Buy App Installs Safely: What's Legit, What Gets You Banned

"Buy app installs" returns a thousand sketchy vendors. Most will get your app suspended. Here are the channels that genuinely work, the red flags to spot, and how to evaluate a vendor in 10 minutes.

Why do apps buy installs in the first place?

Every top-ranked app in every category buys installs — they just call it performance marketing, paid UA, or demand-side bidding instead of "buying installs." The phrase has a sketchy reputation because the sketchy end of the market shouts the loudest in Google search results, but the underlying activity is the foundation of the entire mobile ad ecosystem.

The legitimate reasons apps pay for installs:

- Velocity for ranking: Burst installs to climb category ranks and unlock organic discovery surfaces. Both Google Play's launch guidance and Apple's editorial systems weight velocity heavily.

- Scale beyond organic ceiling: Your organic install rate caps at some level dictated by category demand and ASO. Paid is the only way past it.

- Geographic expansion: Entering markets where you have zero organic presence. India Tier-2/3, SEA, and LATAM almost always require paid seeding before organic kicks in.

- Audience testing: Proving demand in a segment before committing engineering or product investment.

- Competitive defence: Holding category position when a well-funded rival launches a UA push.

The bad reasons — faking traction for fundraising, inflating numbers for vanity, "let me see what happens" experiments without retention infrastructure — all end the same way. Either the platform catches you, or your investors do after the cohort retention curves come in.

Across our 300+ apps managed since 2013, the founders who succeed with paid UA share one trait: they treat install purchases as a CAC-to-LTV maths problem, not as a vanity-number exercise. Everything below assumes you are in the first camp.

There is also a structural reason buying installs is unavoidable past a certain stage: the install funnel is not symmetric. A new app with zero downloads has zero ranking, zero reviews, and zero algorithmic discovery surface — which means zero organic installs, which means zero ranking, in an indefinite loop. Paid acquisition is how you break the loop. Even apps that eventually generate 90% of installs organically went through a 6-12 month phase where paid carried 60-80% of volume to establish the ranking foundation organic could build on.

What separates legitimate paid installs from banned ones?

The single rule that separates safe from suspended: are the installs from real humans who actually want to use your app? Everything else is implementation detail.

Safe is real users seeing an ad on a real publisher app or surface, choosing to install, and using the app. Apple's App Store Review Guidelines and the Google Play Developer Policy both explicitly permit paid user acquisition — it is the foundation of the entire mobile ad ecosystem and the revenue source for most publisher apps you have on your phone right now.

Banned is anything where the install is generated without genuine user intent: bot traffic, device farms, install hijacking, undisclosed incentivised offers, click flooding to claim attribution for organic installs, or coordinated review/install schemes.

The grey zone — incentivised non-disclosed installs — is what trips up most apps. Disclosed incentivised traffic (offerwalls clearly labelled "install this app, get 50 coins in your current game") is allowed on both platforms. Disguising incentivised traffic as organic is not. AppsFlyer's State of App Marketing reports consistently show that incent-disguised-as-organic is the single largest fraud category by volume — and the one MMPs are best at detecting.

Apple's SKAdNetwork and Google's Play Install Referrer give both platforms first-party visibility into install patterns. If your installs cluster on emulator fingerprints, run from datacentre IPs, or show install velocity inconsistent with the publisher app driving the click, the signal goes back to the platform. Suspension follows.

One nuance worth flagging: enforcement is asymmetric. Apple is faster and more aggressive on consumer-facing violations (review schemes, misleading subtitles, incent-disguised-as-organic). Google is faster on policy violations around data handling, permissions, and SDK behaviour. Both platforms now share intelligence with the major MMPs through SDK signals, so the half-life of "this fraud method still works" has dropped from years to weeks in 2026.

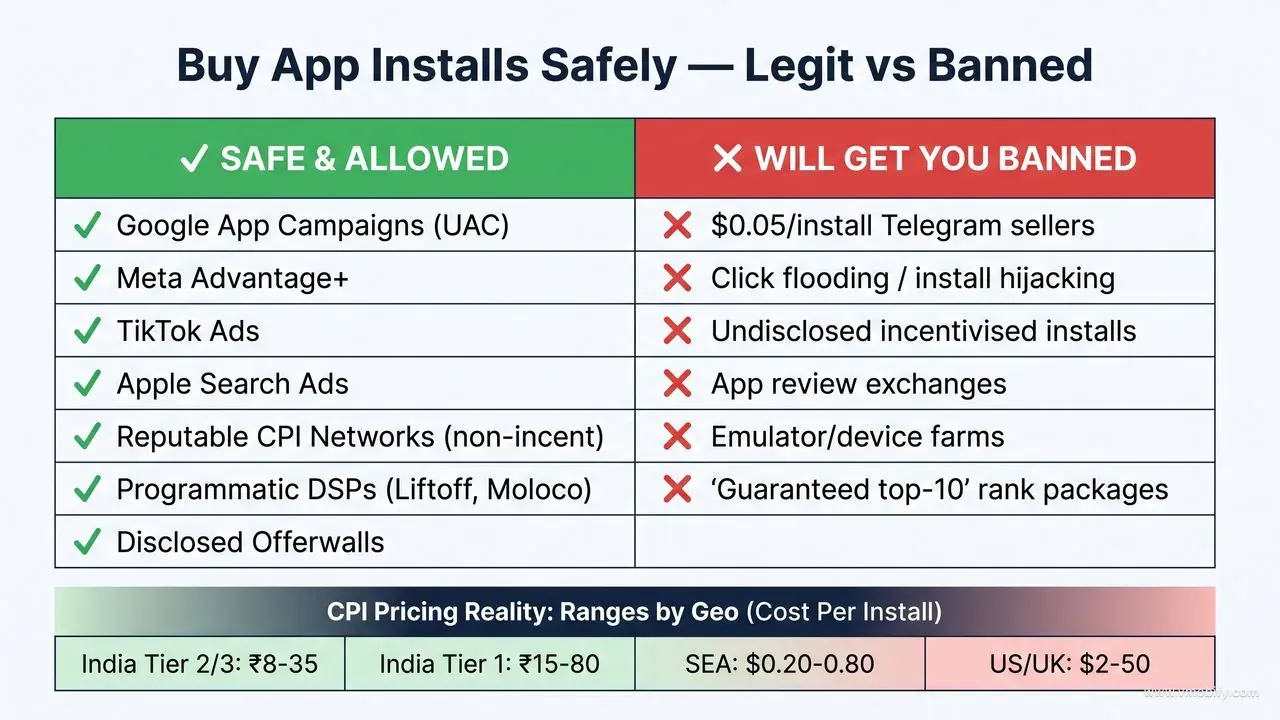

Which channels are genuinely safe to buy installs from?

The safe channel set is short, well-documented, and used by every serious app at scale. If a channel is not on this list, treat it as guilty until proven innocent.

- Google App Campaigns (UAC): The largest paid install channel on the planet. Ads run across Search, YouTube, Play, Discover, and Google's display network. Google's own UAC documentation covers setup. Zero platform risk.

- Meta Advantage+ App Campaigns: Same model on Facebook, Instagram, Messenger, and Audience Network. Meta's official guidance covers structure. Excellent for broad-demographic apps.

- TikTok Ads Manager: In-feed video and Spark Ads driving installs. The strongest paid channel for sub-25 audiences in 2026.

- Apple Search Ads: Pay for placement in App Store search results via the Apple Search Ads platform. The single most intent-rich install source on iOS — users searching the App Store have demonstrated intent before they ever see your ad.

- Reputable non-incent CPI networks: Tapjoy, Aarki, Liftoff, ironSource non-incent inventory, and our own vetted publisher set. Real users on real third-party apps clicking real ads. Quality is measurable through any MMP.

- Programmatic DSPs: Moloco, AppLovin, Adikteev, Remerge. Real-time bidding into real publisher inventory. Best for retargeting and lookalike scaling once you have a base of converted users.

- Disclosed offerwalls and rewarded video: Tapjoy, Fyber, ironSource offerwalls where users see a clear "install this app, get 50 coins in your current game" prompt. Allowed because users opt in knowingly — but track these installs separately, as their retention curve is structurally different from organic-look-alike traffic.

Any of these channels can be used at scale without any platform risk. Combined, they cover essentially the entire legitimate paid UA market. For a head-to-head comparison of the three biggest channels for most apps, see our Google UAC vs Meta vs CPI breakdown.

In our portfolio, the channel mix that works for most apps post-product-market-fit is roughly 40% UAC, 30% Meta, 15% Apple Search Ads (iOS-heavy apps), 10% CPI network burst, and 5% experimental DSP/TikTok. Adjust by vertical — gaming apps lean heavier on DSPs and rewarded video; fintech leans heavier on Search Ads where buyer intent is highest.

The reason this list stays short is structural. Real install volume requires real publisher inventory, which is dominated by a handful of supply networks (Google, Meta, TikTok, Apple, AppLovin, Unity, ironSource). Anyone selling "installs" outside that supply chain is either reselling the same inventory at a markup, or they are not selling real installs at all. There is no secret high-quality supply hidden away from the big networks — supply consolidation is one of the defining features of the 2026 ad market.

Which channels will get your app banned?

Some of these channels still operate openly online. They are not safe — they are unenforced for now and high-risk forever. Apple and Google both run continuous fraud-detection sweeps; "unenforced today" is not a business model.

- "$0.05 per install" packages from anonymous Telegram or WhatsApp sellers: Bot or device-farm traffic, detected by every major MMP within hours. The cost saving is illusory because the installs are filtered out before they ever count toward your goals.

- Click flooding and install hijacking services: Vendors that "attribute" your existing organic installs to themselves by spraying clicks at every IP they can buy. You pay; they delivered nothing real. AppsFlyer's fraud benchmarks show click flooding remains one of the most common fraud types in 2026, especially in emerging markets.

- Incentivised installs sold as organic: The vendor knows you are not disclosing the incentive. The platform is what catches you — and the platform does not refund your spend or your account.

- App review exchange groups: Coordinated install-plus-review schemes operating on Telegram, Discord, and obscure forums. Apple's Review Guideline 5.6 explicitly bans participation. Suspension on detection.

- Emulator farms and virtual-device installs: Easy to spot in MMP fraud filters because device fingerprint entropy is low, install velocity per IP is unnatural, and behavioural patterns are uniform across "users."

- Anyone "guaranteeing" top-10 category rank in a competitive vertical for a fixed price: The only ways to guarantee that outcome involve fraud at scale, or an enormous budget — and the enormous-budget path comes from your spend, not theirs. An honest agency will not guarantee outcomes the platform algorithm controls.

- "SDK installs" from publishers that auto-install apps on user devices: A recurring fraud pattern in low-quality Android ad networks. The install registers; the user never opens the app because they never asked for it.

If a vendor pitch sounds like a too-good-to-be-true bargain, it almost certainly involves one of the above. We have seen apps lose 6-12 months of organic traction after a single bad CPI campaign tipped the platforms' fraud signals. The cleanup is harder than the original UA work.

How do you evaluate a vendor in 10 minutes?

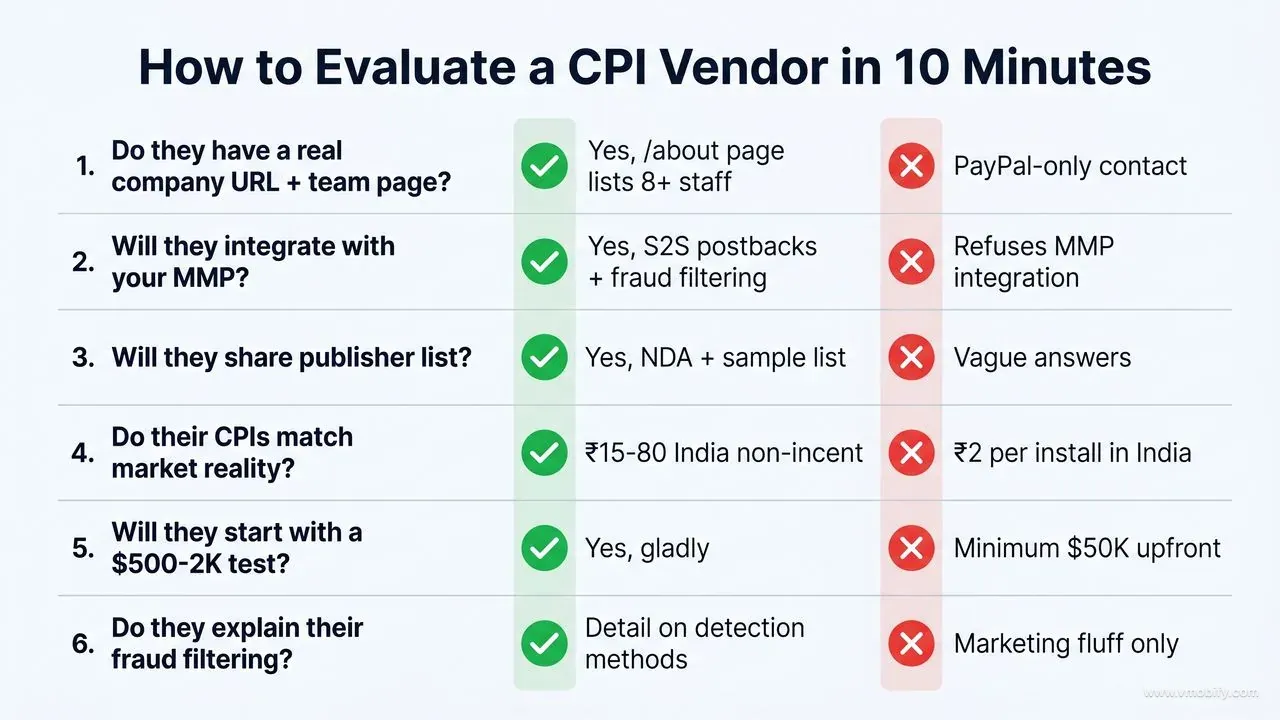

Before you pay anyone for installs, run this six-question checklist. A legitimate vendor passes all six in a single call; resellers and fraud operators fail at least two.

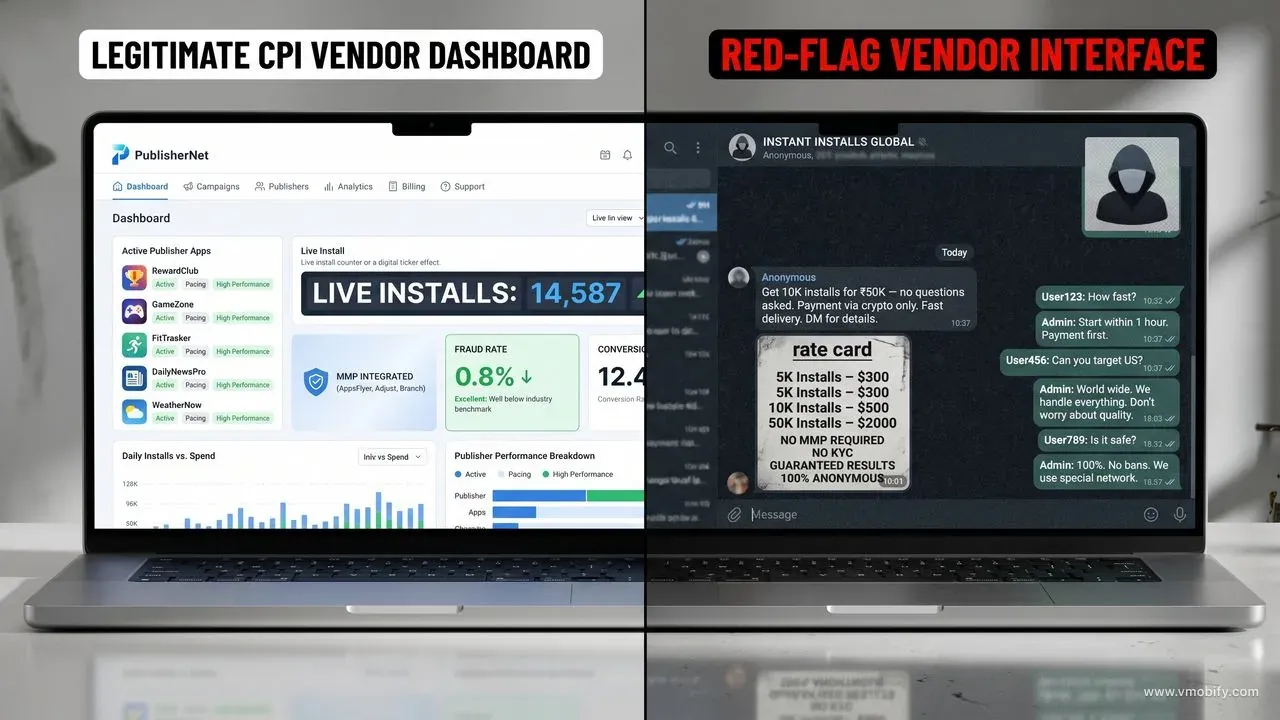

- Do they have a real company URL, team page, and verifiable office? Anonymous PayPal-only or USDT-only vendors are red flags by themselves. Real CPI networks have LinkedIn-traceable founders and named operations leads.

- Will they integrate with your MMP (AppsFlyer, Adjust, Singular, or Branch)? If they refuse or claim "our own tracking system is better," they cannot prove install quality on a neutral measurement layer. Walk away. MMP integration is the single most diagnostic question.

- Can they share a sample publisher list? Real CPI networks know exactly which apps their traffic is from and can name at least a top 10 by volume. Vague answers ("we have thousands of publishers") mean opaque sourcing — which is how fraud enters the supply chain.

- Do their CPIs match market reality? If they offer ₹2 per install in India or $0.10 in the US for non-incentivised traffic, the underlying maths does not allow real installs. The cost of acquiring a real human via a real publisher is bounded by publisher CPMs and click-through rates — there is no magic discount.

- Will they start with a small test ($500-$2,000)? Legitimate vendors welcome a small pilot because they expect to win on retention quality. Vendors demanding $10K minimums upfront are usually running on advance payments because they cannot retain clients past the first campaign.

- Do they explain their fraud filtering in specifics? Real networks talk freely about IP reputation, device fingerprint entropy, install-to-event timing distributions, and SDK-level signal validation. If you get marketing fluff instead of specifics, the fraud filter does not exist.

A bonus seventh question for the genuinely cautious: ask whether they will sign a clawback clause that refunds any installs flagged as fraud by your MMP within 30 days. Real networks have clean enough traffic to accept this; fraud operators will not even discuss it.

If you want a managed second opinion before committing budget to a new vendor, our team reviews vendor proposals as part of standard UA strategy engagements.

What does real install pricing look like by geography?

Realistic non-incentivised CPI ranges in 2026, by geography and vertical, based on our portfolio data and cross-referenced with AppsFlyer Performance Index benchmarks:

- India Tier-1 metros (Mumbai, Delhi, Bangalore): ₹15-80 depending on vertical. Utility apps land at ₹15-35; D2C and ecommerce ₹30-70; fintech ₹50-150; gaming ₹20-60.

- India Tier-2/3 cities: ₹8-35. The cheapest meaningful CPI market in the world for genuine installs. Audience size is in the hundreds of millions; competition from Western advertisers is still light.

- SEA (Indonesia, Vietnam, Philippines, Thailand): $0.20-0.80 for utility and gaming; $0.80-2.50 for fintech and ecommerce.

- LATAM (Brazil, Mexico, Colombia, Argentina): $0.40-1.50 for utility; $1.50-4 for fintech and subscription apps.

- US, UK, Canada, Australia: $2-8 for utility and social; $5-20 for gaming; $15-50 for fintech and BFSI verticals. These are the most competitive auctions in the world.

- Western Europe (Germany, France, Netherlands, Nordics): $1.50-7 across most verticals; up to $25-40 for regulated fintech and insurance.

- Tier-1 MENA (UAE, Saudi Arabia): $1-4 for utility and gaming; $3-10 for ecommerce and fintech. High AOV makes the maths work.

If a vendor quotes 30%+ below these ranges for "the same audience," ask hard questions. The economics of acquiring real users on real publishers do not allow 80% discounts — publisher CPMs and conversion rates put a floor under what an honest CPI can be. Anything dramatically below market is one of: incentivised traffic disguised as organic, bot or device-farm traffic, click-flooded attribution stealing your organic, or a vendor losing money on first deals to lock in larger commitments.

The flip side: if a vendor quotes far above these ranges, you are likely paying agency margin on resold supply. Going direct to the network — or working with an agency that discloses its supply chain — typically saves 15-30% on the same publisher inventory.

For category-specific India benchmarks see our India CPI benchmark guide; for context on how these economics compare across the three biggest paid channels, see our UA services overview.

How do you measure install quality after you buy?

Judge bought installs on retention and behaviour — never on the raw install count the vendor invoices you for. A vendor can deliver 10,000 "installs" that all churn by D1 and technically claim contract completion; whether those installs were worth paying for is an entirely separate question.

The five signals we measure on every paid campaign across our portfolio:

- D1 retention vs your organic baseline: Good non-incent traffic lands within 70% of your organic D1. Below 30% is bot traffic or completely mistargeted audience. Disclosed offerwall traffic structurally retains worse — budget for that going in.

- Conversion to a meaningful in-app event: Registration, first purchase, level 5, paywall view. If paid installs convert at less than 25% the rate of your organic installs on the same event, the traffic is low-intent regardless of what the install count says.

- Geographic distribution at sub-region level: If you bought "India" and 80% of installs cluster in three small towns you have never targeted, you are looking at a device farm. Real publisher traffic distributes across the country roughly in proportion to smartphone population, which Statista's India smartphone forecast tracks reliably.

- Install timestamp pattern: Real organic and real paid installs distribute smoothly across the day, with predictable peaks during commute and evening hours. Bot traffic clusters tightly in 1-hour windows because it is generated by scripts running on fixed schedules.

- MMP fraud rate flagged: Anything above 5% post-attribution should trigger a refund discussion. Anything above 15% means the supply was contaminated and you should stop the campaign immediately, not wait for the contract to complete.

A sixth signal worth tracking once you have 30+ days of data: revenue per install relative to organic. Paid users from genuine intent sources typically monetise at 50-90% of organic on a per-install basis. Anything under 20% is either fraud, deeply misaligned audience, or both — and either way the spend should stop while you investigate rather than continue while you "wait for the cohort to mature."

The diagnostic move when something looks off: pull a sample of 50 installs at random from the paid cohort and look at the per-user event sequence in your MMP. Real users have messy, varied sessions — they open, browse, leave, come back, hit one or two events. Fraudulent installs either show zero post-install activity or show a uniform 3-event sequence that completes inside two minutes. The pattern is unmistakable once you have seen it twice.

If you need help evaluating a vendor, structuring a managed CPI program, or auditing existing paid UA spend for fraud and quality, our CPI network team vets every publisher before traffic flows. See case studies for examples of how this playbook performs in production.

Frequently Asked Questions

Is buying app installs against App Store or Google Play policy?+

No — buying installs through legitimate ad networks is explicitly allowed and is the foundation of the entire app advertising ecosystem. What is banned is fraudulent installs (bots, device farms, undisclosed incentivisation, install hijacking).

Can buying installs improve my ranking?+

Yes, if the installs are real users from non-fraudulent sources. Both stores reward install velocity as a ranking signal. Fraudulent installs may briefly lift ranking but trigger penalties when detected, often costing 6-12 months of organic traction.

What is the cheapest country to buy real installs in?+

India Tier-2/3 cities and Indonesia consistently have the lowest non-incentivised CPIs globally — often under ₹15 or $0.30 — while still delivering real users from real publisher apps.

How long after a CPI burst should I expect organic lift?+

Typically within 3-7 days. The lift usually lasts 2-4 weeks as your category ranking holds, then decays unless paid spend continues. Pairing the burst with ASO updates extends the decay window.

How do I know if my MMP is filtering fraud properly?+

Enable all built-in fraud rules in AppsFlyer / Adjust / Singular and review the rejected install report weekly. Reputable networks send well below 3% fraud-flagged installs; bad ones send 20%+ and the supply should be cut immediately.

Are offerwall installs safe or banned?+

Disclosed offerwalls (where users see a clear "install this app for X reward" prompt) are explicitly allowed by both Apple and Google. Disguising offerwall traffic as organic is what triggers bans. Track offerwall cohorts separately so the retention curve does not contaminate your blended UA reporting.

Should I pay a vendor upfront or post-attribution?+

Post-attribution wherever possible, with MMP-validated installs as the billable trigger. Reputable networks accept this model because their traffic survives MMP validation; vendors who insist on upfront payment for "installs delivered" are pricing in attrition that will show up in your fraud flag rates.

Sources

- Apple — App Store Review Guidelines — Official rules on incentivised installs, review schemes, and install manipulation (sections 3.2.2, 5.6)

- Google Play — Developer Policy — Official policy on artificial install inflation and ad fraud

- Google Play — Launch Best Practices — Google's documentation on install velocity as a ranking signal

- Google Ads — App Campaigns Help — UAC setup, bidding, and creative best practices

- Meta — Advantage+ App Campaigns — Official Meta documentation on app install campaign structure

- Apple Search Ads — Official platform documentation for App Store paid placements

- AppsFlyer — Performance Index — Quarterly benchmarks for CPI, retention, and fraud rates by category and geography

- AppsFlyer — State of App Marketing — Annual industry report on fraud categories, spend trends, and channel performance

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy