Indus Appstore: The India-First App Distribution Play

PhonePe's Indus Appstore is the most India-native Android store yet — 100M+ devices, Tier-3 reach, vernacular and voice search, and zero commission on in-app purchases. Here is how it works, how to publish, and where it actually pays off.

What is the Indus Appstore and who is it for?

The Indus Appstore is PhonePe's India-first Android app store — a homegrown alternative to Google Play built around vernacular discovery, Tier-2/3 reach, and a billing model that takes no cut of your in-app revenue. It launched its developer platform in early 2024 and has since become the most credible India-native distribution channel an Android developer can add.

The pitch is straightforward. Google Play is the default on virtually every Android phone in India, but it is built for a global audience, runs an English-first discovery surface, and mandates its own billing with a 15-30% commission on most digital goods. Indus inverts each of those: it is built for India, indexes discovery across a dozen Indian languages, and — per PhonePe's developer-platform announcement — charges zero commission on in-app purchases while letting you plug in any payment gateway you already use.

It is owned by PhonePe, India's largest UPI player, which gives it two structural advantages most alternative stores never get: a payments rail it controls, and the distribution muscle to strike preinstall deals with device makers. The store gained real momentum during the 2024 standoff between Google and Indian developers over Play billing, when several large Indian apps were briefly delisted — an episode Business Standard documented as a turning point for developer interest.

Across our 300+ apps managed since 2013, the question we now field from almost every India-focused client is the same: "Is a second store worth the effort?" For most global apps the honest answer has historically been no. Indus is the first alternative store where, for an India-first product, the answer is frequently yes — and this guide explains exactly when.

How big is Indus Appstore in India in 2026?

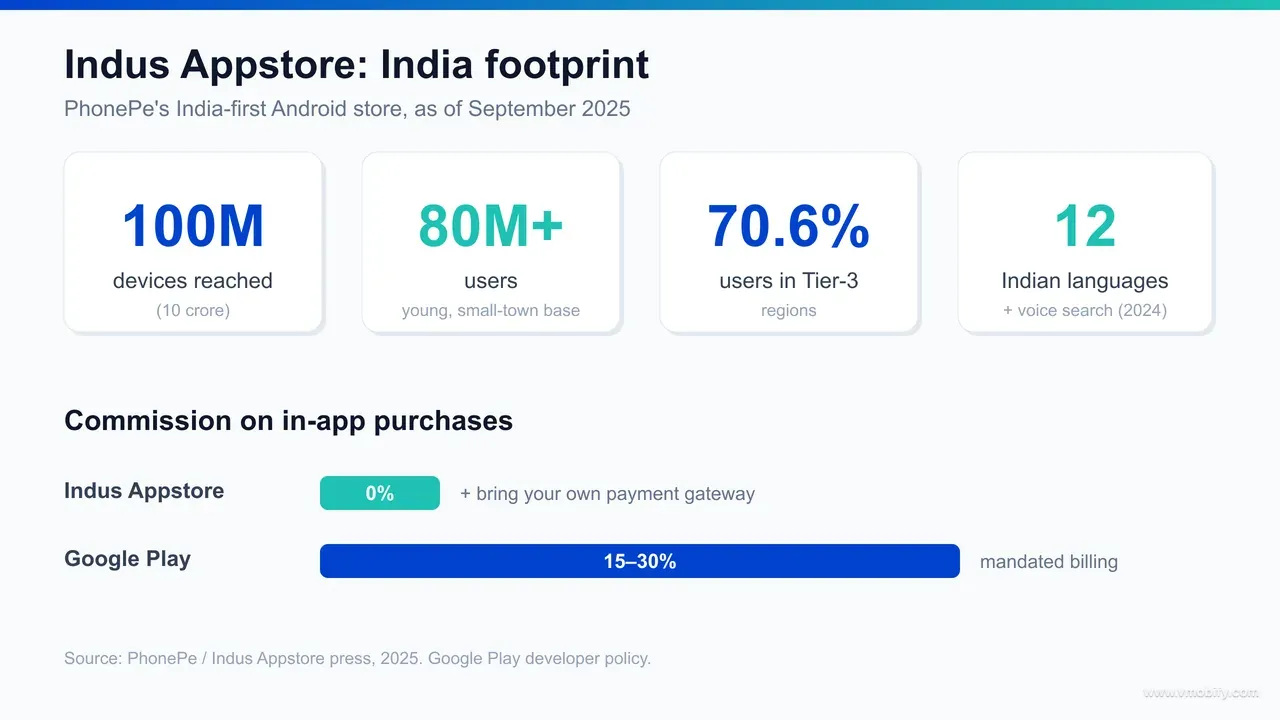

By September 2025, Indus Appstore was live on 100 million (10 crore) devices, serving more than 80 million users, with 70.6% of that base in Tier-3 regions — a footprint no other India-native store comes close to. Those are the numbers PhonePe published in its 10-crore-devices milestone, and the Tier-3 skew is the part that matters most for distribution strategy.

The catalogue had grown to over 500,000 Android apps across categories led by social media, communication, entertainment and finance. The user base is young and small-town: 33.7% are Gen Z (18-27), 93.5% are under 45, and roughly 40% navigate the store in a regional language rather than English. That is a fundamentally different audience profile from the metro-heavy, English-first cohort most Play-optimised listings are written for.

Reach is also a device-channel story, not just an app users download. Indus is preinstalled on Xiaomi and Lava smartphones, and in December 2025 PhonePe announced a partnership with Motorola India to ship it on their devices too. Preinstallation is what separates a viable alternative store from a vanity one — it puts the storefront in front of users who never go looking for it.

For context on where this fits in the wider market, our breakdown of India app install trends in 2026 shows the same pattern across the ecosystem: the next 200 million Indian internet users are overwhelmingly Tier-2/3, vernacular-first, and price-sensitive. Indus is built squarely for them.

What does it cost, and how does billing work?

Indus Appstore charges no commission on in-app purchases and lets you integrate any third-party payment gateway, while listing was free for the first year with only a nominal fee signalled thereafter — the inverse of Google Play's mandated billing and 15-30% cut. This is the headline economic argument, and it is worth being precise about it.

On Google Play, most digital goods must flow through Google Play Billing, which takes 15% on the first $1 million of annual revenue and 30% above it, plus a reduced 15% on subscriptions — terms set out in Google's developer policies. Indus, by contrast, lets you keep that revenue and route payments through a gateway you control — which for an India-focused app usually means UPI, the rail PhonePe itself dominates. For a subscription business, escaping even a 15% platform fee is a direct margin gain that compounds every renewal.

The arithmetic is worth seeing plainly. Take an app processing ₹50 lakh a year in in-app subscriptions. At Play's 15% subscription rate that is ₹7.5 lakh handed to the store annually; at the 30% rate that applies to most one-off digital goods above the threshold, it is ₹15 lakh. On Indus the platform commission on that same revenue is zero — you pay only your own payment-gateway fees, which for UPI are a fraction of a percent. For a business running on thin margins, that recovered commission can be the difference between a sustainable unit economic and a loss-making one, and it grows with every additional rupee of in-app revenue.

One honest caveat on the listing fee: the original free-listing window was framed around the store's first year, and PhonePe has signalled any future fee would be "low single digits, not double digits" rather than a Play-style commission. The exact post-2025 fee schedule is not something we will state as fixed here — confirm the current terms directly on the Indus developer portal before you model unit economics, because this is the kind of detail that changes. What does not change is the structural point: the listing fee, whatever it settles at, is a small fixed cost, while the commission saving is a percentage of all your revenue.

The strategic conclusion holds regardless of the listing fee: the commission structure, not the listing cost, is where the money is. If you run in-app monetisation at any scale in India, the difference between a 0% and a 15-30% take rate on IAP is the single largest line item this decision moves — and it is why a subscription or IAP-led app should run the numbers before dismissing a second store as not worth the effort.

How do you publish an app on Indus Appstore?

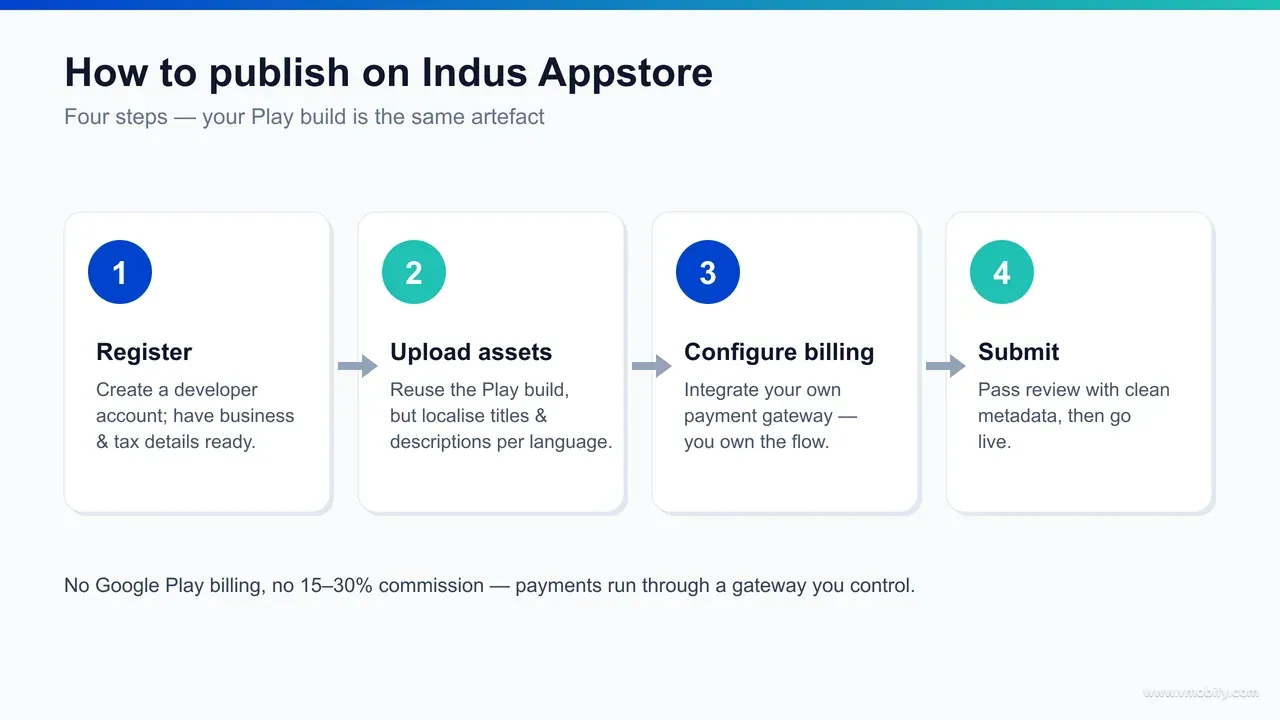

Publishing to Indus follows the same broad shape as any Android store — create a developer account, upload your build and assets, set pricing and your payment gateway, then submit for review — through the self-serve developer console. If you already ship on Google Play, you have everything you need; the APK or App Bundle is the same artefact.

- Register on the developer platform: create an account at the Indus developer portal. PhonePe's UPI footprint means onboarding leans on Indian developer verification — keep your business and tax details ready.

- Upload your build and store assets: reuse your Play build, but do not reuse your Play listing copy verbatim. Indus indexes discovery across Indian languages, so localised titles and descriptions are a ranking lever, not an afterthought (more on this below).

- Configure billing: integrate your chosen payment gateway for any in-app purchases. This is the step that differs most from Play — you own the payment flow rather than handing it to the store.

- Submit for review and publish: the store runs a review before your app goes live. Plan for a review window rather than an instant publish, and treat your first submission the way you would a Play submission — clean metadata, accurate screenshots, no policy edge cases.

Before you submit, run the same pre-flight checks you would for any store: confirm your screenshots reflect the current build, that your content rating and category are accurate, and that your privacy and data-safety declarations match what the app actually does. A young store still rejects sloppy submissions, and a rejection on day one delays the install volume you listed for.

In our portfolio, the teams that get the most from a second store treat the launch as a real listing, not a copy-paste. The half-hour you save by duplicating your Play assets is the half-hour that costs you vernacular discovery — which is the entire reason to be on Indus in the first place. The incremental effort over a Play listing is small; the missed opportunity from treating it as an afterthought is not.

How do vernacular and voice search work?

Indus indexes discovery in English plus 12 Indian languages and added voice search in 10 Indian languages in April 2024 — a vernacular discovery surface that lets a user find your app by typing or speaking in their own language, which Google Play does not replicate in India. For an India-first app, this is the most underrated reason to list.

The store supports app discovery across Assamese, Bangla, Gujarati, Hindi, Kannada, Malayalam, Marathi, Odia, Punjabi, Tamil, Telugu and Urdu, with in-session language switching, per TechPP's launch coverage. With roughly 40% of users navigating in a regional language, an app whose metadata exists only in English is invisible to a large share of the searches happening on the store.

Voice search compounds this. PhonePe's voice-search announcement notes that vernacular speakers make up around three-quarters of India's internet base and that a large majority of smartphone users engage with voice. A user who speaks "cricket score app" in Tamil should land on your app — and that only happens if your listing carries the right vernacular terms.

A concrete example makes the stakes clear. A user searching for a food-delivery app in Hindi may speak "khaana order" rather than the English "food delivery", and a user looking for a learning app in Tamil will use the Tamil word for "study" or "class", not "edtech". If your only indexed keywords are English, every one of those high-intent vernacular searches misses you and surfaces a competitor who localised. On a store where 40% of navigation already happens in a regional language, that is not a rounding error — it is a large share of your addressable demand.

The practical takeaway mirrors how we approach app store optimisation generally: keyword research has to be done per language, not translated word-for-word. The Hindi term a user actually speaks for "money transfer" or "movie tickets" is rarely the literal translation of your English keyword. Treat each language as its own ASO surface — research the real spoken terms, write native titles and descriptions for the languages your audience uses, and revisit them as the store's search data accumulates. That discipline is what turns Indus's vernacular indexing from a feature into installs.

How does it compare to Google Play for Indian developers?

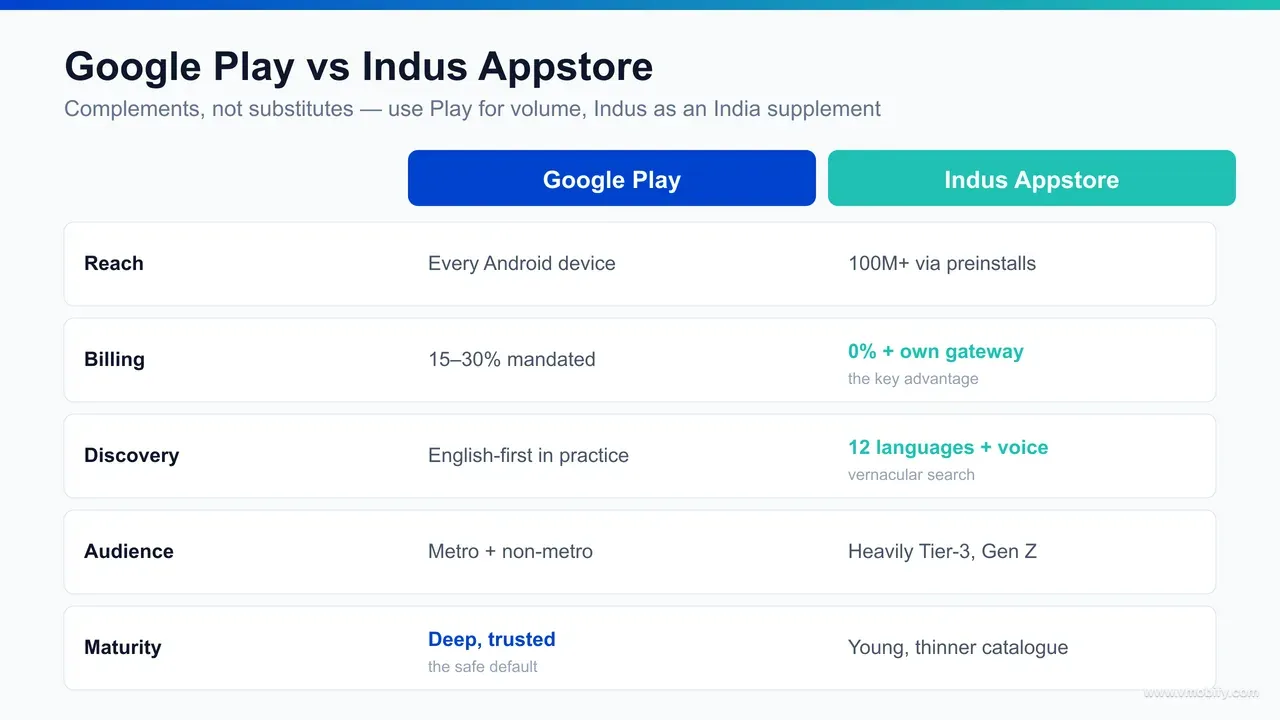

Google Play wins decisively on raw reach and is still where the overwhelming majority of Android installs happen; Indus wins on billing economics, vernacular discovery, and Tier-3 audience fit — which is why the right model is "Play plus Indus," not "Play or Indus." They are complements, not substitutes.

- Reach: Play is on effectively every Android device in India; Indus is on 100M and growing via preinstalls. Play is your volume engine — that does not change.

- Billing: Play mandates its billing with a 15-30% cut; Indus takes nothing on IAP and lets you bring your own gateway. This is Indus's clearest structural advantage.

- Discovery: Play's search is English-first in practice; Indus indexes 12 Indian languages plus voice. For a vernacular audience, Indus surfaces apps Play buries.

- Audience: Play spans metro and non-metro; Indus skews heavily Tier-3 and Gen Z. If that is your user, Indus concentrates them.

- Maturity: Play is a mature, trusted, deeply featured store; Indus is young, with a thinner catalogue and developing tooling. Play is the safer default; Indus is the upside bet.

The honest framing we give clients: keep Google Play as your primary store and your source of install volume, and add Indus as a high-margin, India-native supplement. The work to maintain a second listing is real, but for an India-first app with in-app revenue, the commission savings alone usually justify it before you even count the incremental vernacular installs.

What are the real limitations today?

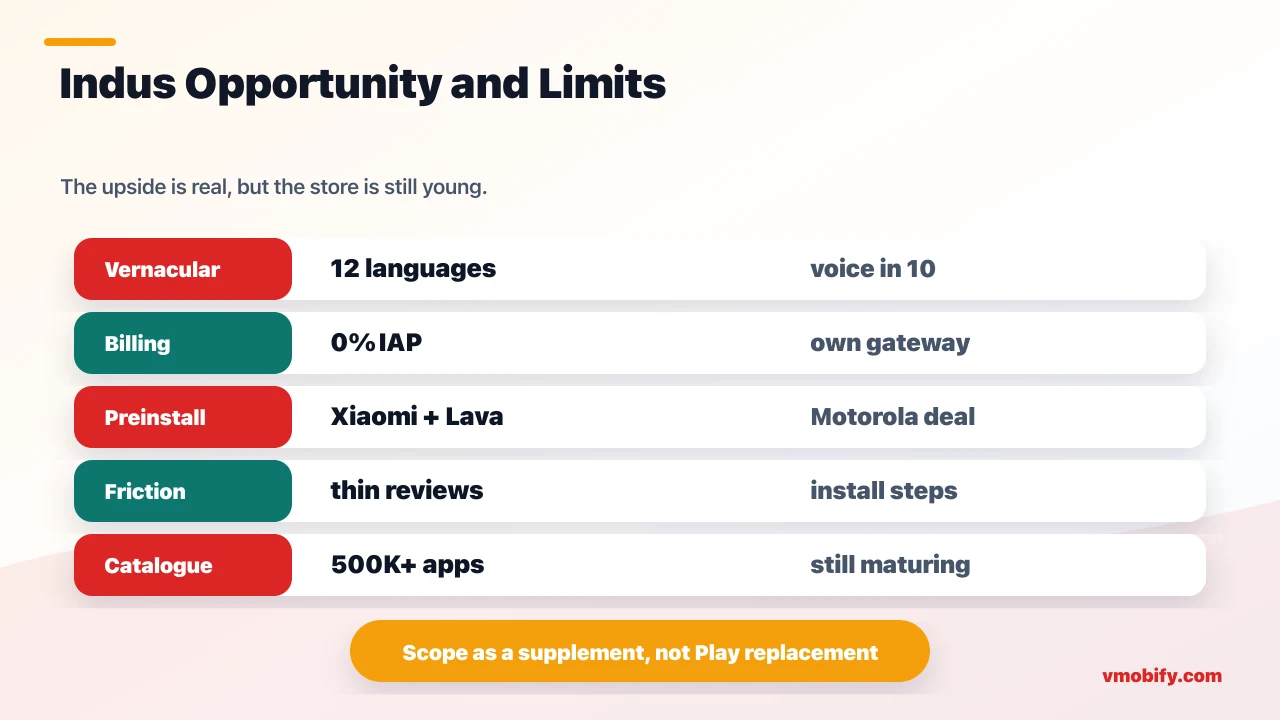

Indus's biggest limitations are update fragmentation, a thin and young review base, install-flow friction, and catalogue gaps — none fatal, but all reasons to treat it as a supplement rather than a primary store. Going in clear-eyed about these is what separates a productive second-store launch from a disappointing one.

- Update routing: users who install from Indus may still be pointed back to the original store for updates, which fragments your update path and complicates version management. This is the most-cited practical friction.

- Thin social proof: a young store means fewer ratings and reviews per app, so the trust signals that help conversion on Play are weaker here. Your listing has to earn the install on its own merits.

- Install friction: first-time installs from any non-default store involve more steps than a one-tap Play install, which costs some conversion at the margin.

- Catalogue gaps: coverage in some categories — gaming, certain OTT and social apps — is still filling in, which affects how often users return to the store organically.

We have seen these frictions matter most for apps that expect Indus to behave like Play on day one. It will not. The teams that succeed scope Indus correctly: a channel to capture commission-free India revenue and vernacular discovery, measured on its own incremental contribution, not held to Play's volume or polish. Set that expectation internally before launch and the limitations become manageable trade-offs rather than surprises.

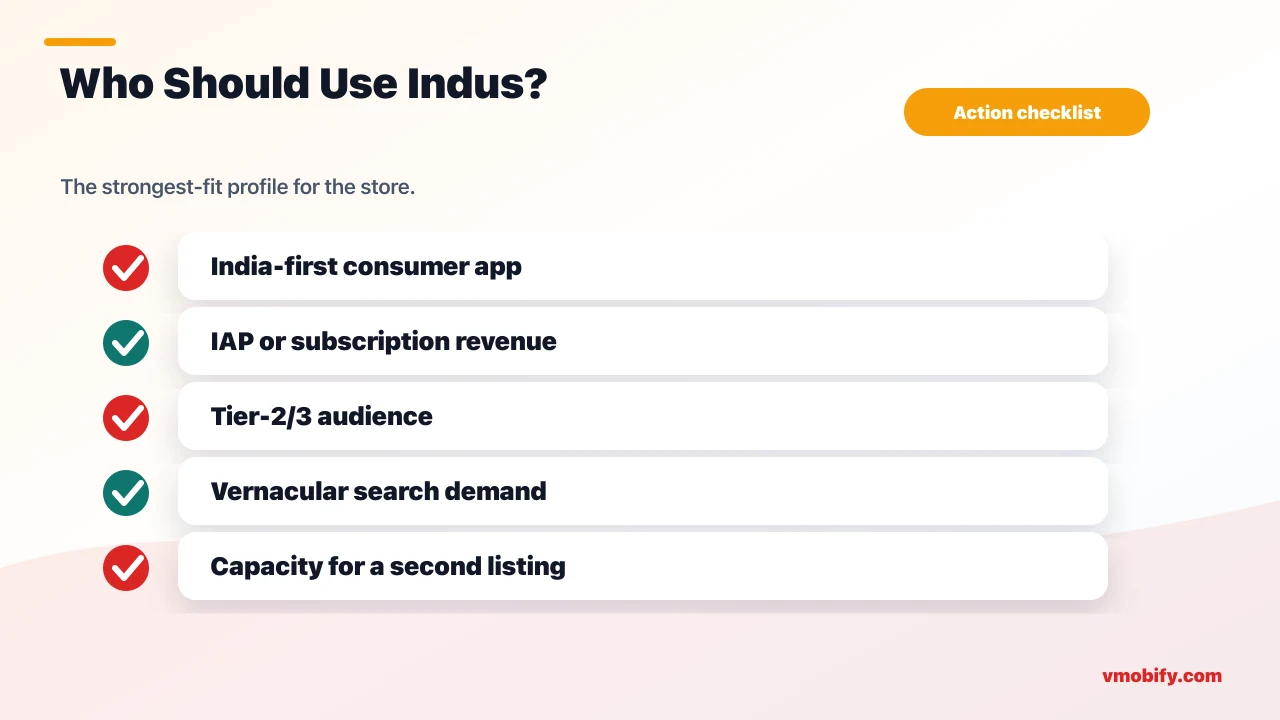

Which apps get the most out of Indus Appstore?

The apps that win on Indus are India-first consumer products with in-app purchases or subscriptions, a vernacular or Tier-2/3 audience, and the operational capacity to maintain a second listing — the more of those that describe you, the stronger the case. If you are a global app with a metro-English audience and no IAP, the upside is thin and Play alone is fine.

Three profiles see outsized returns. First, subscription and IAP-heavy apps, where escaping a 15-30% commission is a direct margin gain on every transaction — fintech, content, and utility apps in particular. Second, vernacular-first apps targeting the next 200 million Indian internet users, where Indus's language and voice discovery actively surfaces you to audiences Play does not. Third, apps already navigating Play-billing tension that want a credible distribution alternative on hand.

Equally important is knowing when not to bother. If your audience is metropolitan, English-comfortable, and you monetise through ads rather than in-app purchases, the commission advantage does not apply to you and the vernacular discovery edge is muted — Google Play alone will serve you fine, and a second listing is overhead you do not need. The decision is not "every app should be on Indus"; it is "India-first, monetised, vernacular apps should run the numbers, because for them the case is unusually strong."

For maximum India device-channel coverage, Indus pairs naturally with the other preinstalled OEM stores — listing on Indus and a Xiaomi-channel store together puts you in front of a large share of India's non-metro Android base that a single store cannot reach. The marginal effort of a second and third listing is small relative to the commission savings and incremental installs for an India-first product.

If you want help deciding whether a multi-store strategy is worth the operational overhead for your specific app — and want it set up and measured properly rather than launched and forgotten — that is exactly the kind of India growth work our ASO team runs, and you can see the outcomes across our case studies or talk to us directly.

Frequently Asked Questions

Is Indus Appstore free for developers?+

Listing was free for the first year, and PhonePe has signalled any future fee would be low single digits rather than a Play-style commission. Critically, it takes zero commission on in-app purchases. Confirm the current listing terms on the Indus developer portal before modelling your economics.

Does Indus Appstore charge commission on in-app purchases?+

No. Indus charges no commission on in-app purchases and lets you integrate your own payment gateway, versus the 15-30% cut Google Play takes through its mandated billing.

How many devices is Indus Appstore on?+

It reached 100 million (10 crore) devices and over 80 million users by September 2025, with 70.6% of users in Tier-3 regions, according to PhonePe.

Which phones come with Indus Appstore preinstalled?+

Xiaomi and Lava devices ship it, and PhonePe announced a Motorola India preinstall partnership in December 2025.

Can I use UPI or my own payment gateway on Indus Appstore?+

Yes. Indus lets you integrate any third-party payment gateway for in-app billing, which for India-focused apps typically means UPI — the rail PhonePe itself dominates.

How does Indus Appstore compare to Google Play?+

Google Play wins on raw reach and maturity; Indus wins on zero-commission billing, vernacular and voice discovery in 12 Indian languages, and Tier-3 audience fit. The best approach is to use both — Play for volume, Indus as a high-margin India supplement.

Do apps update automatically on Indus Appstore?+

Update routing is a known limitation — users may be pointed back to the original store for updates, which fragments version management. Factor this into your release process before listing.

Sources

- Indus Appstore — 10 crore devices milestone — Reach, user base, Tier-3 share and catalogue size (Sept 2025)

- PhonePe — Indus developer platform launch — Zero IAP commission and bring-your-own-gateway billing

- Indus Appstore — voice search in 10 languages — Vernacular voice discovery (launched April 2024)

- PhonePe — Indus x Motorola India partnership — OEM preinstall deal (Dec 2025)

- Business Standard — Indus gains traction amid Google spat — Developer momentum during the 2024 Play-billing dispute

- TechPP — Indus Appstore features and languages — The 12 supported Indian languages and discovery features

- Google Play — Developer content policy — Play Billing requirement and commission structure for comparison

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy