Stock Trading App Activation: KYC 36% to 59%, First Trade Doubled

A fast-growing Indian discount-broking app was buying installs efficiently but bleeding them in the account-opening funnel — only 36% of the users who started KYC finished it, and just 8% of installs ever placed a trade. Over five months we rebuilt the KYC funnel, the first-trade experience, and the early-retention loop: KYC completion climbed from 36% to 59%, install-to-first-trade doubled from 8% to 17%, D30 retention rose from 12% to 20%, and CAC payback fell from 14 months to 8. Here is the full activation playbook.

What was the brief and the starting position?

A fast-growing Indian discount-broking app came to us with an unusual problem for a venture-backed fintech: its paid acquisition was working, but almost none of the installs it was buying ever turned into funded, trading customers. The acquisition team had spent two years getting cost-per-install down and install volume up. The activation funnel underneath had never been rebuilt to match. The result was a leaky bucket — installs poured in at the top, and a thin trickle of funded accounts came out the bottom.

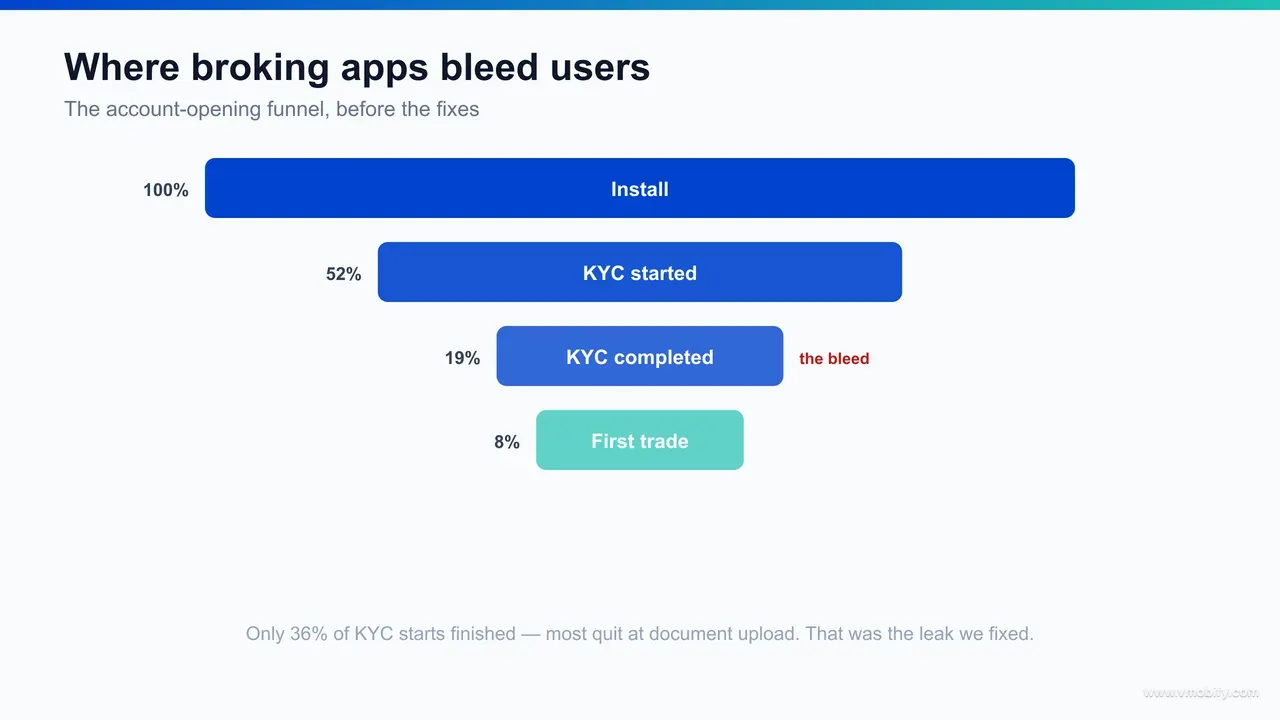

The starting numbers told the whole story. Of every hundred installs, 52 started the KYC / account-opening flow — a respectable top-of-funnel intent rate for the category. But of those who started, only 36% completed KYC. Multiply it through and barely 19 of every 100 installs ever reached a funded, tradeable account. Worse, only 8% of installs ever placed a first trade, and D30 retention sat at 12%. With that little activation, the blended CAC payback period stretched to roughly 14 months — dangerously long for a business that has to fund growth out of trading revenue.

The brief, once we had pulled the data apart with them, was not "get us more installs". It was the opposite. They had installs. They needed those installs to open accounts, fund them, place a trade, and come back. In other words, this was an activation and early-retention engagement, not an acquisition one — a distinction most growth teams miss until the unit economics force the issue.

Across our 300+ apps managed since 2013, we have seen this exact pattern repeatedly in Indian fintech: a competent media team buying efficient installs into a funnel that was never instrumented or rebuilt, so the deepest, most expensive-to-influence drop-offs stay invisible. The money was not being wasted in the auction. It was being wasted between the install and the first trade. This case study documents how we found that waste, fixed it, and reset the economics over a five-month window — taking KYC completion from 36% to 59%, install-to-first-trade from 8% to 17%, D30 retention from 12% to 20%, and CAC payback from 14 months to 8.

Why is the KYC funnel where broking apps bleed users?

The account-opening funnel is where Indian broking apps lose the most users because it is the longest, most regulated, most friction-dense stretch of the entire journey — and it sits before the user has experienced a single moment of product value. A user installs a trading app on a burst of intent; then, before they can do anything, they are asked to complete a regulated identity-verification gauntlet. The gap between intent and reward is where the bleed happens. Five structural reasons make this the hardest funnel in the category:

- KYC is mandatory, multi-step, and document-heavy: Opening a demat and trading account in India is a SEBI-regulated process that requires PAN, Aadhaar-based verification, bank-account linking, a signature, often an in-person or video step, and nominee details. Every required field is another place to abandon. The regulation is non-negotiable, but the sequencing and presentation of it is entirely within the app's control — and that is where most apps leave conversion on the table.

- The value is deferred: Unlike a game or a content app, a broking app delivers no value during onboarding. The user works through a long form for a reward — the ability to trade — that they cannot taste until the very end. Deferred value plus high friction is the textbook recipe for funnel abandonment.

- The document-upload step is a UX minefield: Photographing a PAN card, capturing an Aadhaar OTP, matching a name across mismatched government records — these are the steps where users on mid-range Android devices and patchy connections drop off in droves. A blurry-image rejection with no clear retry path ends the session permanently.

- Trust is fragile and the alternative is one tap away: A first-time investor who hits friction in an unfamiliar broking app does not push through — they abandon and reconsider an incumbent they already trust. The switching cost of quitting mid-KYC is effectively zero.

- The drop-off is invisible without instrumentation: Most broking apps fire an "install" event and a "KYC complete" event and nothing meaningful in between. That means the funnel looks like a black box — you can see that users go in and few come out, but not where they vanish. You cannot fix a drop-off you cannot see.

India's demat-account base has grown at a record pace, and AppsFlyer's India benchmarks consistently show finance onboarding funnels converting well below gaming or shopping. That is the opportunity and the trap at once: enormous top-of-funnel demand, funnelled through an account-opening flow that quietly discards most of it. Knowing all five constraints shaped the plan — make every step of the funnel visible, then attack the friction step by step, starting with the document-upload screen where the bleed was worst.

How did we instrument the account-opening funnel?

Before changing a single screen, we instrumented the full account-opening funnel as a granular event sequence — so that every drop-off between install and first trade became a number on a chart instead of a guess. You cannot optimise what you cannot see, and the app's existing analytics treated KYC as one opaque step. The first month of the engagement was almost entirely measurement work, and it was the highest-yielding month of the project.

What we built, in order:

- A step-by-step event taxonomy: We replaced the two-event "install → KYC complete" model with a properly instrumented sequence — install, KYC-start, PAN-entered, PAN-verified, Aadhaar-OTP-requested, Aadhaar-verified, document-uploaded, document-accepted, bank-linked, nominee-added, signature-captured, KYC-complete, account-funded, first-trade-placed. Suddenly the black box had fourteen windows in it. Our mobile analytics team owns this layer because a mis-fired or missing event hides exactly the drop-off you most need to fix.

- Funnel visualisation by step and segment: With the events flowing, we built funnel views — broken down by device tier, OS, acquisition channel, and city tier — using a product-analytics stack. Amplitude's product-analytics approach to step-conversion analysis is the model: see the absolute drop at every step, then segment to find who drops worst.

- The drop-off heat map: The instrumentation immediately exposed the truth. The single largest cliff was at the document-upload step — PAN photo and Aadhaar verification — where a disproportionate share of the KYC-start-to-complete loss occurred. A secondary cliff sat at bank-account linking. The "36% completion" number was not a smooth, evenly-distributed leak; it was two or three specific screens doing most of the damage.

- Session replay on the worst steps: For the two worst screens we layered in session replay and rage-tap detection. Watching real users fail to photograph a PAN card, get a vague rejection, and quit told us more in an afternoon than a month of aggregate funnel data could.

The reframe this produced was the turning point of the whole engagement. The client had been treating a 36% KYC-completion rate as a single, monolithic conversion problem to be solved with incentives or more retargeting. The instrumentation showed it was really a handful of specific, fixable UX failures concentrated on two or three screens. That is a completely different — and far more tractable — problem. We have seen this every time we instrument a fintech funnel properly: the headline number is an average that hides a small number of catastrophic steps. Fix those steps and the average moves hard.

How did we fix the document-upload drop-off?

The document-upload and identity-verification step was the single biggest leak in the funnel, so it got fixed first — and rebuilding it recovered more KYC completion than any other change in the project. This is the screen where a user has to photograph a PAN card, complete Aadhaar verification, and have their name matched across government records, often on a mid-range phone with an unreliable connection. The original flow handled all of that badly. Here is what we changed and why each change mattered:

- Real-time capture guidance, not post-hoc rejection: The original flow let users take any photo, uploaded it, and then rejected it seconds later with a generic "document not clear" error and no obvious retry. We replaced that with live, on-camera guidance — edge detection, a framing guide, glare and blur warnings before capture — so the photo is right the first time. The number-one cause of document-step abandonment is a rejection the user does not know how to fix; eliminating the rejection eliminates the abandonment.

- Specific, actionable error states: Where verification did fail, we rewrote every error from vague ("verification failed") to specific and instructive ("the name on your PAN does not match your Aadhaar — tap here to enter it as it appears on your PAN"). A user who knows exactly what to do next retries; a user staring at "failed" closes the app.

- Aadhaar OTP resilience: The Aadhaar-OTP step failed silently when an OTP was delayed or the network dropped. We added explicit retry, resend, and timeout states, plus a fallback path, so a slow OTP no longer dead-ended the session. India's identity rails are robust but latency varies; the RBI's KYC master direction mandates the verification, but nothing mandates handling it fragile-first.

- Progressive autofill and name-matching: Where a PAN-verified name and an Aadhaar name diverged — extremely common in India — we surfaced the mismatch early and let the user resolve it in one tap instead of failing at the end of the flow. Catching the mismatch at entry rather than at submission saved an entire abandoned application per occurrence.

- Device-tier-specific handling: Session replay had shown the drop-off was concentrated on lower-end Android devices. We compressed image handling, reduced the upload payload, and added optimistic UI so the step felt responsive even on slow connections, which is where the most price-sensitive — and most valuable to convert — Tier-2/3 users live.

The document step alone accounted for the largest single block of recovered completion. It is the clearest illustration of why instrumentation came first: had we started by adding first-deposit incentives or retargeting, as the client originally proposed, we would have been pouring more users into a funnel that broke at exactly the same screen. Fix the leak before you increase the inflow. This is the core principle behind our work on app onboarding best practices — the highest-converting onboarding is the one with the fewest places to fail.

How did onboarding compression and deferral lift KYC completion?

Beyond fixing the broken screens, we shortened the funnel itself — compressing the number of steps a user had to clear before their account was usable, and deferring every step that did not legally have to happen up front. The original flow front-loaded everything: it demanded nominee details, full bank verification, segment activation (equity, F&O, commodity), and communication preferences all before the account was opened. Most of that is not required to reach a funded, tradeable state. Moving it out of the critical path was the second-largest lever after the document fix.

The principle is simple: get the user to value with the minimum mandatory friction, then collect everything else once they are already invested. What that meant in practice:

- Deferring non-essential steps past the activation moment: Nominee details, additional-segment activation, and communication preferences were pulled out of the opening flow and moved to post-funding prompts. A user can now reach a funded account having completed only what regulation strictly requires, and is asked for the rest contextually, later, when the friction cost is far lower because they are already committed.

- Collapsing the step count: We merged screens that did not need to be separate, removed redundant confirmation interstitials, and cut the visible step count of the core flow by roughly a third. Every screen removed is a place a user can no longer abandon. Adjust's onboarding research is consistent on this — completion rate falls measurably with each additional mandatory step, so the shortest compliant path wins.

- A persistent progress bar and step counter: The original flow gave no sense of how much was left, so users abandoned because the process felt open-ended. We added a clear "step 3 of 6" progress indicator. Knowing the finish line is near is one of the cheapest, most reliable completion levers in onboarding — the effort feels bounded.

- Contextual nudges and save-and-resume: If a user paused mid-flow, their progress was saved and a contextual nudge could bring them back to the exact step they left. No more starting over from screen one — the single most demoralising thing a half-finished applicant can encounter.

- Just-in-time explanations: At each potentially confusing step ("why do you need my bank details?"), we added a one-line, plain-language reason inline. Trust friction in regulated finance is reduced by explaining the why at the moment of the ask, not burying it in a help centre.

Compression plus deferral plus the progress bar moved completion materially on their own, on top of the document-upload fix. The combined effect of the funnel-rebuild workstream — fixing the broken steps and removing the unnecessary ones — is what carried KYC completion from 36% toward the high-50s. Critically, none of it touched the regulatory requirements; every legally mandated check still happens. We simply stopped asking for things early that could be asked for late, and stopped letting fixable UX failures end applications. Our user acquisition and growth team treats funnel architecture as inseparable from media buying for exactly this reason — efficient installs into a broken funnel is just efficient waste.

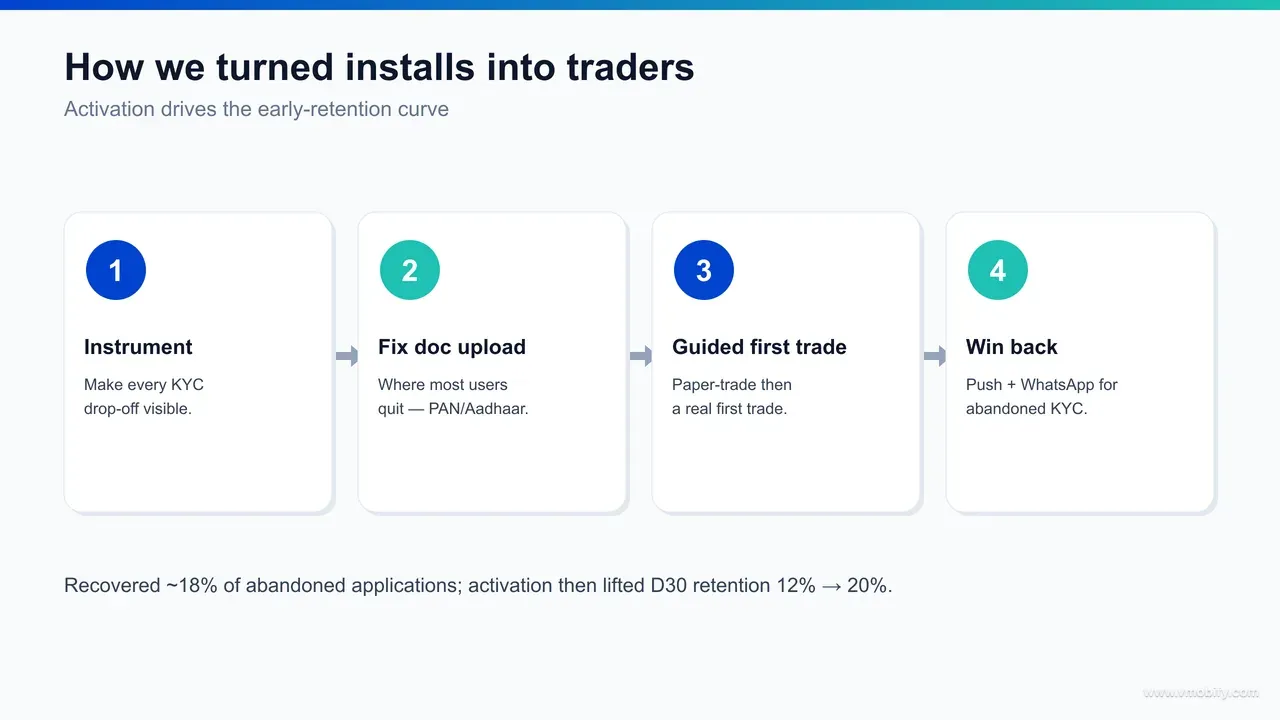

How did the guided first-trade experience drive activation?

Getting a user to a funded account is only half of activation — the other half is getting them to place a first trade, and we did that by replacing an intimidating empty dashboard with a guided paper-trade-to-real-trade experience. A newly funded user who lands on a blank trading terminal full of unfamiliar order types, charts, and jargon freezes. They have crossed the hardest part of the funnel and then stall at the finish line. The first-trade experience was rebuilt to carry them across it. This is where install-to-first-trade doubled, from 8% to 17%.

The guided experience worked on four mechanics:

- A risk-free paper trade first: Instead of dropping the user into a live order with real money, we offered a guided practice trade — pick a familiar large-cap stock, place a simulated buy, watch it confirm. It teaches the exact mechanics of placing an order with zero financial risk and zero fear. Removing the fear of the first real order is the entire job, and a dry run does it better than any tooltip.

- A curated, confidence-building first watchlist: A blank watchlist is paralysing. We pre-populated a starter watchlist of well-known, liquid stocks so the new user had something familiar to look at and act on, rather than a search box and a blinking cursor. Choice overload at the activation moment kills activation.

- A scaffolded path from paper to real: Immediately after the successful paper trade, the user was prompted to place their first real trade — same flow, now with real money, while the muscle memory was fresh. The transition was deliberately frictionless by design: the real-trade screen mirrored the paper-trade screen they had just succeeded at, so it felt familiar instead of new.

- Contextual education at the point of action: Order types, market-versus-limit, and basic risk concepts were explained inline at the exact moment the user encountered them, not in a separate tutorial they would skip. Education delivered at the point of need converts; education delivered up front gets dismissed.

The strategic insight here is that activation is a sequence of confidence thresholds, not a single conversion event. Funding the account is one threshold; placing the first order is the next; and the gap between them is mostly fear and unfamiliarity, not intent. A user who has funded an account clearly wants to trade — they just need to be shown it is safe and simple. The guided first-trade flow is the bridge across that fear, and doubling install-to-first-trade is what it bought. In our portfolio, the broking and investing apps that retain best are invariably the ones that get the user to a successful first trade fastest — the first trade is the true activation event, not the funded balance.

How did the dropped-KYC win-back flow work?

For the large pool of users who started KYC and abandoned it, we built a behavioural win-back flow — timed push and WhatsApp nudges that deep-linked each user straight back to the exact step they dropped on — and it recovered roughly 18% of abandoned applications. Every half-finished application is a user who has already shown high intent; they did not bounce on the install screen, they got partway through a demanding regulated flow and stalled. Recovering even a fraction of them is far cheaper than acquiring a fresh install. The win-back flow was the single highest-ROI workstream in the engagement on a per-rupee basis.

How it was built:

- Step-aware deep links: Because the funnel was now fully instrumented, the win-back system knew the precise step each user abandoned on. A user who dropped at document-upload received a different message — and a deep link to the document-upload screen with their prior progress intact — than a user who dropped at bank-linking. Generic "come finish your application" nudges convert poorly; "you are one step from trading — finish verifying your PAN" converts.

- Timed, behavioural sequencing: The nudges fired on a behavioural schedule — a gentle reminder within hours of abandonment while intent was still warm, a value-led message a day later, and a final reactivation attempt a few days on — rather than a single blast. Each message led with the reward (start trading) and the proximity to it, not the chore (finish KYC).

- WhatsApp as the primary channel: In India, WhatsApp open and response rates dwarf email and rival push for transactional, opted-in messaging. We ran the core of the win-back sequence over WhatsApp with compliant, templated messages, falling back to push and email. The channel choice mattered as much as the message — meeting Indian users where they actually read is half the battle.

- Friction-matched offers, sparingly: For the hardest-to-recover cohort — users who had abandoned more than once — a small, time-bound incentive (a brokerage-free first month, say) was layered on. We deliberately did not lead with incentives for everyone; most abandoners came back for the deep link and the reminder alone, and spending margin on users who would have returned anyway is waste.

Recovering ~18% of abandoned KYC applications is a large number when you consider the base it applies to — in a funnel where most starters were abandoning, the abandoned pool was the single biggest reservoir of recoverable, high-intent users in the entire business. The win-back flow turned a one-way exit into a second chance, and it kept working continuously in the background as new abandonment occurred. We have built this same step-aware recovery loop across fintech and edtech apps in our portfolio; the mechanics generalise because the underlying truth does — a user who got halfway through a hard flow is the warmest audience you will ever message.

How did activation feed early retention?

Fixing activation did not just produce more funded accounts and first trades — it lifted D30 retention from 12% to 20%, because a user who has funded an account and placed a real trade has a tangible reason to come back that a stalled, half-onboarded user never had. Activation and retention are not separate problems in a broking app; they are the same curve at two points. The strongest predictor of whether a user is still around at day 30 is whether they ever became a real, trading user in the first week. Get activation right and retention follows; get it wrong and no amount of re-engagement messaging will save a user who never experienced the product.

The mechanisms by which better activation compounded into better retention:

- A funded, invested user has skin in the game: A user with money in the account and a live position has a concrete reason to open the app tomorrow — to check that position. A user stuck at document-upload has none. Simply moving more users across the activation line mechanically lifted the retained base, before any retention-specific tactic was applied.

- The first trade created a reason for the second: Once a user had placed one trade through the guided flow, the next-best-action prompts — a watchlist movement, a relevant market event, a second-trade nudge — had something to anchor to. Re-engagement only works on users who have a behaviour to re-engage; the first trade created that behaviour.

- Early habit loops on the activated cohort: For users who had activated, we layered light, well-timed lifecycle messaging — portfolio-movement alerts, watchlist nudges around market opens, relevant news on held stocks — so the app earned a recurring reason to be opened. We deliberately restricted these to activated users; messaging a non-activated user about portfolio movements they do not have is noise that drives uninstalls.

- Closing the deferred-step loop: The steps we had deferred out of onboarding — nominee, additional segments, preferences — became gentle post-activation prompts that doubled as re-engagement touchpoints, deepening the account over the first month rather than front-loading friction.

The retention lift validated the entire thesis of the engagement. We did not run a separate retention campaign to move D30 from 12% to 20%; the retention improvement fell out of the activation work almost as a by-product, because the two are causally linked. This is the part most teams get backwards — they try to fix retention with notifications and offers aimed at users who never activated, when the real retention lever sits upstream in the activation funnel. The way to retain more users is to activate more of them properly in the first place. The compounding then runs forward: more activated users, better retained, with a longer revenue tail — which is precisely what reset the unit economics in the next section.

What were the final results across KYC, activation, and retention?

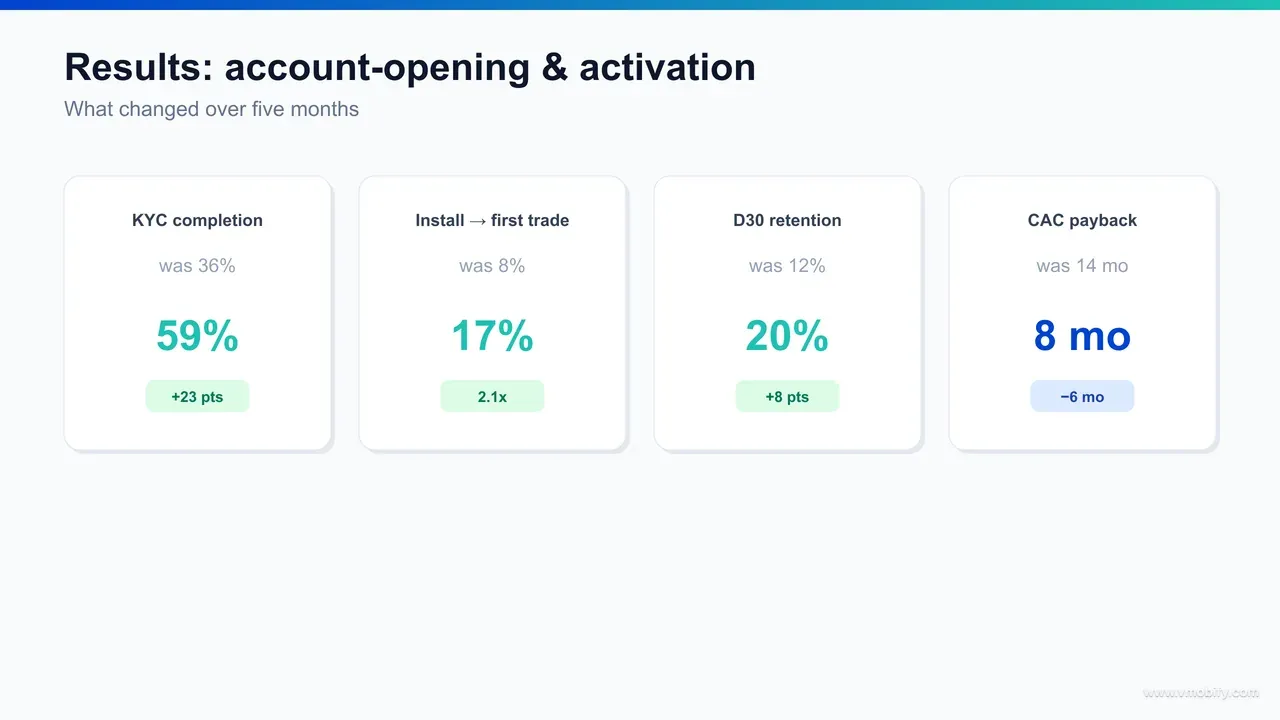

Over roughly five months, with no increase in acquisition spend, we took KYC completion from 36% to 59%, install-to-first-trade from 8% to 17%, D30 retention from 12% to 20%, recovered ~18% of abandoned KYC applications, and cut blended CAC payback from about 14 months to 8. Every gain came from the funnel between install and first trade — the part the acquisition team could not reach and the part nobody had instrumented. The consolidated results:

- KYC completion (start to complete): 36% → 59%. The document-upload rebuild plus onboarding compression and deferral did the bulk of this.

- Installs reaching a funded account: roughly 19% → over 30%. Because more users both started and completed KYC, the share of installs reaching a tradeable, funded account rose by more than half.

- Install-to-first-trade: 8% → 17%. The guided paper-trade-to-real-trade experience roughly doubled the activation rate.

- D30 retention: 12% → 20%. A by-product of more users becoming genuinely activated, not a separate retention campaign.

- Abandoned-KYC recovery: the win-back flow recovered roughly 18% of applications that had stalled mid-funnel.

- Blended CAC payback: ~14 months → 8 months. Same media spend, far more of it converting into funded, trading, retained users — which is what actually pays acquisition cost back.

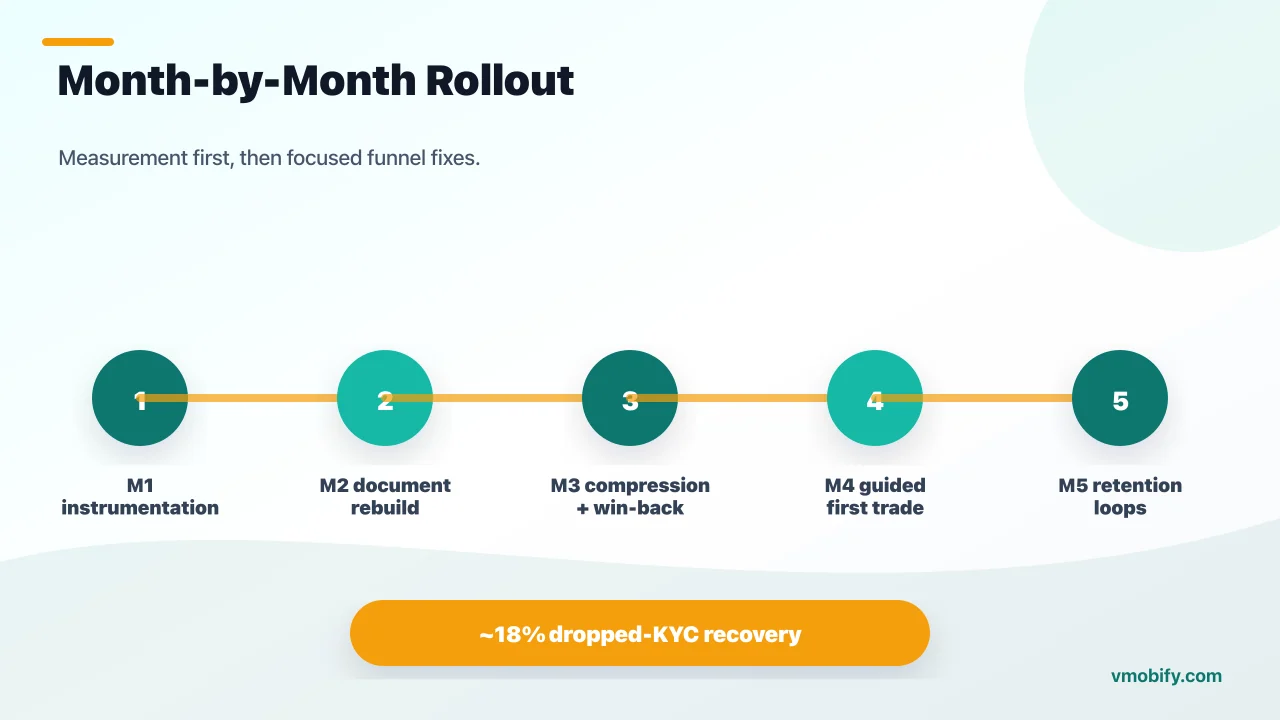

The month-by-month shape of the engagement:

- Month 1: Full funnel instrumentation. The fourteen-step event taxonomy goes live, funnel visualisation and segmentation are built, and session replay exposes the document-upload step as the largest leak. No UX changes yet — measurement first.

- Month 2: The document-upload and identity-verification rebuild ships — live capture guidance, specific errors, Aadhaar-OTP resilience, name-match handling. KYC completion starts climbing immediately; this is the single biggest step-level recovery of the project.

- Month 3: Onboarding compression and deferral go live — step count cut by roughly a third, progress bar added, non-essential steps moved past funding. Completion continues climbing toward the high-50s. The dropped-KYC win-back flow launches on WhatsApp and push.

- Month 4: The guided first-trade experience ships — paper trade, starter watchlist, scaffolded path to the first real order. Install-to-first-trade begins its climb from 8% toward the mid-teens.

- Month 5: The activated-cohort retention loops mature, D30 retention settles at 20%, the win-back flow reaches steady-state ~18% recovery, and the improved activation works through to an 8-month CAC payback. The funnel is now a compounding system rather than a leaky bucket.

Two observations future teams should internalise. First, the cheapest growth was already inside the funnel — the same installs, activated properly, transformed the economics without a single extra rupee of media spend. Second, activation is the master variable — KYC completion, first-trade rate, retention, and payback all moved together because they are links in one chain, and the chain is only as strong as the activation funnel that feeds it. You can see the same systems thinking across our portfolio of case studies, including our companion stock-broker app growth case study on the acquisition side of the same vertical.

What makes this activation playbook repeatable?

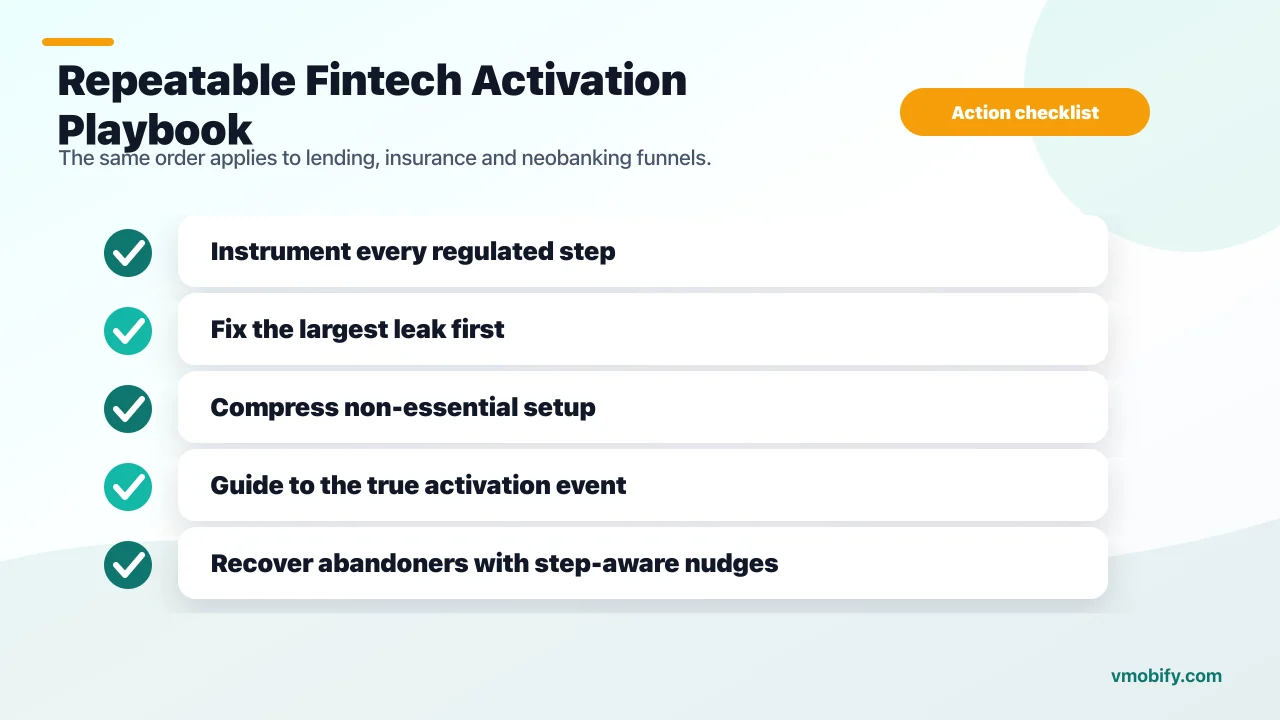

This playbook is repeatable because it is a method, not a set of one-off fixes — instrument the full funnel, find the few catastrophic drop-off steps, rebuild them, compress and defer everything non-essential, guide the user to the true activation event, and recover the abandoners. The specific screens change between apps; the sequence and the principles do not. Any app with a long, friction-dense funnel between install and value — broking, lending, neobanking, insurance, even high-consideration commerce — can run the same method and get a similar shape of result.

The transferable principles, in the order they create value:

- Instrument before you optimise. The headline conversion number is always an average hiding a few terrible steps. Granular, step-level instrumentation is what turns an unfixable "our funnel converts badly" into a fixable "these two screens are killing us". This is non-negotiable and it comes first.

- Fix the biggest leak first. Resist the urge to redesign everything. Find the single largest drop-off step, rebuild that, ship it, measure, then move to the next. The document-upload fix delivered more than the rest of the funnel work combined precisely because it was attacked first and in isolation.

- Shorten the path to value. Defer every step that does not legally or functionally have to happen before the user reaches the core experience. The shortest compliant path always out-converts the complete-but-front-loaded one.

- Engineer the true activation moment. Identify the action that actually predicts retention — here, the first trade, not the funded balance — and build a guided, fear-removing path to it. Activation is a sequence of confidence thresholds, and the last one is usually the one teams forget to design.

- Recover the abandoners. Step-aware, behaviourally-timed win-back over the channel your users actually read is the highest-ROI growth available, because the abandoned pool is your warmest possible audience. Never let a half-finished application be a one-way exit.

- Let retention fall out of activation. Do not try to retain users you never activated. Fix activation and the early-retention curve lifts with it; then layer light, activated-only lifecycle loops on top.

The reason this method generalises is that the underlying behaviour generalises. A user mid-way through any hard, deferred-value flow behaves the same whether they are opening a demat account or a credit line — high intent, fragile patience, one tap from quitting, and recoverable if you meet them at the exact step they stalled on. We have run versions of this funnel-rebuild across fintech and beyond in our portfolio, and the structure holds every time even as the regulatory details and the specific friction screens change.

Who built this, and how would it map to your app?

Vmobify has managed app growth for Indian and global publishers since 2013, across 300+ apps in fintech, gaming, OTT, edtech, news, and utility — and the reason we could fix this app's activation funnel is that we treat acquisition, activation, and retention as one connected system rather than three separate disciplines. Most agencies stop at the install. The interesting, economically decisive work usually starts there.

- We optimise toward activation, not vanity installs: A cheap install that never funds an account is a cost, not a customer. Every engagement we run points at the deepest meaningful event — here, the funded account and the first trade — which is the discipline at the core of our user acquisition and analytics practice.

- Instrumentation is a first-class deliverable: We do not optimise blind. A properly instrumented funnel is the foundation of every activation win, and we build it before we touch a single screen. The drop-off you cannot see is the one quietly bankrupting your CAC payback.

- India is our home market: The team works out of India, understands the KYC, demat, and regulatory landscape — SEBI, RBI, the Aadhaar and PAN rails — and knows that WhatsApp, device tiers, and Tier-2/3 connectivity are not edge cases but the centre of the Indian market. International agencies spend their first quarter relearning what we start with.

- The portfolio compounds: Fintech activation learnings cross-pollinate with edtech (trust-driven, deferred-value funnels), with gaming (first-session activation), and with commerce (cart-to-checkout recovery). No single-vertical agency builds that lateral muscle.

- Case studies, not promises: Every engagement is followed by a write-up like this one. The portfolio is the proof — you can read the companion fintech app marketing guide for India and our stock-broker growth case study for the acquisition side of the same vertical.

If you are running a broking, lending, neobanking, or insurance app in India and your installs are not turning into funded, active, retained customers, the problem is almost certainly not your media buying — it is the funnel underneath it. The keyword set, the regulatory framing, and the specific friction screens change between apps; the method — instrument, find the leak, rebuild it, compress, guide to activation, recover the abandoners — does not. Talk to Vmobify's growth team to see how this activation playbook would map to your app.

Frequently Asked Questions

Was the problem acquisition or activation?+

Activation. The app was already buying installs efficiently — the leak was the account-opening funnel underneath. Only 36% of users who started KYC finished it, so barely 19% of installs ever reached a funded account, and just 8% placed a first trade. The fix was rebuilding the funnel, not buying more installs.

How did you lift KYC completion from 36% to 59%?+

Three things, in order of impact: full funnel instrumentation that exposed the document-upload step as the biggest leak; a rebuild of that step with live capture guidance, specific error states, and Aadhaar-OTP resilience; and onboarding compression that cut the step count by roughly a third, added a progress bar, and deferred every non-essential step past the funding moment. Every regulatory check still happens — we only changed sequencing and UX.

What is the single highest-impact change you made?+

Instrumenting the funnel first. The 36% completion rate was an average hiding two or three catastrophic steps. Once the document-upload step was visible as the largest leak, fixing it recovered more completion than any other change. You cannot fix a drop-off you cannot see — measurement before optimisation is the whole method.

How did the guided first-trade experience double activation?+

A newly funded user landing on a blank trading terminal freezes. We replaced it with a risk-free paper trade, a pre-populated starter watchlist, and a scaffolded path from the simulated trade to the first real order — with education delivered inline at the point of action. Removing the fear of the first order took install-to-first-trade from 8% to 17%.

How did the win-back flow recover 18% of abandoned applications?+

Because the funnel was fully instrumented, the win-back system knew the exact step each user abandoned on and could deep-link them straight back to it with progress intact. Behaviourally-timed nudges — primarily over WhatsApp, with push and email fallback — led with the reward (start trading) and the proximity to it, not the chore. The abandoned pool is the warmest audience in the business, which is why per-rupee this was the highest-ROI workstream.

Why did retention improve without a separate retention campaign?+

Because activation and early retention are the same curve at two points. A user who has funded an account and placed a real trade has a concrete reason to come back; a user stalled at document-upload has none. Moving more users across the activation line mechanically lifted D30 retention from 12% to 20% — the retention gain fell out of the activation work.

Can this playbook work for a lending, neobanking, or insurance app instead of broking?+

Yes. Any app with a long, friction-dense, deferred-value funnel between install and value runs the same method: instrument the full funnel, fix the biggest leak first, compress and defer non-essential steps, engineer a guided path to the true activation event, and recover the abandoners. The regulatory framing and the specific friction screens change; the structure does not.

Sources

- SEBI — Statistics & Demat Data — Official source on demat-account growth and the regulated account-opening process in India

- RBI — Master Direction on KYC — The regulatory basis for the identity-verification steps in the account-opening funnel

- AppsFlyer — Performance Index — Benchmarks for onboarding conversion, activation, and retention by vertical and geography

- Adjust — Resources & Onboarding Research — Industry research on onboarding step-count, drop-off, and activation

- Amplitude — Product Analytics — Reference on step-level funnel analysis and segmentation methodology

- Google Play — Launch Best Practices — Google's guidance on onboarding, retention, and engagement signals

- AppTweak — ASO & Growth Research — Independent benchmarks on fintech conversion and engagement dynamics

- AppsFlyer — State of App Marketing — Cross-vertical data on cost-per-install, activation, and CAC payback

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy