Fintech App Marketing in India: UPI, Lending & Wealth Apps

India's fintech market is a ₹65B+ opportunity with regulatory rules that make or break every campaign. This guide covers UPI acquisition triggers, SEBI/RBI/IRDAI compliance for creatives, CPI benchmarks by sub-vertical, and the vernacular ASO edge that most growth teams leave untapped.

Why Is India the Most Complex and Most Rewarding Fintech App Market in 2026?

India is simultaneously the world's largest greenfield fintech opportunity and its most regulation-dense app marketing environment — and the teams that understand both dimensions win disproportionately. The country's fintech market has crossed $65 billion in addressable revenue and is growing at a compound rate that outpaces every other major economy. Smartphone penetration continues to climb, 4G/5G coverage now reaches Tier 3 districts, and a population that largely skipped desktop banking has adopted mobile-first financial services as its primary interface with the formal economy.

The numbers are extraordinary. NPCI's official UPI statistics show 18.7 billion UPI transactions processed in March 2026 alone — a figure that would have seemed implausible five years ago. Every one of those transactions is a user actively engaged with their mobile financial life, and every one is an acquisition signal for fintech apps positioned correctly.

Yet the same market that offers this scale imposes compliance requirements that routinely sink well-funded campaigns. SEBI's investor education and protection framework, RBI's master circulars on digital lending, and IRDAI's insurance marketing regulations each impose distinct creative rules. Ads rejected for compliance violations are not just lost impressions — they delay campaigns by days and can attract regulatory scrutiny if patterns repeat.

Across our portfolio of 300+ apps managed since 2013, fintech is the vertical where the gap between teams that understand the regulatory and cultural context and teams that do not is widest. The reward for getting it right is enormous; the penalty for getting it wrong is steep. This guide covers both dimensions in full.

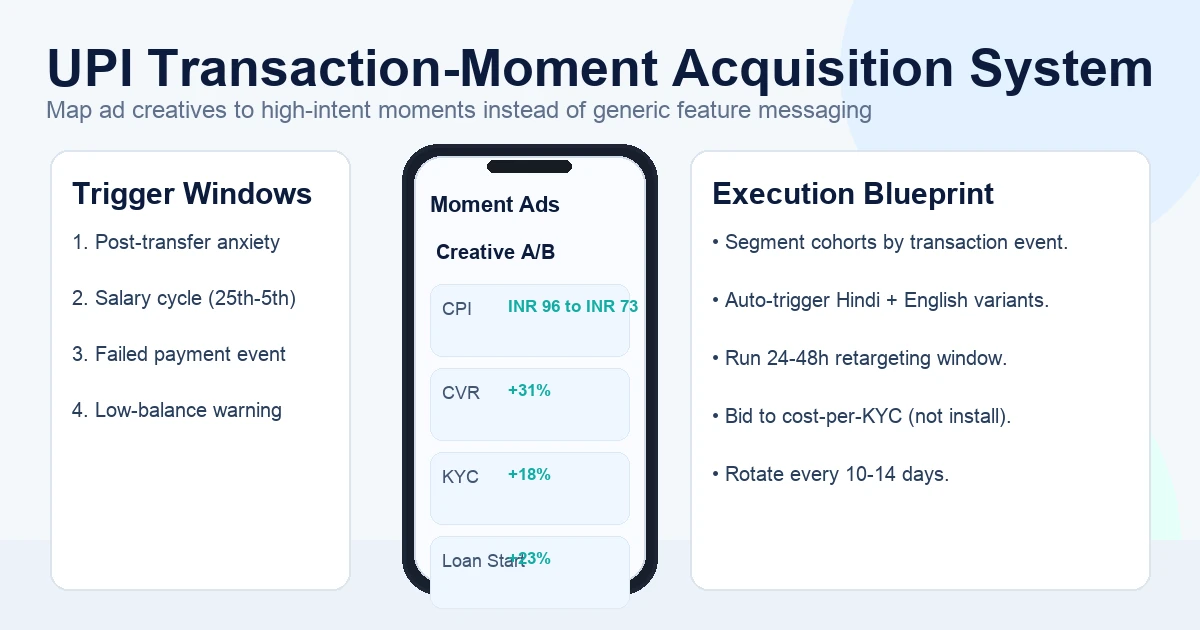

How Do UPI Transaction Moments Drive Fintech App Installs?

The most powerful acquisition frame in Indian fintech is not a feature — it is a moment: the precise transaction context in which a user realises they need a better financial tool than the one they currently have. UPI has trained hundreds of millions of Indians to think about money in micro-moments: splitting a restaurant bill, paying a kirana store, sending rent to a landlord. Each of those micro-moments is an entry point for the right fintech app if your campaign is structured to intercept it.

The three highest-converting UPI acquisition triggers we have observed across our portfolio:

- Post-transfer anxiety: Users who have just completed a large UPI transfer (above ₹10,000) are highly receptive to wealth management and fixed-deposit apps. Retargeting these users via MMP cohorts in the 24–48 hours post-transfer consistently outperforms cold audiences by 2–3× on conversion to first investment.

- Month-end salary cycle: The 25th–5th window every month sees a spike in searches for "best savings app," "fixed deposit app," and "mutual fund SIP." Scheduled budget pushes in this window produce 15–25% lower CPI versus the rest of the month for wealth and lending apps.

- Failed payment moments: Users who encounter a UPI payment failure are acutely aware of limits, credit access, and liquidity. Lending app campaigns targeting keywords and in-app placements around payment failure contexts see above-average first-loan activation rates.

Structuring campaigns around these triggers requires two capabilities: an MMP integration that passes transactional signals to your ad platforms (AppsFlyer, Adjust, or Singular with proper event taxonomy), and a creative library segmented by moment rather than by feature. A creative that says "Low on balance? Get instant credit in 2 minutes" outperforms a generic feature-list creative by 3–5× in lending verticals across our in-portfolio tests.

For broader acquisition strategy across the Indian market, see our guide on user acquisition services and our deep-dive on India app install cost benchmarks.

What Are the SEBI, RBI, and IRDAI Compliance Rules That Govern Fintech App Creatives?

Every fintech app creative in India operates under at least one regulatory framework — and most operate under two or three simultaneously, each with specific disclosure requirements that Google and Meta's policy teams actively enforce. Understanding these rules is not optional; it is the single most important operational skill for any team running paid fintech campaigns in India.

Quick scan checklist before you submit any ad:

- Include the right registration/licence disclosure for your sub-vertical.

- Avoid wording that implies guaranteed outcomes or hides pricing/coverage terms.

- Keep every disclaimer legible on mobile (size, contrast, and placement).

SEBI Rules (Investment & Broking Apps)

- No guaranteed returns: Any creative language implying guaranteed, assured, or fixed investment returns is explicitly prohibited under SEBI's advertising guidelines. This includes phrases like "earn 15% guaranteed" or "assured returns on your portfolio."

- Mandatory registration number: All advertising materials for SEBI-registered entities must display the SEBI registration number. Omitting it is grounds for immediate ad rejection by Google and Meta's fintech policy reviewers. See SEBI's investor protection guidelines for the full disclosure framework.

- Past performance disclaimer: Any creative showing historical returns must include the standard "past performance is not indicative of future results" disclaimer in legible type — not white-on-white or sub-8px.

RBI Rules (Lending Apps)

- NBFC licence disclosure: Lending apps must disclose their NBFC (Non-Banking Financial Company) licence number or their lending partner's NBFC details in all creatives. Apps that obscure this information have faced suspension from both stores and regulatory action from RBI.

- No misleading interest rate claims: Per RBI's master circular on fair lending practices, interest rates must be expressed as annual percentage rates (APR) rather than monthly rates presented in a way that conceals the true cost of credit. "1% per month" without annual equivalent disclosure is non-compliant.

- KYC and consent language: Creatives for apps that collect financial KYC data must not imply instant approval without KYC, as this misrepresents the actual user journey and triggers high-intent abandonment when reality doesn't match expectation.

IRDAI Rules (Insurance Apps)

- Policy exclusions must be disclosed: IRDAI's insurance advertising guidelines require that key policy exclusions be included in creatives or clearly linked. A health insurance ad that shows a ₹5 lakh cover without disclosing pre-existing condition exclusions violates these rules.

- Regulatory approval reference: Insurance product advertisements must reference that the product is approved by IRDAI, typically via the IRDAI registration number of the insurance company.

- No fear-based exploitation: Creatives that use exaggerated fear tactics around death, illness, or financial catastrophe without substantiation are rejected by IRDAI's monitoring framework.

The operational implication: build a compliance checklist into your creative brief template. Every single fintech creative should be reviewed against the relevant regulatory checklist before it enters the ad platform review queue. Rejected creatives reset campaign learning windows and cost you 24–72 hours of campaign performance.

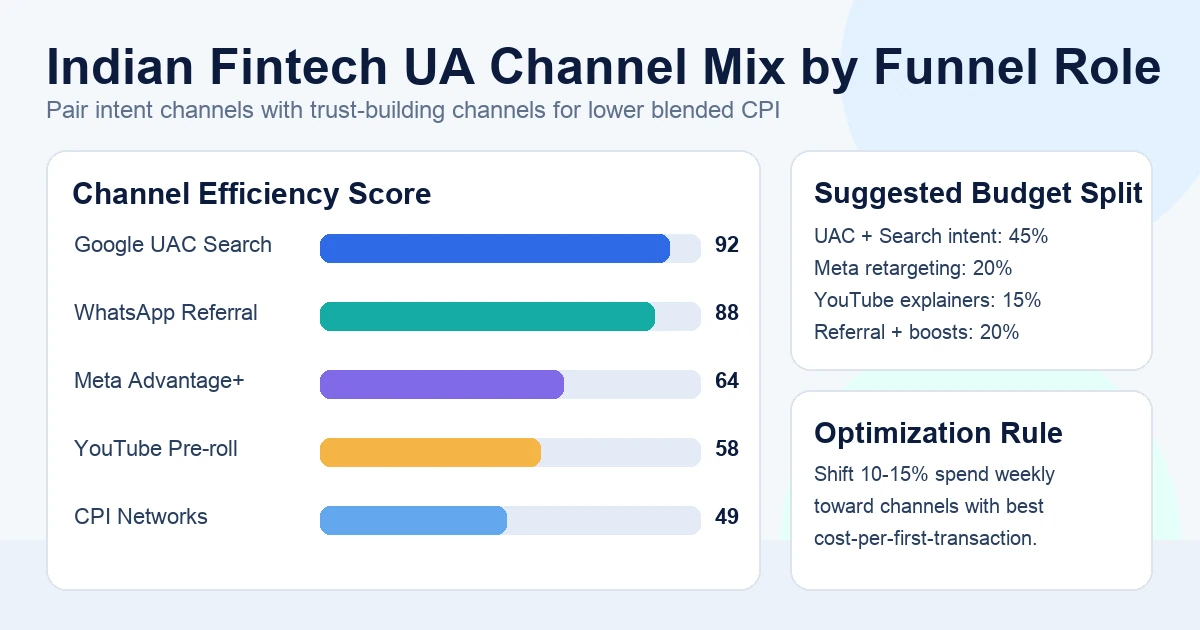

Which User Acquisition Channels Work Best for Indian Fintech Apps?

Indian fintech app user acquisition requires a different channel weighting than consumer apps — trust signals, intent matching, and regulatory compliance across platforms make some channels dramatically more efficient than others.

Based on our portfolio data across 300+ apps including multiple fintech properties, here is how channels rank by performance-to-cost ratio for Indian fintech in 2026:

- Google App Campaigns (UAC): The highest-intent channel for fintech in India. Search inventory captures users actively looking for loan apps, investment apps, and UPI tools — the most valuable moment in the acquisition funnel. UAC campaigns on Search + YouTube deliver consistently the lowest cost-per-first-transaction across our fintech portfolio. Target tCPI initially, then shift to tROAS once you have 50+ post-install conversion events tracked.

- Meta Advantage+ App Campaigns: Effective for broad-reach top-of-funnel awareness and for re-engagement campaigns. Less effective for bottom-of-funnel fintech conversion than Google, because Meta audiences are in consumption mode rather than intent mode. Best used for retargeting lookalikes of high-LTV users from your MMP cohorts. CPIs run ₹80–₹200 for lending, ₹100–₹300 for wealth on Meta for India.

- CPI Network Burst Campaigns: Useful for ranking velocity pushes around product launches or feature releases, but must use Tier-1 networks with fraud filtering. Fintech is a high-fraud category; always integrate with your MMP's fraud-protection layer and set post-install KYC completion as your validation event — not raw install count.

- WhatsApp referral programmes: Significantly underutilised by most fintech teams. In our portfolio, WhatsApp referral share converts 3× better than social share for fintech apps in India. The reason is straightforward: WhatsApp is a trust channel in India. A referral from a known contact about a financial app carries an implicit endorsement that a Facebook ad cannot replicate. Building a structured WhatsApp referral mechanic — with a clear incentive and a frictionless share flow — is one of the highest-ROI growth investments for fintech apps in this market.

- YouTube pre-roll (managed buys): Effective for insurance and wealth apps where the product complexity requires 30–60 seconds of explanation. Skippable TrueView ads from verified financial channels can reach highly relevant audiences at CPMs below ₹20 in Tier 2/3 geographies.

For broking and investment apps specifically, see our detailed stock broker app growth case study which covers the full channel stack for a mid-size broking platform scaling from 50K to 500K users. Insurance app channels are covered in depth in our insurance app marketing guide.

How Do Vernacular Keywords Unlock a Low-Competition Ranking Advantage for Fintech Apps?

The single most underexploited ASO opportunity in Indian fintech is Hindi and regional-language keyword optimisation — most growth teams skip it entirely, leaving a near-zero-competition ranking surface wide open.

Consider the competitive landscape: English-language fintech keywords like "instant personal loan" or "best investment app" have keyword difficulty scores above 70 on most ASO platforms, with dozens of well-funded apps competing aggressively. Now compare that to Hindi equivalents:

- "पैसे उधार लो" (borrow money) — near-zero ASO competition, despite representing the search intent of hundreds of millions of Hindi-speaking smartphone users in Tier 2/3 India.

- "शेयर बाजार" (share market) — similarly low competition on the App Store and Google Play, despite being how the majority of first-time investors in North and Central India describe stock market apps.

- "म्यूचुअल फंड ऐप" (mutual fund app) — Hindi speakers performing this search are high-intent users in the consideration stage, and the ranking competition is a fraction of the English equivalent.

- "लोन ऐप" (loan app) — extremely high search volume from Tier 2/3 users, very low competition, and directly reflects lending intent.

The mechanics of vernacular ASO for Indian fintech:

- Add Hindi keywords to your App Store subtitle (iOS) and short description (Android). Both stores index Devanagari script and serve it to users whose device language is set to Hindi. A simple subtitle update can move you from unranked to top-10 for a Hindi keyword within 2–3 weeks.

- Create a Hindi-language long description section. Google Play's long description is a keyword-rich text field that is fully indexed. A 500-word Hindi section describing your app's features can cover dozens of high-intent vernacular queries simultaneously.

- Use Tamil, Telugu, Kannada, and Marathi equivalents for regional market penetration. A lending app that ranks for "பணம் கடன்" (money loan in Tamil) in Tamil Nadu has a virtually uncontested path to top-3 in that geographic segment.

- Screenshot localisation: Screenshots with Hindi or regional-language benefit statements convert significantly better for non-English speakers, who represent the majority of new fintech app users entering the market from Tier 2/3 cities.

AppsFlyer's State of App Marketing in India report consistently highlights that the growth in mobile app adoption is concentrated in non-metro, non-English-primary users. Vernacular ASO is the mechanism by which fintech apps reach this majority.

What CPI Benchmarks Should You Expect Across UPI, Lending, and Wealth Apps?

CPI benchmarks in Indian fintech vary by a factor of 5–10× across sub-verticals, and planning your budget against the wrong benchmark is one of the most common and costly mistakes we see from teams entering this market.

The benchmarks below are drawn from our first-party portfolio data across multiple fintech campaigns running in India in 2025–2026, cross-referenced against published industry data from Sensor Tower's India Mobile Market Report.

CPI benchmarks by fintech sub-vertical (India, 2026):

- UPI / Payments apps: ₹30–₹80 per install. The lowest CPI in the fintech category because UPI awareness is near-universal and the value proposition is immediate and tangible. Competition is intense from PhonePe, Google Pay, and Paytm, which limits organic share for new entrants — but paid CPIs remain relatively accessible because of high search volume.

- Lending apps: ₹80–₹200 per install. Higher CPI reflects the trust barrier — users are significantly more cautious about installing an app that will access their financial data for credit assessment. Tier 2/3 city campaigns (Jaipur, Bhopal, Coimbatore) consistently deliver the lower end of this range with higher LTV because credit-underserved populations in these cities have fewer alternatives and higher loan activation rates.

- Insurance apps: ₹60–₹150 per install. Insurance app CPI sits between payments and lending. The category benefits from high public awareness of need (health, term, motor insurance) but suffers from high consideration times — users research extensively before installing. Creatives that remove friction and simplify comparison convert better than feature-rich demos.

- Wealth / Broking apps: ₹100–₹300 per install. The highest CPI in Indian fintech, reflecting the sophisticated user profile (higher income, more considered decision), the complexity of the value proposition, and intense competition among established players. Cost-per-first-investment or cost-per-KYC-completion is a better optimisation target than raw install CPI for wealth apps.

A note on Tier 2/3 geography: across our portfolio, Jaipur, Bhopal, and Coimbatore consistently appear in the top-10 cities by LTV-per-install for lending and insurance apps. CPI in these cities runs 20–35% lower than Mumbai or Bengaluru, while first-loan activation and insurance policy purchase rates are comparable or higher. Separating metro and non-metro campaigns in your UAC and Meta structure is not optional if you are managing a fintech budget above ₹5L per month.

For a comprehensive view of CPI benchmarks across all app categories in India, see our India app install cost guide. For crypto and blockchain app benchmarks specifically, our crypto app marketing case study covers that segment in detail.

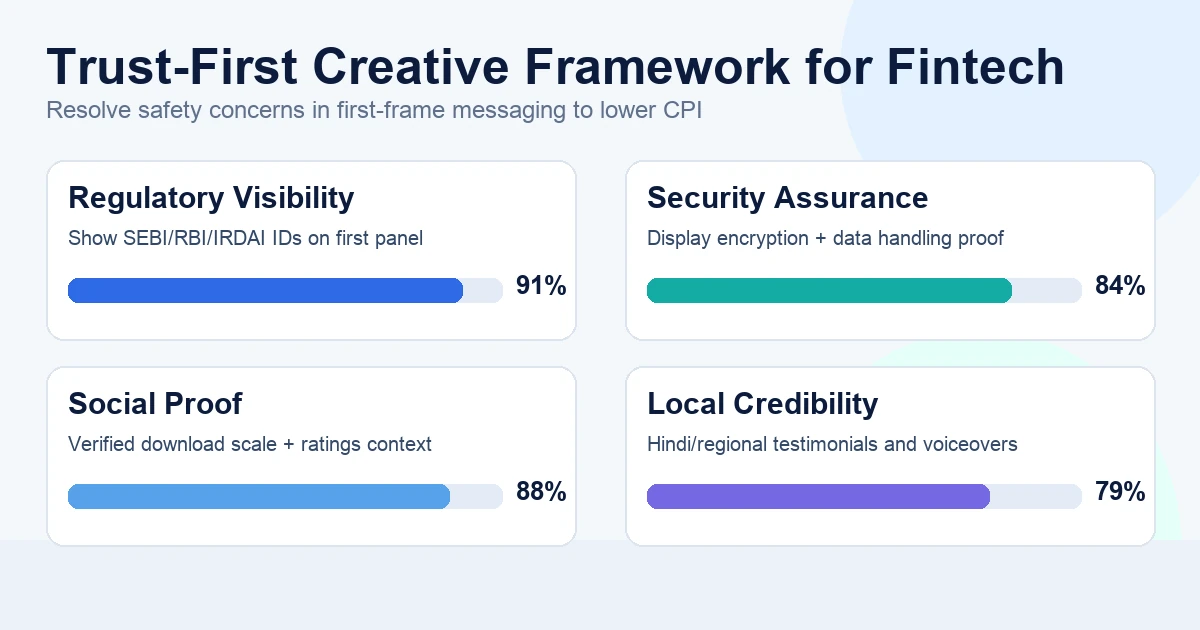

How Do You Build Trust-First Creatives That Reduce Fintech CPI?

Trust is the primary purchase barrier in fintech — not price, not features, not awareness — and creatives that resolve the trust question first consistently outperform feature-demonstration creatives by 2–4× on conversion-to-install in our portfolio.

The trust deficit in fintech is structural. Users are being asked to hand over their bank account details, PAN card, Aadhaar, and sometimes biometric data to an app they discovered in an ad. The mental model they apply is not "does this app have better features?" — it is "is this app safe to trust with my money and my data?" Every creative element should answer that question before it does anything else.

Trust signals that produce measurable CPI reductions in Indian fintech:

- SEBI / RBI / IRDAI regulatory logos in screenshot frames: Displaying the relevant regulator's logo — with the registration number visible — in your App Store screenshots directly addresses the "is this regulated?" question that high-intent users ask. We have observed CPI reductions of 15–25% from screenshot sets that include regulator logos versus those that do not, across multiple lending and wealth app campaigns in our portfolio.

- SSL and data security badges: "256-bit encryption," "ISO 27001 certified," and "bank-grade security" badge overlays in screenshots and video creatives reduce security anxiety for users unfamiliar with the app brand. The effect is strongest for lending apps asking for income and employment data.

- Download counts and social proof: "1 crore+ downloads" or "Trusted by 50 lakh Indians" prominently displayed in the first screenshot frame acts as a powerful herd-signal. Users are more willing to trust an app that demonstrably millions of others have trusted. The number only works if it is real and verifiable — inflated claims are immediately suspect to sophisticated users.

- User testimonial UGC creatives: Video testimonials from real users explaining how a loan cleared a medical emergency or how an investment grew consistently outperform polished product demonstrations. The production quality bar is lower; the authenticity bar is high. A genuine testimonial in Hindi from a Tier 2 city user converts better with that audience than a Mumbai-shot studio ad.

- News media mention overlays: "As seen in Economic Times / Moneycontrol / NDTV" overlays in the first 2 seconds of video creatives borrow credibility from recognisable media brands. This is particularly effective for new entrants without established brand recall.

WhatsApp referral mechanics are a trust-amplification channel rather than a pure performance channel. When a user receives a fintech app referral via WhatsApp from a known contact, the trust transfer is implicit and powerful. Across our fintech portfolio, WhatsApp referrals convert to first-transaction at 3× the rate of social media referral links — the channel is categorically different because the endorsement comes from a person the recipient already trusts with their phone number.

See our user acquisition services page for how we build trust-first creative frameworks as part of managed fintech campaigns.

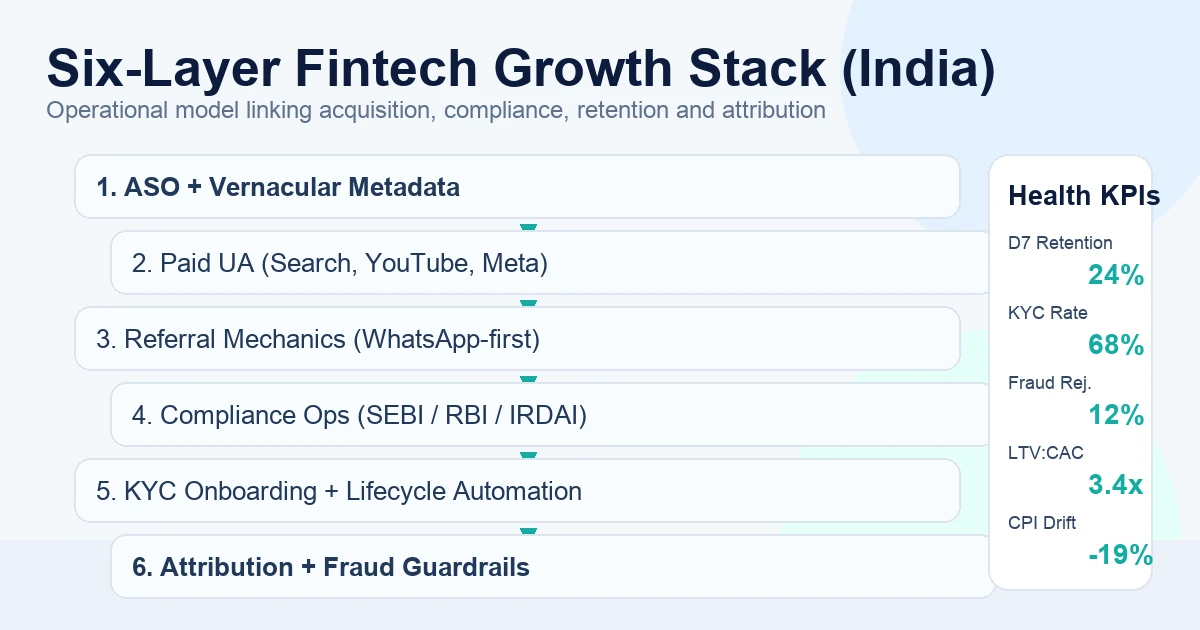

What Does a Full-Funnel Fintech App Growth Stack Look Like in India?

A production-ready fintech app growth stack in India integrates six layers: ASO, paid acquisition, referral mechanics, retention, lifecycle, and compliance infrastructure — and each layer must be configured for the specific regulatory and cultural context of the Indian fintech market.

Here is the full-funnel architecture we use across our fintech portfolio:

Layer 1 — ASO (Top of Funnel, Organic Discovery):

- English + Hindi + 2 regional-language keyword optimisation in metadata

- Screenshot set A/B tested for trust signals (regulator logos, download counts, security badges)

- App icon updated every 6 months minimum; ratings management with developer responses to all 1–2 star reviews within 48 hours

- Google Play Store Listing Experiments running continuously for CVR optimisation

Layer 2 — Paid Acquisition (Mid Funnel, Intent Capture):

- Google UAC on Search + YouTube for high-intent keyword intercept

- Meta Advantage+ for lookalike retargeting against KYC-completed user cohorts

- Geographic campaign splits: Metro India (Mumbai, Delhi, Bengaluru, Hyderabad) versus Tier 2/3 (Jaipur, Bhopal, Coimbatore, Lucknow, Nagpur)

- Creative refresh cadence: new variants every 10–14 days minimum; pause anything below CPI ceiling within 72 hours of launch

Layer 3 — Referral and Trust Amplification:

- WhatsApp share mechanic built into post-transaction flow (deeplink + incentive structure)

- Referral reward calibrated to first-transaction completion, not install — avoids rewarding non-activated referrals

- In-app NPS at D7 and D30 to surface promoter cohorts for referral programme targeting

Layer 4 — Compliance Infrastructure:

- Creative compliance checklist gating all ad assets before platform submission (SEBI/RBI/IRDAI rules per sub-vertical)

- Legal review sign-off for any creative making specific return, rate, or coverage claims

- MMP event taxonomy aligned to regulatory definitions (loan disbursement, KYC completion, first investment) to avoid misrepresentation in performance reports

Layer 5 — Retention and Lifecycle:

- Push notification cadence calibrated to transaction-moment triggers (salary credit, EMI due dates, market hours for broking apps)

- In-app onboarding optimised for KYC completion rate — the single most important post-install event for fintech app health metrics

- D1 / D7 / D30 cohort analysis fed back to paid acquisition bidding strategy via MMP ROAS targeting

Layer 6 — Analytics and Attribution:

- Full MMP integration (AppsFlyer, Adjust, or Singular) with fraud protection enabled — fintech is one of the highest-fraud-risk app categories

- Custom event taxonomy covering every monetisation event: KYC completion, first loan application, first EMI payment, first investment, first renewal

- Incrementality measurement for major channel decisions: never attribute 100% of organic growth to paid without holdout testing

The full stack detailed above is what separates fintech apps that achieve sustainable, repeatable growth from apps that have strong launch months followed by CPI inflation and deteriorating LTV. India's fintech market rewards systematic operators — the regulatory complexity and trust barriers that make entry hard also protect margins for teams that build compliance and trust into their growth infrastructure.

For app-specific playbooks, see our stock broker app growth case study and our insurance app marketing guide. If you are ready to build this stack for your fintech app, talk to our team — we have run campaigns across UPI, lending, wealth, and insurance sub-verticals and can benchmark your current performance against our portfolio.

Frequently Asked Questions

What is the average CPI for a lending app in India in 2026?+

Lending app CPIs in India range from ₹80–₹200 depending on geography, channel mix, and creative quality. Tier 2/3 city campaigns (Jaipur, Bhopal, Coimbatore) consistently deliver the lower end of this range with comparable or higher LTV versus metro campaigns, because credit-underserved users in these cities have higher loan activation rates.

Do fintech app ads in India need SEBI or RBI registration numbers?+

Yes. SEBI-registered investment and broking apps must display their SEBI registration number in all advertising materials. RBI-licensed lending apps must disclose their NBFC licence number or their lending partner's NBFC details. Omitting these disclosures results in ad rejection by Google and Meta's fintech policy reviewers and can attract regulatory action.

Why does WhatsApp referral outperform social share for fintech apps in India?+

WhatsApp is a trust channel in India — referrals arrive from a known contact whose number is already saved. This implicit endorsement from a trusted person resolves the primary trust barrier in fintech (is this app safe with my financial data?) in a way that an anonymous social media referral link cannot. Across our fintech portfolio, WhatsApp referrals convert to first transaction at 3× the rate of social share links.

How do vernacular keywords improve ASO for fintech apps in India?+

Hindi and regional-language fintech keywords like "पैसे उधार लो" (borrow money) and "शेयर बाजार" (share market) have near-zero ASO competition on both App Store and Google Play, despite representing the search intent of hundreds of millions of non-English-primary smartphone users. Adding these keywords to your app subtitle (iOS) or short description (Android) can move you from unranked to top-10 for high-intent vernacular queries within 2–3 weeks.

Which fintech sub-vertical has the highest CPI in India?+

Wealth and broking apps have the highest CPI range in Indian fintech, at ₹100–₹300 per install. This reflects the sophisticated target user profile (higher income, more considered decision-making), the complexity of the value proposition, and intense competition from established broking platforms. Cost-per-KYC-completion or cost-per-first-investment are better optimisation targets than raw CPI for this sub-vertical.

How do I reduce CPI for a fintech app in India?+

The three most effective CPI reduction levers for Indian fintech are: (1) trust-first creatives that display SEBI/RBI logos, SSL badges, and user download counts prominently in the first screenshot frame; (2) vernacular keyword ASO in Hindi and regional languages to capture low-competition organic search traffic; and (3) geographic campaign splits separating Tier 2/3 cities — where CPIs run 20–35% lower than metros while LTV is comparable or higher for lending and insurance apps.

Sources

- NPCI — UPI Product Statistics — Official NPCI data: 18.7 billion UPI transactions in March 2026

- SEBI — Investor Education and Protection — SEBI framework governing advertising disclosures for investment and broking apps

- RBI — Master Circular on Fair Lending Practices — RBI guidelines on interest rate disclosure, NBFC licence requirements, and digital lending compliance

- IRDAI — Insurance Regulatory and Development Authority — IRDAI advertising guidelines: policy exclusion disclosures and regulatory approval requirements for insurance apps

- AppsFlyer — State of App Marketing in India — First-party data on Indian app marketing performance, vernacular user growth, and channel benchmarks

- Sensor Tower — India Mobile Market Report — CPI benchmarks and fintech app category performance data for India

- Vmobify — India App Install Trends 2026 — First-party analysis of install cost trends across fintech and adjacent categories in India

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy