languages and supports voice search in 10 of them, so vernacular keyword research becomes a ranking lever rather than a nice-to-have. In our portfolio the teams that get the most from alternative stores treat each one as its own ASO surface — researching the real indexed fields and the spoken vernacular terms per store — rather than translating their Play metadata once and reusing it everywhere. That discipline is the difference between a second listing that ranks and one that sits invisible.

Is the Amazon Appstore still worth it after its 2025 shutdown?

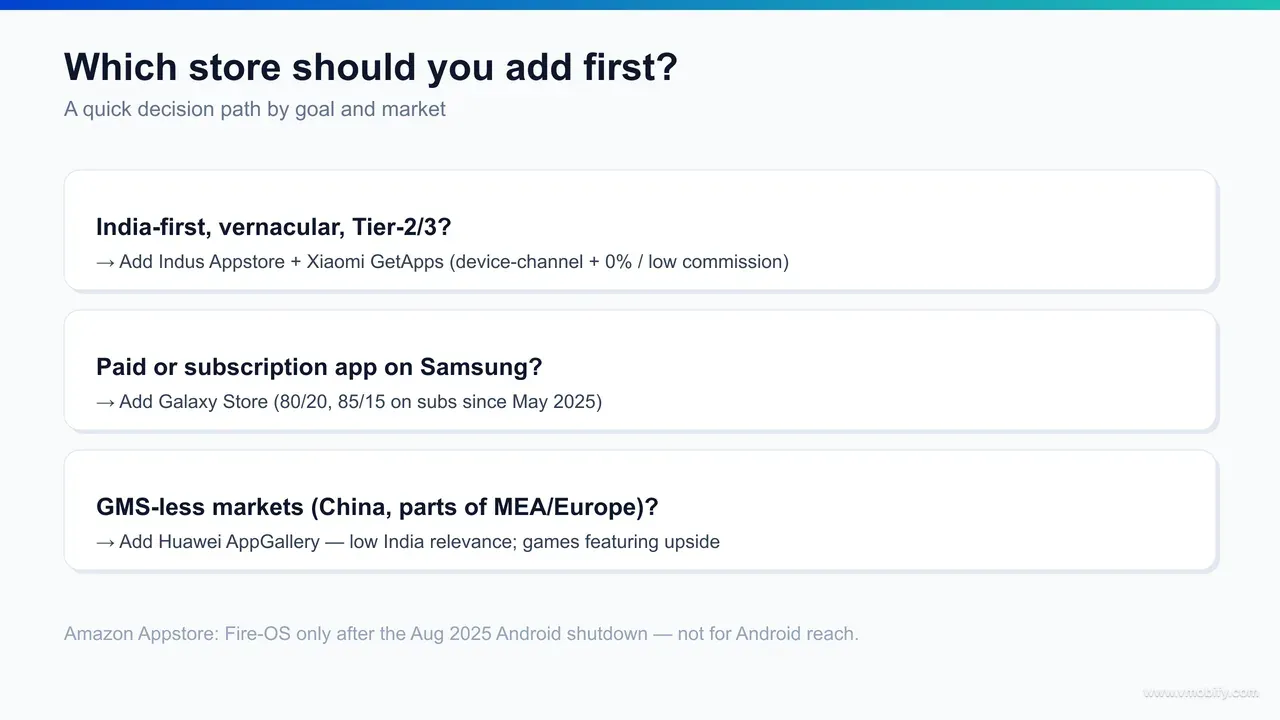

No — not for Android reach. Amazon discontinued its Android Appstore on 20 August 2025 (it stopped accepting new Android submissions on 20 February 2025), so the store now exists only on Fire OS devices, and you should ignore it for any Android distribution strategy. This is a clean decision, and it removes a store that appears on a lot of outdated alternative-store listicles.

The shutdown was announced directly by Amazon. Per the Amazon Developer blog, the Amazon Appstore for Android devices and the associated Amazon Coins program were wound down, with the store remaining available only on Amazon's own Fire tablets and Fire TV hardware. If your goal is reaching Android phones, the Amazon Appstore is no longer a channel — full stop.

Any guide still recommending you publish to the Amazon Appstore "to reach more Android users" is working from pre-2025 information. Fire OS is a fork of Android, so a Fire-tablet listing can make sense for a specific tablet-content app, but that is a narrow, hardware-bound case — not the broad Android reach the store used to offer. For the multi-store decision in this guide, it simply drops off the list.

Stale listicles are exactly where bad distribution decisions come from. We have seen teams spend a sprint preparing an Amazon Appstore submission for "extra Android coverage" that no longer exists. Spend that effort on a store whose device audience is still live — the Galaxy Store, Indus or GetApps — instead.

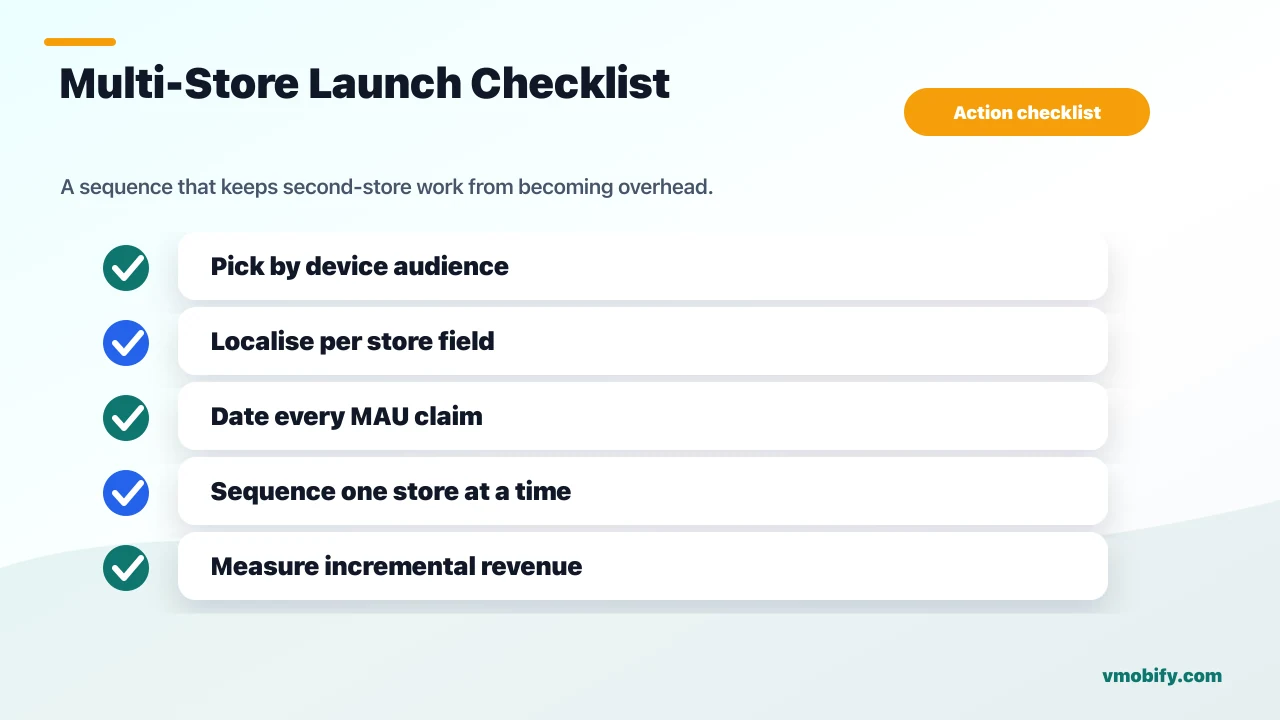

How do you run a multi-store strategy without doubling the workload?

You keep the workload manageable by reusing one build artefact across stores, centralising your store assets and release process, automating where each store allows it, and being selective about which stores you maintain — the cost is in per-store ASO and review, not in the binary itself. The same APK or App Bundle ships everywhere, so the incremental work is metadata and maintenance, not re-engineering.

Start with what genuinely carries over. Your build, your screenshots' source files, your feature graphics and your core positioning are reusable across every Android store. What is not reusable — and should not be copy-pasted — is the indexed metadata: titles, keyword fields and descriptions need per-store optimisation because, as covered above, the fields and their weights differ. Treat the build as shared infrastructure and the listing as store-specific.

- Centralise releases: maintain one source of truth for your build and store assets, then push to each store on a defined cadence rather than ad hoc, so versions do not drift.

- Sequence, do not parallelise blindly: add stores one at a time, prove the incremental installs and revenue, then add the next — rather than launching on five stores at once and maintaining none of them well.

- Budget for per-store review: each store runs its own review, with its own timeline and policy quirks; plan for a review window per store rather than assuming an instant publish.

- Measure each store on its own contribution: judge a store on its incremental installs and commission savings, not against Play's volume — a store that adds 5% incremental India revenue at zero commission is a win even if it never rivals Play.

The honest constraint is operational capacity. Across our 300+ apps managed since 2013, the teams that succeed at multi-store distribution treat it as a deliberate, sequenced programme — not a one-time bulk upload. If you can resource per-store ASO and a clean release process, the marginal effort of each additional store is small relative to the reach and margin it can unlock. Two stores done well beat five done badly.

What do developers most often get wrong about alternative app stores?

The most common mistakes are publishing everywhere instead of where the audience sits, copy-pasting Play metadata and expecting it to rank, trusting stale stats (dead Huawei promos, inflated or undated MAU figures, the discontinued Amazon Android store), and measuring alternative stores against Play's volume instead of their own incremental contribution. Almost every disappointing multi-store launch traces back to one of these.

- Publishing everywhere: the instinct to list on every store maximises overhead and dilutes effort. Reach only counts when the device audience matches yours — a billion-device store is worthless if your users are not on that hardware.

- Reusing Play metadata verbatim: stores with dedicated keyword fields or vernacular indexing reward listings written for them. Copy-pasted Play copy leaves ranking signals on the table — most visibly Xiaomi GetApps' 80-100 character keyword field and Indus's 12-language discovery.

- Trusting stale facts: the alternative-store space is full of recycled claims — Huawei's expired "100% revenue" promo, the Amazon Android store that shut down in August 2025, undated MAU numbers presented as current. Date every figure and verify every commission rate before you plan around it.

- Wrong success metric: a second store will rarely rival Play on volume. Holding it to that bar guarantees disappointment; measuring its incremental installs, vernacular reach and commission savings shows whether it actually earned its place.

The thread connecting all four is treating alternative stores as smaller copies of Play rather than distinct channels with their own economics, audiences and ranking mechanics. The teams that get it right scope each store before launch — what audience it concentrates, what it saves on billing, and what incremental contribution would make it worthwhile — then resource it to hit that. That up-front clarity is worth more than any single tactic.

How should you decide which stores to add first?

Decide by working from your device audience and monetisation model outward — add the store whose preinstalled base matches your users and whose billing economics most help your model, prove the incremental contribution, then add the next, rather than ranking stores by raw reach. The right first store for an India fintech app is almost never the right first store for a global game, and that is the whole point of deciding rather than defaulting.

Three routes cover most teams. If you are India-first with in-app revenue, start with the Indus Appstore — zero-commission billing and vernacular reach line up perfectly — then add Xiaomi GetApps for MIUI coverage. If your audience is Samsung-heavy and you sell paid apps, subscriptions or games, the Galaxy Store's 80/20 split and one-billion-device base make it the obvious first add. If you target Google-less markets in China, the Middle East or parts of Europe, Huawei AppGallery is the relevant channel despite its low India fit.

And there is a fourth, equally valid route: add nothing. If you are a metro-English, ad-monetised app with no in-app purchases, the commission advantage does not apply and the vernacular edge is muted — Google Play alone serves you fine, and a second listing is overhead you do not need. Deciding not to expand is a real answer, not a failure to act.

Whichever route fits, sequence it: add one store, write store-specific ASO, measure incremental installs and revenue over a real window, and only then add the next. If you want help deciding whether a multi-store strategy is worth the operational overhead for your specific app — and want it set up, optimised and measured properly rather than launched and forgotten — that is exactly the India growth work our install and distribution team runs, and you can talk to us directly to scope it.

Frequently Asked Questions

What is the best alternative app store for Android?+

It depends on your audience. By raw reach the Samsung Galaxy Store leads with roughly one billion active devices; for the Indian market the Indus Appstore and Xiaomi GetApps are the strongest device-channel plays. The best store is the one whose preinstalled base matches your users and whose billing economics help your monetisation model.

Do alternative app stores pay better than Google Play?+

Some do. The Indus Appstore charges zero commission on in-app purchases, and the Samsung Galaxy Store moved to an 80/20 split (85/15 on subscriptions) in May 2025, both better than Play’s 15-30%. Huawei AppGallery and most others sit at the standard 70/30. The saving only matters in proportion to the in-app revenue you actually process on that store.

Can I publish to multiple app stores from one build?+

Yes. The same Android build artefact (APK or App Bundle) ships across Android stores, so the engineering work is shared. What is not shared is the indexed metadata — titles, keyword fields and descriptions need per-store optimisation, because each store indexes different fields with different weights.

Are alternative app stores safe for users?+

The major OEM and PhonePe-backed stores covered here run their own app review and security checks, and several ship preinstalled by the device maker. As with any store, safety depends on the store’s moderation, so the established alternative stores are the ones to prioritise over unknown third-party APK sites.

Which alternative app store is best for India?+

The Indus Appstore is the strongest single India bet — 100 million-plus devices skewed 70.6% Tier-3, zero IAP commission, and discovery in 12 Indian languages — with Xiaomi GetApps as the natural pairing for MIUI device coverage. Huawei AppGallery has low India relevance after the 2020 sanctions.

Does the Amazon Appstore still work for Android?+

No. Amazon discontinued its Android Appstore on 20 August 2025 and stopped accepting new Android submissions in February 2025. The store now exists only on Amazon’s Fire OS tablets and Fire TV hardware, so it is not a viable channel for reaching Android phones.

How do app updates work on alternative app stores?+

Each store distributes and updates the build you submit to it, so you push new versions per store on your own release cadence. Some younger stores route certain updates back through the original store, which can fragment version management — plan a centralised release process so versions do not drift.

Sources

- SamMobile — One billion active Samsung devices — Galaxy Store installed base (~1.03B active devices)

- Samsung Developer — New Galaxy Store revenue-share model — 80/20 apps and games, 85/15 subscriptions, effective 15 May 2025

- Engadget — Samsung cuts Galaxy Store commission to 80/20 — The split change as a play to win game developers

- Indus Appstore — 10 crore devices milestone — 100M devices, 80M+ users, 70.6% Tier-3 (September 2025)

- PhonePe — Indus developer platform launch — Zero IAP commission and bring-your-own-gateway billing

- HuaweiCentral — AppGallery exceeds 580 million users — 580M+ MAU, 170+ countries (2022-23 figure)

- Amazon Developer — Changes to the Amazon Appstore for Android — Android Appstore discontinued 20 August 2025 (Fire OS only)

- ASOMobile — Xiaomi GetApps ASO fields — GetApps indexed fields, including the dedicated keyword field

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy