The Mobile App Monetisation Playbook: Ads vs IAP vs Subscriptions

Most apps are free to download, so the revenue question is not 'do we charge?' but 'how?'. This playbook compares the four monetisation models — subscriptions, one-off IAP, in-app advertising, and hybrid — by ARPU, audience fit, and the low-ARPU India reality, then shows how to sequence them as you scale.

How do free apps actually make money?

Almost every app on the store is free to download, so the revenue question is never "do we charge?" — it is "how, and from whom?". Free apps make money by converting a small slice of their users into payers, or by selling those users' attention to advertisers, or both at once. The download price is a customer-acquisition decision; the real monetisation happens after install.

This matters because the economics of mobile are brutally top-heavy. Across the freemium market, only around 3-8% of users ever pay for anything — a free tier or an ad load carries the other 92-97%. So when you choose a monetisation model, you are really making two decisions at once: how to extract meaningful revenue from a thin layer of high-intent users, and how to keep the large non-paying majority engaged enough to be worth either upgrading later or showing ads to now.

There are four building blocks, and every business model on the store is some combination of them: subscriptions (recurring access for a fee), one-off and consumable in-app purchases (pay per item, level, or feature), in-app advertising (you sell attention, not features), and hybrid (two or more of the above running together). A paid up-front download is technically a fifth, but it is now a rounding error outside a few premium niches — the store norm is free-to-install with monetisation layered on after.

It helps to think of the choice as picking a default revenue source for each layer of your user base rather than one model for the whole app. The top sliver of high-intent users can carry a subscription or repeat IAP; the broad middle can be nudged toward a one-off unlock; the long tail that will never pay can still generate ad revenue or, just as valuably, organic growth through referrals and reviews. Framed that way, the question stops being "which model?" and becomes "which model for which layer, and in what order do we switch them on?" — which is what the rest of this playbook answers, section by section.

Across our 300+ apps managed since 2013, the single most expensive mistake we see is not a weak paywall or a low ad fill rate — it is choosing a model that fights the product. An ad model bolted onto a high-intent utility that users open twice a week will never earn what a subscription would; a subscription forced onto a casual game with no recurring value will starve. This playbook is the decision framework we use to get that choice right before a line of monetisation code is written, and a hub for the deeper guides on each model. If you want that decision made and instrumented properly for your app, that is the core of our app monetisation service.

What are the four app monetisation models, compared?

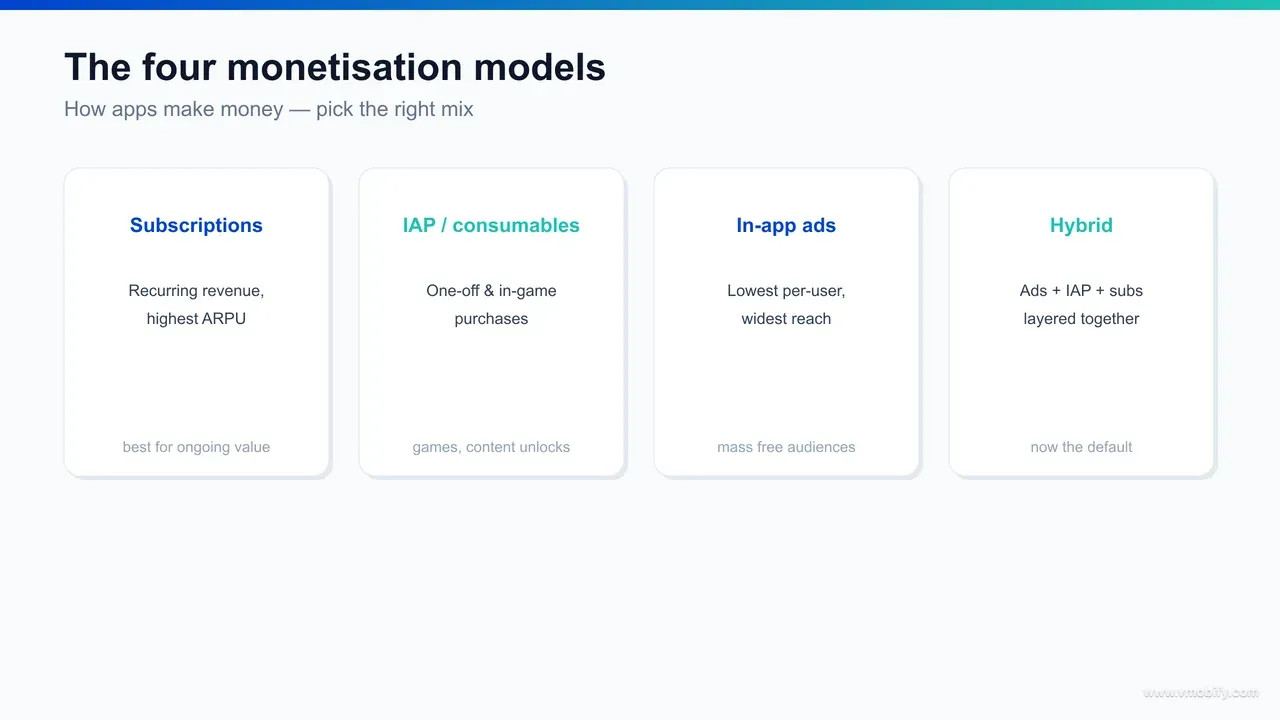

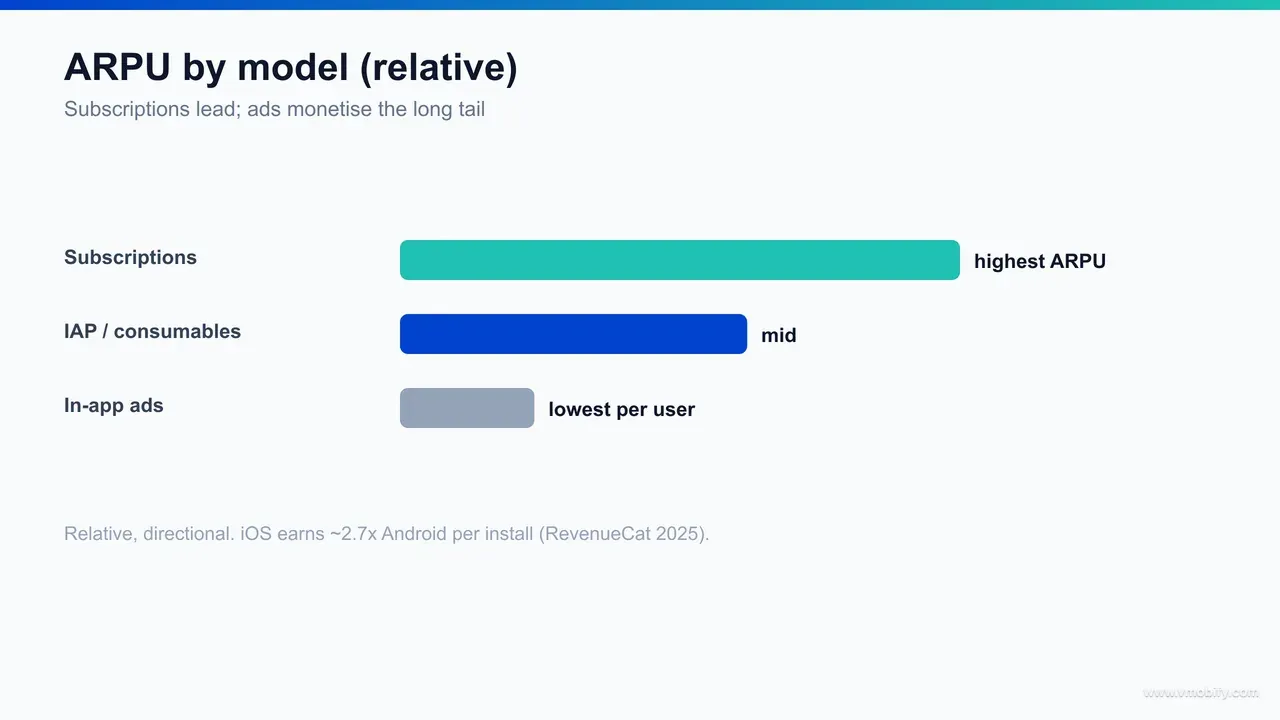

Subscriptions produce the highest revenue per user, in-app advertising the lowest per-user but by far the widest reach, consumable IAP a small but extremely high-value spender tier, and hybrid blends them to capture the whole spend curve at once. Each model trades reach against revenue-per-user differently, and that trade-off is the heart of the decision.

- Subscriptions: recurring payments for ongoing access — streaming, fitness, productivity, news. Highest ARPU of any single model because revenue compounds with each renewal, but the addressable base is the smallest because most users will not commit to a recurring charge.

- One-off and consumable IAP: pay-per-item — game currency, extra lives, a one-time feature unlock, a content pack. Revenue is concentrated in a tiny "whale" tier that spends repeatedly, with a long tail of users who never buy. Very high ceiling, very low conversion.

- In-app advertising: you monetise attention by showing banner, interstitial, native, or rewarded-video ads. The lowest revenue per user of any model, but it monetises everyone — including the 92-97% who will never pay — so it scales with raw reach and session time.

- Hybrid: ads on the free base, IAP and subscriptions on the engaged top. The default in modern gaming and increasingly in consumer apps, because it stops leaving money on the table at both ends of the spend curve.

The general rule, well documented in Business of Apps' monetisation guide, is that subscriptions and IAP maximise revenue per paying user while ads maximise reach. No model wins on both axes — which is exactly why hybrid has become so common. In our portfolio, the apps that plateau early almost always picked a single model and defended it past the point of sense; the ones that compound revisit the mix as their audience grows.

How do you choose a model by app type and audience?

Match the model to how often your app delivers value and to how much your audience can pay: recurring-value apps suit subscriptions, session-based entertainment suits ads or consumable IAP, and price-sensitive mass-market audiences almost always need an ad-led base whatever else sits on top. Usage pattern and willingness-to-pay are the two variables that decide it.

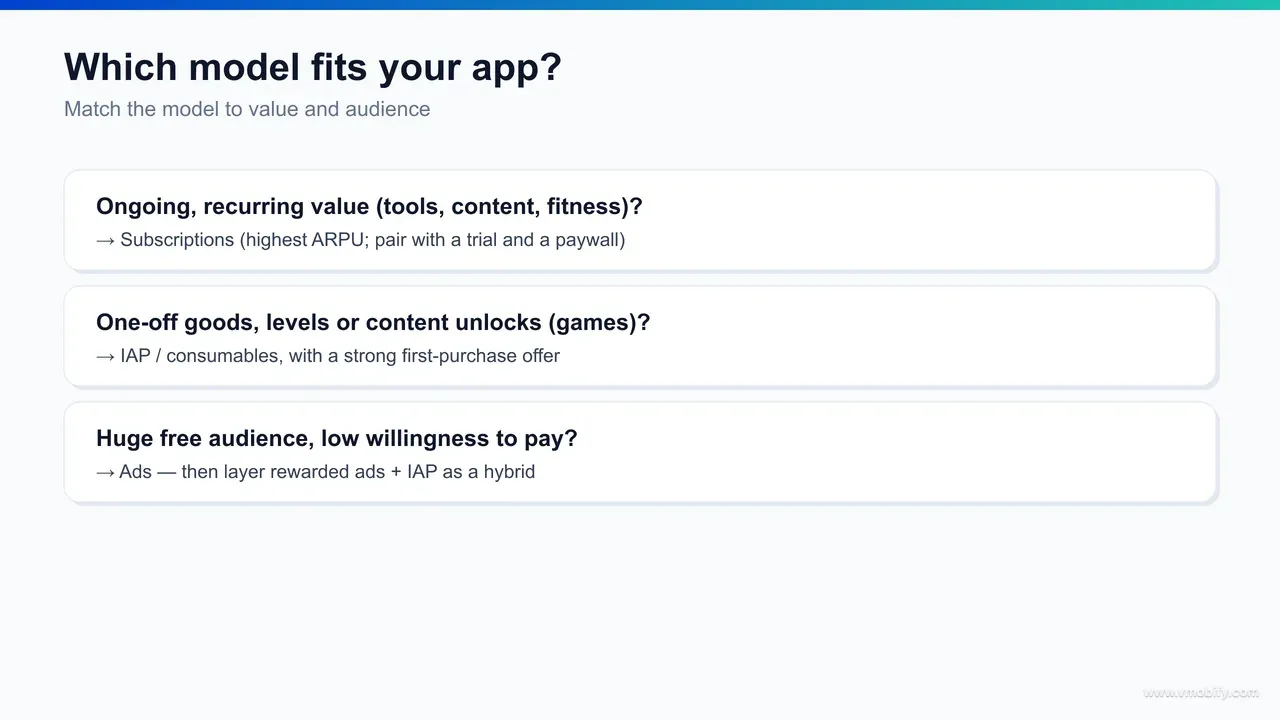

Start with the usage question. If your app delivers value repeatedly and continuously — a fitness coach you open daily, a news app you read every morning, a productivity tool tied to your workflow — recurring value justifies a recurring charge, and subscriptions fit. If your app delivers value in discrete sessions or bursts — a casual game, a photo editor, a one-off utility — users resist a standing charge, and ads or per-item IAP fit better because they monetise the moment of use without asking for commitment.

Then layer in audience ability-to-pay. A productivity app aimed at Western professionals can lead with a subscription at $9.99/month and expect a healthy conversion. The same app aimed at a mass-market Indian audience cannot — the willingness and ability to pay a recurring Western price simply is not there at scale, so the base has to be ad-monetised with a thin premium tier on top. This is not a small adjustment; it changes which model is even viable, and we cover the specifics in the India section below.

A quick way to sanity-check your instinct: write down what fraction of your users would pay anything, and how often your app earns the right to charge them. If both numbers are high, lead with subscriptions. If conversion is low but session volume is huge, lead with ads. If a tiny minority will spend a lot repeatedly, build for consumable IAP. Most real apps land between these, which is the case for hybrid. When we scope a new client's model, this two-axis read — usage frequency against willingness-to-pay — is the first thing we map before touching pricing.

How do subscriptions work as a monetisation model?

Subscriptions charge users a recurring fee — usually monthly or annual — for ongoing access to premium features or content, and they produce the highest lifetime value of any model because revenue compounds with every renewal rather than ending at a single transaction. They are the model with the best long-term economics and the hardest to start.

The reason LTV is so high is renewal. A user who pays $9.99/month and stays 18 months is worth roughly $180 — far more than any one-time purchase — and the cost to serve them barely moves. That compounding is why investors and operators prize subscription apps, and why the RevenueCat State of Subscription Apps 2025 report has become the de facto benchmark for the category. But the same mechanic that makes subscriptions powerful makes them unforgiving: every renewal is a fresh churn risk, so retention is the business, not a side metric.

The decisions that make or break a subscription are not the price tag — they are paywall placement, trial length, and the annual-versus-monthly split. Place the paywall after the user has felt the product's value (the "aha moment"), not on first open, and conversion typically multiplies. Offer annual plans at roughly two months' discount and a large share of revenue shifts to the higher-LTV, lower-churn annual cohort. These levers each deserve their own treatment, which is why this is a hub: we go deep on the full stack in our subscription monetisation strategy guide, and on the paywall screen specifically in our paywall optimisation benchmarks.

One under-appreciated point: subscriptions only work if you can actually collect recurring payments, and that varies wildly by market. In the West, stored cards on the App Store and Play Store handle it invisibly. In India, card-on-file recurring mandates are friction-heavy, and UPI AutoPay is what makes recurring collection viable at all — a market-specific detail we cover in our price localisation guide. Pick subscriptions where the value is genuinely recurring and the payment rail can support renewals; otherwise you will win the first charge and lose every one after it.

How do one-off and consumable in-app purchases work?

In-app purchases let users buy individual items — durable feature unlocks that they keep, or consumables like game currency and boosts that are used up and re-bought — and the model lives or dies on a tiny tier of repeat spenders, the so-called whales, rather than broad conversion. It has the highest revenue ceiling per user of any model and the lowest conversion rate.

There are two distinct flavours, and they behave very differently:

- Durable (non-consumable) IAP: a one-time purchase the user keeps forever — removing ads, unlocking a pro feature, buying a content pack. Predictable, low-friction, but each user can only buy it once, so it does not compound.

- Consumable IAP: items that deplete and must be repurchased — coins, gems, extra lives, energy refills. This is where the revenue ceiling is, because a committed player can buy the same pack hundreds of times. The flip side is that the spend is concentrated in a fraction of a percent of users.

The economic shape is what makes consumable IAP unusual. In a typical free-to-play game, a single-digit percentage of players spend at all, and within that, a fraction of a percent — the whales — drive the majority of revenue. Apple's In-App Purchase and Google Play's in-app billing systems both handle the mechanics, but the design challenge is entirely yours: building an economy that gives the free majority a good experience while offering high-spenders enough to keep buying, without tipping into pay-to-win resentment that drives everyone else away.

Consumable IAP is the right lead model when your app has a built-in economy or progression loop — games, above all, but also some creator and social apps with virtual goods. It is the wrong lead model for a utility or content app, where there is no natural item to consume and the right structure is a durable unlock or a subscription. In our portfolio, the IAP apps that scale are the ones that treat the in-app economy as a product in its own right, tuned continuously, not a price list set once at launch.

Because the revenue is so concentrated, the metric that governs an IAP business is not conversion rate but the spend distribution behind it — how many whales you have, how often they buy, and how long they stay before they burn out. A game can have a perfectly healthy conversion rate and still collapse because its top spenders churned and were never replaced. The operational discipline, then, is segment-level: identify high-spenders early, give them reasons to keep progressing, and watch the re-purchase interval the way a subscription business watches renewals. The IAP model rewards the teams that instrument their economy as carefully as a subscription team instruments its churn cohort, and starves the ones that ship a static store and hope.

How does in-app advertising work?

In-app advertising monetises attention rather than features — you show ads and get paid per impression or per action — and while it earns the least per user of any model, it is the only one that monetises the entire base, including the overwhelming majority who will never pay a rupee or a dollar. Reach is its whole advantage.

The main ad formats sit on a clear spectrum of revenue versus intrusiveness:

- Banner ads: small, persistent, low revenue per impression, low disruption. Fine as a background earner, never a primary engine.

- Interstitial ads: full-screen ads at natural breaks (between levels, between articles). Higher revenue, but mistimed interstitials are the fastest way to crater retention.

- Rewarded video: the user opts in to watch an ad in exchange for an in-app reward. The best-performing format in most apps because it is consent-based — users choose it, so it lifts revenue without the retention penalty of forced ads.

- Native ads: ads styled to match your content feed. Higher engagement, lower disruption, but they demand careful labelling to stay trustworthy.

The number that governs ad revenue is eCPM — effective revenue per thousand impressions — and it varies enormously by geography. A US impression can be worth many times an Indian one, which is the single biggest reason ad-led apps with large Indian audiences post low ARPU despite huge install bases. Mediation platforms that auction each impression across multiple ad networks are how mature publishers squeeze the most out of every view; Adjust's measurement resources are a good grounding in how ad monetisation and attribution interlock.

Lead with ads when you have scale and session time but low willingness-to-pay — casual games, content browsers, mass-market utilities, and almost any consumer app whose base skews toward price-sensitive markets. The discipline that separates good ad monetisation from bad is restraint: protect the early sessions, gate disruptive formats behind engagement, and lean on rewarded video so the ad load feels like a choice rather than a tax. Push ad density too hard and you trade short-term eCPM for long-term churn — a trade that almost never pays.

What is hybrid monetisation and why is it now the default?

Hybrid monetisation runs two or more models in the same app — typically ads on the free base, plus IAP or subscriptions for the engaged top — and it has become the default in mobile gaming and is spreading fast to consumer apps because no single model captures the full spread of how different users want to pay. It is less a model than an acknowledgement that your user base is not monolithic.

The logic is straightforward once you accept the spend curve. A pure subscription app leaves the 92-97% who will not subscribe completely unmonetised. A pure ad app leaves the small minority who would happily pay to remove ads or unlock premium features earning you a few cents in impressions instead of dollars in IAP. Hybrid closes both gaps: the free majority generates ad revenue, the willing minority converts to IAP or a subscription, and a common option — "subscribe to remove ads" — even turns the ad experience itself into a conversion lever toward higher-value revenue.

Adjust's analysis of hybrid monetisation documents how gaming moved here first, with the majority of top-grossing games now blending ads and IAP rather than choosing. The pattern is now crossing into non-gaming: a fitness app might run ads on free workouts, sell a one-off programme pack, and offer an all-access subscription, all at once. The reason it works is that it stops forcing every user into the same payment behaviour and instead meets each segment where it is.

The catch is complexity. Hybrid means more SDKs, more measurement surface, and real design tension — ads can cannibalise IAP if a user can simply watch a rewarded video for what you also sell, and an aggressive ad load can suppress the goodwill that drives subscriptions. Done carelessly, the models compete; done well, they sequence — ads warm up the base, IAP captures intent, subscriptions lock in the committed. We treat the interactions explicitly in our dedicated hybrid monetisation guide; the headline is that hybrid is the right answer for most apps at scale, but only if you design the boundaries between the models deliberately.

How do iOS, Android, and India change the monetisation maths?

Platform and geography quietly decide whether a paid model is even viable: iOS earns roughly 2.7x what Android earns per install, and India inverts the whole equation toward an ad-led base with a thin premium top tier collected over UPI rather than the subscription-first model that works in the West. The same app can be a healthy subscription business in one market and an ad business in another.

The platform gap is stark. Per the RevenueCat 2025 benchmark, iOS generates about $0.38 in day-60 revenue per install against roughly $0.14 on Android — a multiple of about 2.7x. iOS users skew higher-income and have stored payment credentials they actually use, so subscription and IAP conversion runs ahead of Android almost everywhere. The practical consequence: if your install mix is Android-heavy, a subscription-led model has to clear a much lower revenue-per-user bar to break even, and ads often have to carry more of the load.

India compresses this further. ARPU is low by global standards across both platforms, the install base is overwhelmingly Android, and willingness to pay a recurring Western price is concentrated in a thin metro top layer. The model that works at scale is therefore ad-led monetisation across the base, with a premium IAP or subscription tier sized for the minority who will pay — not a subscription-first model imported wholesale from the US. The advertising rate (eCPM) on Indian impressions is also lower, so the strategy is volume and session time, not premium pricing.

Two India-specific mechanics make the premium tier collectible at all. First, PPP pricing — a subscription priced at ₹299/month rather than the $9.99 equivalent of roughly ₹830 — lifts conversion materially without cannibalising higher-value markets, the subject of our price localisation playbook. Second, UPI AutoPay is what makes recurring collection actually work when card mandates are friction-heavy. Across our India-focused work, the teams that win do not weaken their global model — they run a genuinely different one for India: ads first, a localised premium tier second, and payment rails chosen for the market.

How should you sequence monetisation as you scale?

Do not turn on every model at launch — sequence them: prove retention first, introduce the model that best fits your core value once usage data is real, then layer in additional models as your base grows and segments into payers, spenders, and ad-supported free users. Monetisation that arrives before retention kills the very growth it is meant to fund.

- Phase 1 — earn the right to monetise. Before any paywall or ad, prove that users come back. If day-7 and day-30 retention are weak, no monetisation model will save the app; you are just extracting from a leaking bucket. Fix the product loop first.

- Phase 2 — introduce one model that fits the core value. Add the single model your usage pattern points to — a subscription for recurring-value apps, ads or IAP for session-based ones. One model, instrumented properly, beats three models bolted on at once that you cannot read.

- Phase 3 — layer in a second model as segments emerge. Once you can see distinct cohorts — a willing-to-pay minority, a high-spend whale tier, a large ad-tolerant base — add the model that captures the segment you are currently leaving unmonetised. This is the move into hybrid, and it should be driven by data you now have, not a guess.

- Phase 4 — optimise the mix continuously. At scale, monetisation is never "done". Paywall placement, ad load, trial length, and the boundary between ads and IAP all get tuned against live cohorts, because the optimal mix drifts as your audience and markets change.

A useful way to hold the sequence in mind is that each phase changes what question you are allowed to ask of the data. In phase one the only question is "do they come back?". In phase two it becomes "will they pay for the core value, and at what price?". By phase three you can finally ask "which segment am I under-monetising?" — a question that is meaningless until you have payers and non-payers to compare. Skipping phases does not just risk revenue; it produces numbers you cannot interpret, because you never isolated the variables. The teams that move fastest are not the ones that monetise earliest — they are the ones whose phases are clean enough that every reading actually means something.

The most common sequencing error we see across our 300+ apps is monetising too aggressively, too early — stacking interstitials and a hard paywall onto an app that has not yet proven anyone wants to come back. The second most common is the opposite: a beloved app with strong retention that never builds a second revenue stream and caps its own ARPU for years. Sequencing is the discipline that avoids both — and getting the order and timing right for a specific app is exactly what our monetisation team is engaged to do.

Which monetisation metrics should you track?

The metrics that actually run a monetisation strategy are ARPU, ARPPU, conversion rate, and LTV — measured against your blended user acquisition cost — because they tell you not just how much you earn, but whether you can profitably buy more users. Revenue alone is a vanity number; these ratios are the business.

- ARPU (average revenue per user): total revenue divided by all users, payers and non-payers. The headline efficiency number for the whole base, and the one most distorted by platform and geography mix.

- ARPPU (average revenue per paying user): revenue divided only by payers. This separates "we have few payers who spend a lot" from "we have many payers who spend a little" — two very different businesses that share an ARPU.

- Conversion rate: the share of users who pay at all — typically that thin 3-8% in freemium. Small absolute movements here swing total revenue more than almost any pricing change.

- LTV (lifetime value): total revenue a user generates before they churn. The number that, set against acquisition cost, decides whether growth is profitable or a treadmill.

The relationship that matters most is LTV against CAC (customer acquisition cost). If a user is worth more over their lifetime than it costs to acquire them, you have a growth engine and can spend into it; if not, every install loses money and scale makes the problem worse. Every monetisation decision in this playbook ultimately feeds this one ratio. We have collected the category benchmarks — what good ARPU, ARPPU, and LTV look like by vertical and platform — in our ARPU and LTV benchmarks guide, so you can see where your numbers sit against comparable apps.

Which monetisation pitfalls cost teams the most?

The costliest monetisation mistakes are picking a model that fights the product, monetising before retention exists, copying a Western model into a low-ARPU market unchanged, and letting ads cannibalise the IAP and subscription revenue they were meant to complement. None of these show up as a single bad day — they quietly cap revenue for years.

- Model-product mismatch: forcing a subscription onto a casual game, or running ads on a high-intent professional tool whose users would gladly pay. The fix is the usage-frequency-versus-willingness-to-pay read from earlier — do it before you build, because reversing it later means rebuilding the product around a new model.

- Monetising before retention: hard paywalls and heavy ad loads on an app no one comes back to. You extract a little from a churning base and suppress the engagement that would have grown it. Prove retention first, always.

- Importing the model unchanged into India: a $9.99 subscription-first model dropped into a market with low ARPU, an Android-heavy base, and card-mandate friction. It earns a fraction of what an ad-led base with a localised premium tier and UPI AutoPay collection would.

- Ad-IAP cannibalisation: in hybrid apps, offering a rewarded video for the same thing you sell, or an ad load so heavy it sours users on the subscription that removes it. The models have to sequence, not compete.

- Over-optimising one metric: chasing eCPM or short-term conversion while retention quietly bleeds. The base that pays you next year is the one you protect today.

In our portfolio, the recurring lesson is that monetisation is a product decision, not a billing decision — the apps that win treat the model, the pricing, and the payment rail as core product surface, tuned continuously against live cohorts. If you would like that framework applied to your specific app, market, and platform mix, that is precisely the work we do — talk to our team and we will map the right model and sequence before you commit to one.

Frequently Asked Questions

What is the best monetisation model for a mobile app?+

There is no single best model — it depends on usage frequency and audience willingness-to-pay. Recurring-value apps suit subscriptions, session-based entertainment suits ads or consumable IAP, and most apps at scale end up hybrid. Match the model to how your app delivers value, not to what earns most in the abstract.

How do free apps make money?+

Free apps convert a thin slice of users into payers through subscriptions or in-app purchases, sell the attention of the non-paying majority through ads, or combine both in a hybrid model. Only about 3-8% of freemium users ever pay, so the free tier or ad load is what monetises everyone else.

Which model earns the most revenue per user?+

Subscriptions produce the highest revenue per user because revenue compounds with every renewal. Consumable IAP has the highest ceiling thanks to a small tier of high-spending whales, while in-app advertising earns the least per user but monetises the entire base.

Why is in-app advertising still worth it if it pays so little per user?+

Because it monetises the 92-97% of users who will never pay anything. Ad revenue scales with reach and session time, so for a large, price-sensitive base — common in India — an ad-led model can out-earn a subscription that only a tiny minority would buy.

How does monetisation differ in India?+

India has low ARPU, an Android-heavy base, and card-mandate friction, so the workable model is ad-led across the base with a thin premium IAP or subscription tier. PPP pricing lifts conversion, and UPI AutoPay is what makes recurring subscriptions actually collectible.

What is hybrid monetisation and should I use it?+

Hybrid runs ads on the free base plus IAP or subscriptions on the engaged top, capturing the full spend curve instead of leaving money on the table at either end. It is now the default in gaming and worth adopting at scale — but only once you can design the boundaries so ads do not cannibalise paid revenue.

What does Vmobify do on app monetisation?+

We choose and sequence the right model for your app, market, and platform mix, then instrument and optimise ARPU, ARPPU, conversion, and LTV against acquisition cost. It is the core of our monetisation service at /services/monetization, backed by results across 300+ apps managed since 2013.

Sources

- RevenueCat — State of Subscription Apps 2025 — ARPU and LTV benchmarks, iOS-vs-Android revenue gap (D60 $0.38 vs $0.14)

- Business of Apps — App monetisation models — Comparison of subscriptions, IAP, advertising and paid models

- Adjust — Hybrid monetisation — How gaming moved to ads-plus-IAP and why it is now the default

- Apple — In-App Purchase — Official IAP and subscription mechanics on iOS

- Google Play — In-app billing and subscriptions — Android in-app billing and subscription policy

- Adjust — Measurement and monetisation resources — Ad monetisation, eCPM and attribution grounding

- AppsFlyer — App marketing performance index — CPI and revenue benchmarks by category and geography

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy