Bill Payment App Retention: 27% to 43% Repeat Payments

An Indian bill-payment and recharge app could acquire users at scale but could not keep them — most paid once and lapsed. Acquisition was never the problem; repeat usage was. Over four months we rebuilt the lifecycle: bill-due reminders across push and WhatsApp, a UPI Autopay mandate-adoption programme, rewards and streaks for repeat payers, and behavioural 30/60/90-day win-back sequences. Month-1 repeat-payment rate climbed from 27% to 43%, D30 retention from 9% to 17%, UPI Autopay adoption from 11% to 29%, monthly churn fell roughly 30%, and reactivation campaigns recovered about 22% of lapsed users. Here is the full retention playbook.

What was the brief and the starting position?

An Indian bill-payment and recharge app came to us with the opposite of the usual problem: acquisition was working, but retention was not — the app could pour in installs, yet most users paid a single bill or recharge once and never came back. The growth chart looked healthy at the top and hollow underneath. New installs climbed every month while the transacting base barely moved, because almost everyone who arrived left through the same door within thirty days.

The numbers were stark. Month-1 repeat-payment rate — the share of new users who completed a second payment within their first month — sat at just 27%. D30 retention was 9%. UPI Autopay / e-mandate adoption, the structural lever that should make recurring bills automatic, was stuck at 11%. The overwhelming majority of users transacted once and lapsed. The company had spent two years and a large media budget building an acquisition machine, and it was quietly leaking almost everything that machine brought in.

This is deliberately a different case study from our bill-payment app acquisition playbook, where the brief was volume — 10M+ installs in eight months. That one was about getting users in. This one is about keeping them. The lever here was never another acquisition channel; it was lifecycle, CRM, and UPI Autopay adoption. The client had already proven they could buy a first transaction. What they could not do was earn the second, third, and tenth.

The success metric we agreed on was repeat behaviour, not installs. Specifically: lift the month-1 repeat-payment rate, lift D30 retention, and — most importantly — push far more users onto UPI Autopay, because a user whose electricity, DTH, broadband, or FASTag bill runs on an automatic mandate is a user who has effectively pre-committed to staying. Across our 300+ apps managed since 2013, we have seen this exact pattern in fintech repeatedly: the apps that win are never the ones with the cheapest installs, they are the ones that convert a first transaction into a habit. This is the story of how we did that over roughly four months.

Why do bill-payment apps live or die on repeat transactions?

Bill-payment apps live or die on repeat transactions because the headline action is low-margin, the bills are inherently recurring, and the entire unit economics only work if a user pays through you again and again — a one-time payer is a guaranteed loss. The maths is unforgiving. Acquiring and onboarding a user in a regulated payments category costs real money; the margin on a single ₹800 electricity bill or a ₹239 recharge is a few rupees at best. You do not recover acquisition cost on the first transaction. You recover it on the twelfth.

That makes retention the whole business, not a nice-to-have. Five structural reasons make repeat behaviour the make-or-break metric:

- The action is naturally recurring, so churn is a choice the product allows: Electricity, gas, broadband, DTH, postpaid mobile, FASTag, rent — these bills recur every single month whether the user pays through your app or a competitor's. The demand never disappears. If a user lapses, it is because the app failed to be present at the next billing moment, not because the need went away.

- Margins forbid buying loyalty: Unlike a high-LTV lending or gaming app, a bill-payment app cannot afford expensive perpetual incentives. Retention has to come from utility and timing, not from burning cash on every transaction.

- The incumbents own the default habit: A handful of super-apps are the reflexive choice for recharges and bills. A new payer who lapses does not go dormant — they default back to the incumbent, and winning them back a second time is harder than the first.

- Autopay is destiny: India's UPI Autopay framework, run by NPCI, lets users set standing e-mandates for recurring payments. A user on autopay is retained by design — the bill runs itself. A user paying manually every month is one busy week away from churning.

- Retention compounds where acquisition does not: Industry data is blunt on this. AppsFlyer's retention benchmarks show finance-app D30 retention sitting in the single-digit-to-low-teens range for most markets — meaning small absolute gains in repeat rate translate into outsized changes in the transacting base over time.

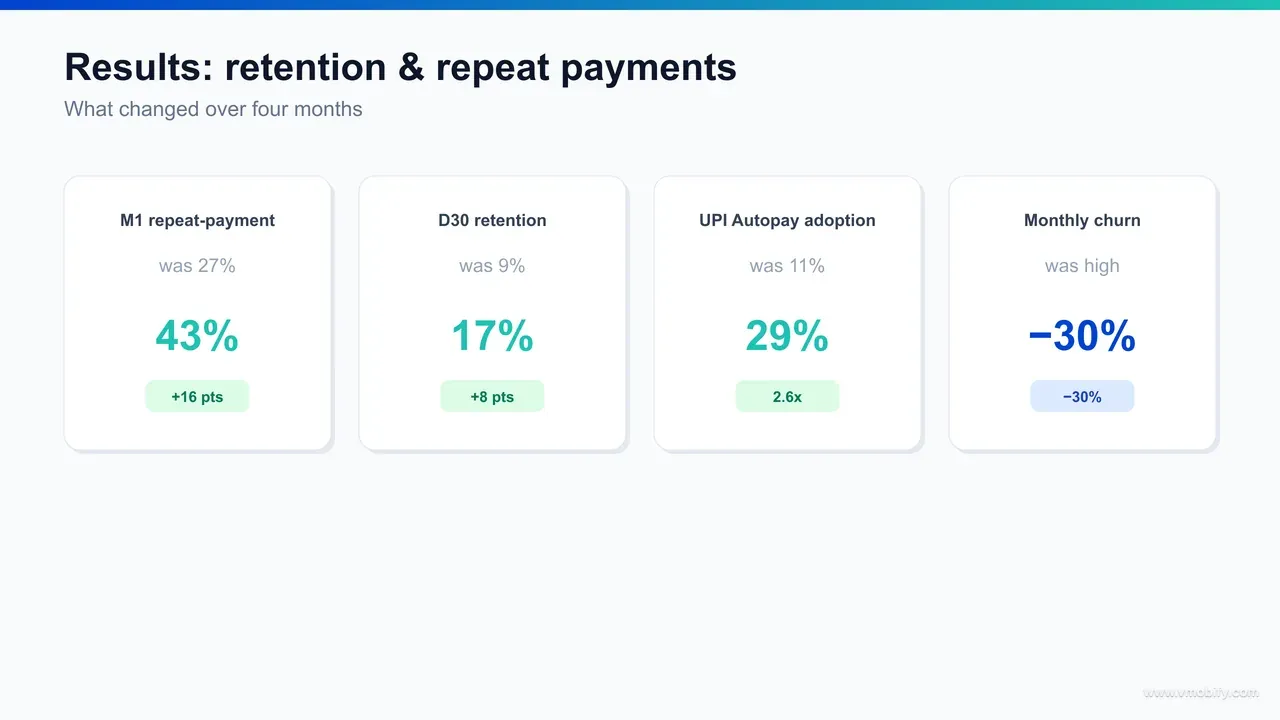

The figure below shows the before-and-after on the four KPIs we set out to move. The starting position — 27% month-1 repeat, 9% D30, 11% autopay — is a classic "leaky bucket". No amount of pouring more installs into the top fixes a bucket leaking that fast at the bottom. Fixing the bucket was the entire engagement.

How did we segment and instrument retention before changing anything?

Before sending a single new message, we rebuilt the measurement layer — a clean lifecycle event taxonomy and a segmentation model by biller type and recency — because you cannot improve a repeat rate you cannot see, and the app's existing analytics could not tell a lapsed user from a loyal one. Most retention failures are measurement failures first. The app knew how many installs it had and how much it processed; it did not know, for any individual user, when their next bill was due, which billers they used, or how many days since their last payment.

The instrumentation work, in order:

- A lifecycle event taxonomy: We wired a proper event hierarchy — install, registration, payment-method added, first payment, biller saved, repeat payment, mandate created, mandate paused, lapse. Without these firing reliably into the analytics and CRM stack, every downstream campaign would be flying blind. Our mobile analytics team owns this layer precisely because a mis-fired lifecycle event silently corrupts every segment built on top of it.

- Segmentation by biller type: An electricity-bill payer and a one-off mobile recharger are completely different retention problems. Electricity, broadband, DTH, gas, and FASTag are predictable monthly commitments — ideal autopay candidates. Recharges are spikier. We segmented every user by their dominant biller category so messaging could match the cadence of the actual bill.

- Segmentation by recency: Using an RFM-style model (recency, frequency, monetary value), we split the base into active, at-risk (no payment in 20-30 days), and lapsed (30/60/90+ days). Recency is the single strongest churn predictor in a recurring-payment app — a user 25 days past their last electricity payment is about to either pay or defect.

- Cohort retention curves: We rebuilt cohort analysis in Amplitude so we could watch each weekly install cohort's decay curve and see whether interventions flattened it. The starting curves had a brutal cliff: a steep drop between the first and second transaction, then a long flat tail of the few who survived.

This phase produced no visible "growth" — and it is the phase most teams skip in their hurry to send campaigns. But every percentage point we later moved traces back to a segment we could only target because the instrumentation existed. In our portfolio, the retention programmes that work are always the ones that spend the first three weeks measuring before they spend a rupee messaging.

How did bill-due reminders across push and WhatsApp drive repeat payments?

Bill-due reminders were the highest-impact lever in the entire programme because they brought users back at the exact moment of natural billing intent — and a reminder timed to a real due date converts many times better than a generic re-engagement blast sent because a calendar said so. The insight is simple: in a recurring-payment app, you do not need to manufacture a reason to return. The bill is the reason. You just have to be present when it lands.

How the reminder engine worked:

- Due-date prediction per biller: Using saved billers and historical payment dates, we predicted each user's next due date per biller and built a reminder window around it — a heads-up a few days before, a reminder on the due date, and a gentle nudge if still unpaid after it. The reminder was specific: "Your [biller] bill of approximately ₹X is due on [date]." Specificity is what separates a useful reminder from spam.

- Push for the active, WhatsApp for everyone: Push notifications carried the active, opted-in users, but push delivery and open rates in India are structurally weak — capped notification permissions, aggressive battery managers on budget Android devices, and notification fatigue. So WhatsApp became the primary reminder rail. As an opt-in Business channel, it lands in the one inbox Indian users actually check, with open rates that dwarf push. Braze's channel research and our own data both put WhatsApp open rates far ahead of push for transactional, time-sensitive messages.

- One-tap payment from the message: Every reminder deep-linked straight into the pre-filled payment screen for that biller — biller selected, amount fetched, user one tap from done. Each extra screen between the reminder and the completed payment bled conversion. We instrumented and removed that friction relentlessly.

- Frequency capping and quiet hours: We capped reminder volume hard and respected quiet hours. The fastest way to destroy a WhatsApp channel is to get reported as spam and lose the number's quality rating, so restraint was a feature, not a limitation.

The effect on D30 retention was the largest single contributor to the programme. A user reminded about a real bill they genuinely needed to pay, with a one-tap path to pay it, came back — and each return was another chance to deepen the habit. This is the same lifecycle discipline we detail in our app re-engagement and win-back guide: relevance and timing beat volume every time.

How did the UPI Autopay nudge programme turn one-time payers into recurring ones?

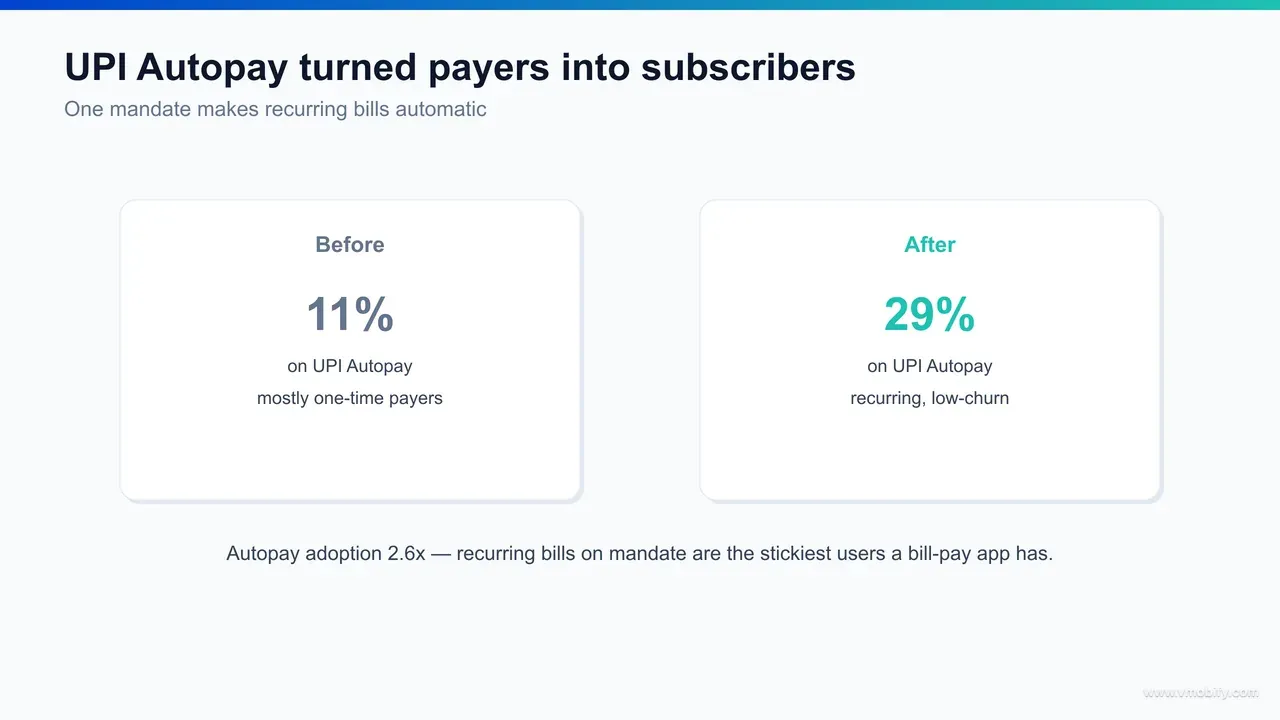

The UPI Autopay nudge programme was the structural fix — instead of reminding a user to pay every single month, we got them to set a one-time e-mandate so the recurring bill paid itself, converting a fragile manual habit into a durable automatic one and lifting autopay adoption from 11% to 29%. A reminder is a recurring cost and a recurring risk; a mandate is a one-off action that retains the user indefinitely. Moving users from the first to the second was the most valuable thing the programme did.

The mechanics of the nudge programme:

- Targeting the right bills: We did not nudge everyone toward autopay — that would have annoyed recharge-only users. We targeted users with predictable, stable-amount recurring bills: postpaid mobile, broadband, DTH, electricity, and FASTag recharges. These are the bills where an e-mandate genuinely removes a monthly chore, so the value proposition is honest.

- Timing the ask to the moment of proven intent: The worst time to pitch autopay is during onboarding, when trust is lowest. The best time is immediately after a successful manual payment — the user has just experienced the app working, the friction is fresh in memory, and "never do this manually again" lands. We fired the autopay prompt right after the second or third successful payment for that biller.

- Explaining the e-mandate honestly: Autopay adoption stalls on fear — users worry about losing control of their money. We addressed it head-on in the copy: clear caps on the maximum debit amount, a pre-debit notification, and one-tap pause/cancel. The UPI Autopay e-mandate framework for recurring e-mandates already mandates pre-debit notifications and amount caps; we surfaced those protections as selling points rather than burying them.

- Reducing mandate-setup friction: We streamlined the e-mandate creation flow and instrumented every drop-off step. A mandate abandoned halfway is worse than never asking, so the flow had to be as close to one-tap as the UPI rails allow.

An autopay user is the closest thing a bill-payment app has to a subscriber, and we treat the economics the same way we treat subscription retention — the structural parallels are why we wrote our UPI Autopay for app subscriptions guide. Every percentage point of autopay adoption is a percentage point of the base that simply does not need to be re-won each month. Pushing adoption from 11% to 29% effectively moved a large slice of the base from "at risk every month" to "retained by default", and it is the single most defensible gain in the whole engagement.

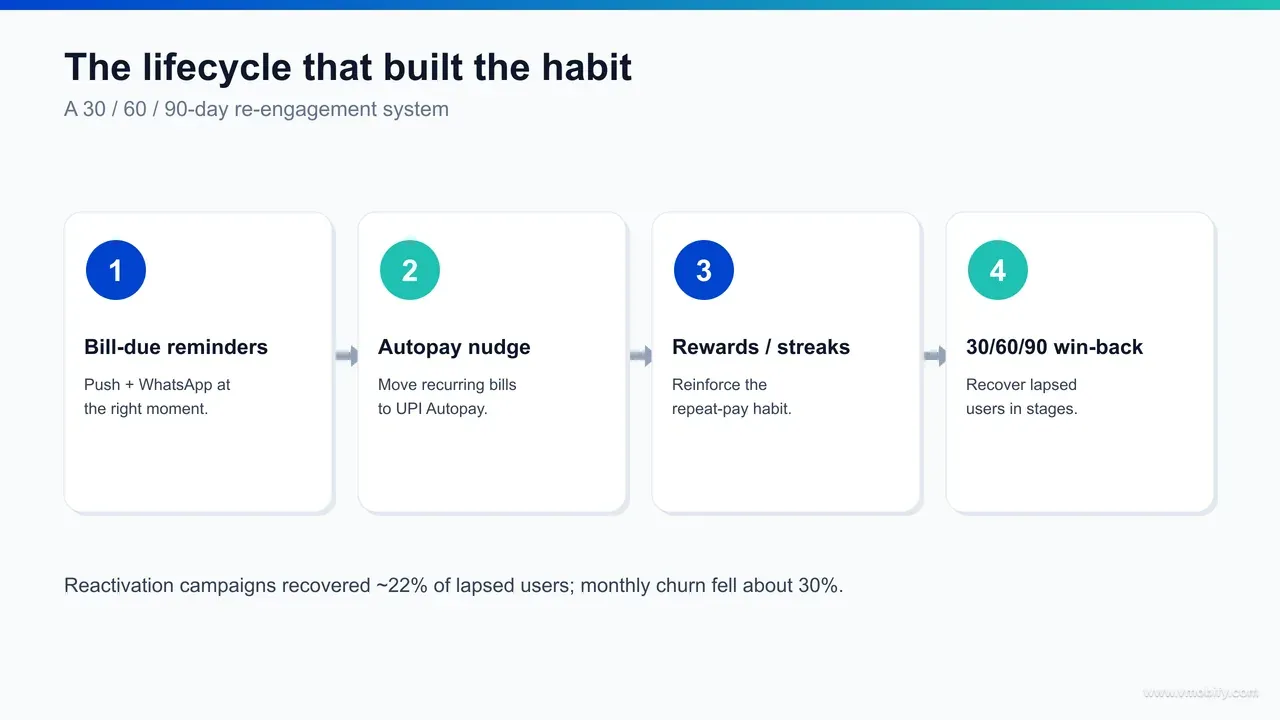

How did the 30/60/90-day win-back sequences recover lapsed users?

The behavioural 30/60/90-day win-back sequences recovered roughly 22% of lapsed users by treating recovery as a graduated, escalating conversation rather than a single "we miss you" blast — and recovering a once-transacted user proved far cheaper than acquiring a fresh install. A user who has already paid once through the app has cleared every hard hurdle: download, registration, KYC, payment-method setup, and the trust barrier of routing money through a non-incumbent. Letting them lapse permanently throws all of that sunk effort away.

The sequence was built on recency triggers, with the message escalating as the lapse deepened:

- Day 30 — the gentle, utility-led nudge: When a user crossed 30 days without a payment, the first touch was purely helpful and zero-pressure: "Your [biller] bill may be due soon — pay in one tap." No discount, no guilt. At this stage most lapses are simply forgetfulness or a single missed billing cycle, and a well-timed, relevant reminder recovers a meaningful share on its own.

- Day 60 — the value reminder plus a small incentive: Users still dormant at 60 days got a sharper message that reminded them what the app does well — speed, saved billers, autopay — paired with a small, time-bound cashback on their next payment. The incentive is deliberately modest and reserved for this stage, not sprayed across the active base.

- Day 90 — the last, strongest offer before suppression: At 90 days we made the strongest single offer, framed as a genuine "come back" moment, then suppressed non-responders from further win-back messaging to protect the WhatsApp channel quality and avoid spam reports. Knowing when to stop is as important as knowing when to send.

- Channel and language matched to the segment: Each step ran on whichever channel the user historically engaged with, in their preferred language, with a one-tap path back to the exact bill they used to pay.

The figure below shows the lifecycle architecture — how active, at-risk, and lapsed users flowed between states and which message fired at each transition. The win-back layer matters because, as MoEngage's retention research repeatedly shows, re-engaging an existing user costs a fraction of acquiring a new one. Recovering 22% of lapsed users — people the acquisition budget had already paid for once — was pure margin recovered from a leak the business had simply been tolerating.

How did rewards and streaks reinforce the repeat-payment habit?

Rewards and streaks reinforced the habit by giving the recurring action a small, predictable emotional payoff — turning a chore into a routine the user actively maintained — but we engineered them so loyalty came from utility and momentum, not from a cashback war the margins could never sustain. The trap in a low-margin payments category is buying repeat behaviour with ever-larger incentives until the unit economics collapse. We deliberately designed the rewards layer to build habit cheaply rather than to bribe transactions expensively.

The design that worked:

- Payment streaks tied to billing cycles: A streak that counted consecutive on-time monthly payments gave users a reason to keep the chain unbroken. Streaks exploit a well-understood behavioural bias — people are loss-averse about breaking a run they have built. The reward for maintaining a streak was modest; the motivation was the streak itself.

- Milestone rewards, not per-transaction cashback: Rather than discounting every payment, we rewarded milestones — the third, sixth, and twelfth consecutive month — so the cost was bounded and the reward landed at moments that deepened commitment. A bounded, milestone-based structure is far kinder to margins than blanket cashback.

- Scratch-cards and surprise rewards on repeat payments: Variable, occasional rewards — a small scratch-card after a payment — drove more repeat engagement per rupee than a fixed, expected discount, because intermittent reward schedules are psychologically stickier than predictable ones. The expected value per transaction stayed tiny; the engagement lift did not.

- Status for autopay users: We gave autopay users a visible "auto-paid" status and protected their streaks automatically, reinforcing the autopay decision and making the most-retained segment feel rewarded for being there.

The rewards layer was never the headline lever — reminders and autopay did the heavy lifting — but it was the connective tissue that made the habit feel worth maintaining between bills. We deliberately kept it on the right side of the margin line, which is also why we think about it alongside monetisation rather than as a pure cost centre: a reward that increases lifetime transaction count more than it costs is not a discount, it is an investment. In our portfolio, the rewards programmes that survive are always the ones engineered for habit, not the ones engineered for a short-term transaction spike.

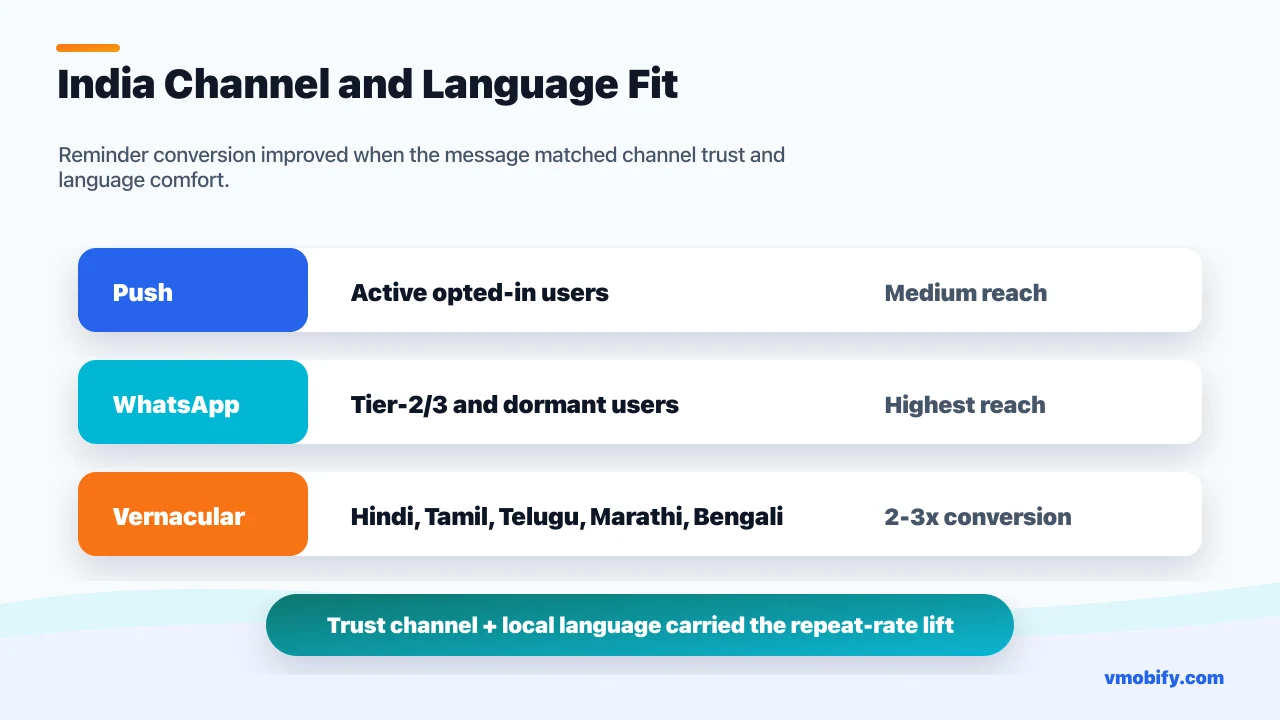

Why was vernacular WhatsApp messaging the unlock for Tier-2/3 users?

Vernacular WhatsApp messaging was the unlock for Tier-2/3 users because the bulk of India's next-wave bill-payers do not read marketing English comfortably, distrust generic notifications, and live inside WhatsApp — so a reminder in Hindi, Tamil, Telugu, Marathi, or Bengali on the channel they already trust converted several times better than an English push they ignored. The retention gap was not evenly distributed across the base. Tier-1 metro users churned for ordinary reasons; Tier-2/3 users churned because the app was, in effect, speaking a language they had to translate before they could act.

What the vernacular layer involved:

- Language inferred and respected per user: We inferred preferred language from region, device language, and onboarding signals, then sent every lifecycle message — reminders, autopay nudges, win-back — in that language. A bill reminder a user can read instantly is a bill reminder a user acts on instantly.

- WhatsApp as the trusted channel: For Tier-2/3 users especially, a WhatsApp message from a verified business sender carries trust that a system push notification does not. It looks like a message, not an ad, and it lands where the user already spends their time. The combination of trusted channel and native language is multiplicative, not additive.

- Culturally and locally accurate copy: We localised properly — not machine-translated string-swaps, but copy reviewed by native speakers for the right register and the right framing of money and trust. Clumsy translation in a payments context erodes exactly the trust the message needs.

- Vernacular autopay education: The autopay nudge, in particular, depended on the user understanding the e-mandate protections. Explaining caps, pre-debit alerts, and one-tap cancellation in the user's own language was what moved Tier-2/3 autopay adoption, where the fear barrier was highest.

India is not one market, and a retention programme that treats it as one English-speaking market leaves most of the upside on the table. The vernacular WhatsApp layer carried a disproportionate share of the 16-percentage-point repeat-rate gain, concentrated exactly in the Tier-2/3 cohorts that the English-only programme had been quietly failing. Being an India-native team — running creative and CRM copy in Indian languages by default — is why we reach for this lever first, not last.

What were the final retention and autopay results?

Over roughly four months, month-1 repeat-payment rate rose from 27% to 43%, D30 retention nearly doubled from 9% to 17%, UPI Autopay adoption climbed from 11% to 29%, monthly churn fell about 30%, and the win-back sequences recovered around 22% of lapsed users — all without changing the acquisition spend by a single rupee. The headline numbers, consolidated:

- Month-1 repeat-payment rate: 27% → 43% — a 16-percentage-point lift in the share of new users who complete a second payment in their first month.

- D30 retention: 9% → 17% — almost doubled, driven by bill-due reminders landing at moments of real billing intent.

- UPI Autopay / e-mandate adoption: 11% → 29% — the most durable gain, moving a large slice of the base to retained-by-default.

- Monthly churn: down roughly 30% as one-time payers converted into recurring ones and the cohort decay curve flattened.

- Lapsed-user reactivation: approximately 22% of lapsed users recovered through the 30/60/90-day sequences — margin recovered from users already paid for once.

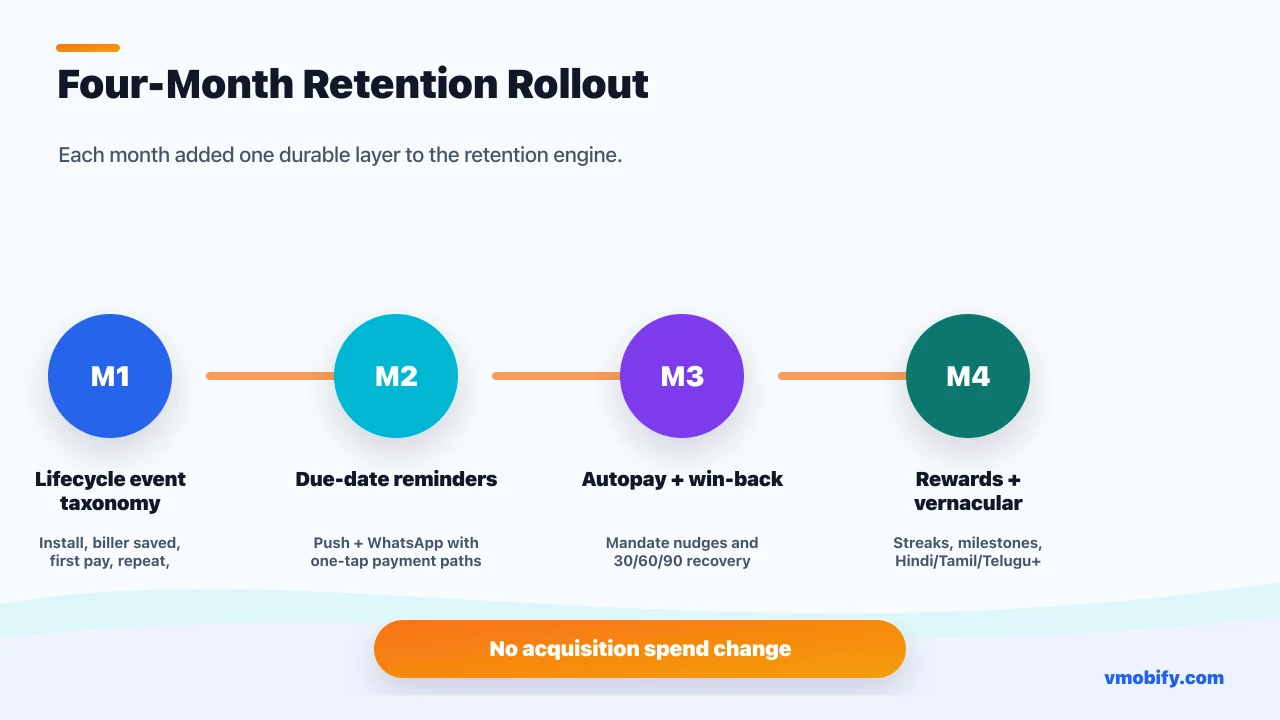

The month-by-month shape of the engagement:

- Month 1: Instrumentation. Lifecycle event taxonomy wired and verified, biller-type and recency segmentation built, cohort curves rebuilt. No visible growth — the foundation phase. Reminder and win-back flows designed but not yet live at scale.

- Month 2: Bill-due reminders go live across push and WhatsApp. D30 retention is the first metric to move as users return at real due dates. Vernacular templates ship for the top five languages. WhatsApp becomes the primary reminder rail.

- Month 3: The UPI Autopay nudge programme launches, fired after the second or third successful payment per biller. Autopay adoption begins its climb. The 30/60/90-day win-back sequences activate against the lapsed base. Rewards and streaks layer on to reinforce the active cohort.

- Month 4: Compounding. Autopay adoption crosses into the high twenties, repeat rate reaches 43%, churn settles roughly 30% below baseline. The base is now self-reinforcing — a growing share of payments run automatically, and the reminder/win-back machine catches the rest.

Two observations future teams should internalise. First, retention is won at the second transaction, not the first — the entire programme was engineered to move users across the cliff between payment one and payment two, because everything after that is far easier. Second, autopay is the only truly durable lever — reminders and win-back recover users repeatedly, but an e-mandate retains them without any further work. You can see the same systems thinking across our portfolio of case studies: the durable wins come from changing the structure of the relationship, not from sending more messages.

What makes this retention playbook repeatable?

This playbook is repeatable because it is a system built on the structure of recurring payments, not a set of clever one-off campaigns — and the single most repeatable element is autopay adoption, because converting a manual payer into an e-mandate holder permanently changes the retention equation in any recurring-payment category. The variables change between apps; the structure does not.

- Instrument before you message: Every gain traced back to a segment we could only act on because the lifecycle taxonomy and recency model existed. The first move in any retention engagement is measurement, and it is the move teams most often skip.

- Be present at the moment of natural intent: In any recurring-payment app, the demand recurs on its own. The job is presence and timing — a relevant message on the right channel at the real due date — not manufactured re-engagement.

- Move users from manual to automatic: Autopay is the structural endgame. A reminder is a recurring cost; a mandate is a one-time action that retains indefinitely. The infographic below shows the autopay adoption curve — 11% to 29% — and that single line is the most defensible asset the engagement produced.

- Match channel and language to the user: WhatsApp over push, vernacular over English, one-tap over multi-screen. The mechanics are universal; the execution must be India-native to capture Tier-2/3.

- Engineer rewards for habit, not for spikes: Bounded, milestone- and streak-based rewards build durable behaviour without starting a cashback war the margins cannot win.

The keyword set, the biller categories, and the regulatory framing shift between a recharge app, a rent-payment app, a SIP/investment app, or a lending EMI app — but the lifecycle structure, the autopay-first mindset, and the channel discipline carry across all of them. That portability is why we treat retention as a system, not a campaign.

Who is Vmobify and why does this playbook hold across verticals?

Vmobify has managed app marketing and lifecycle programmes for Indian and global publishers since 2013, across 300+ apps in fintech, gaming, OTT, edtech, news, and utility — and this retention playbook holds across verticals because it is grounded in the structure of recurring behaviour, which repeats everywhere even when the product does not. The reason the same approach works for a bill-payment app, an OTT subscription, and an edtech course renewal is that all three live or die on the second transaction, not the first.

- We optimise toward repeat behaviour, not vanity installs: This engagement never touched acquisition. The lever was lifecycle, CRM, and autopay adoption — the levers that actually compound. Optimising toward installs is how agencies produce big, hollow numbers; optimising toward repeat transactions is how you build a durable base. That discipline anchors our analytics and monetisation practice.

- India is our home market: We run CRM in Indian languages by default, understand UPI, BBPS, and the RBI e-mandate framework, and have the Tier-2/3 nuance international agencies spend their first three months relearning. The vernacular WhatsApp layer in this case study is not a bolt-on for us — it is the default.

- Retention and acquisition are one system: We ran the acquisition side of this same category, documented in our bill-payment acquisition case study. Knowing how a user was acquired makes retaining them sharper, and vice versa.

- The portfolio compounds: Fintech retention learnings cross-pollinate with OTT (subscription win-back), edtech (renewal nudges), and gaming (streak mechanics). No single-vertical agency builds that lateral muscle.

If you have an acquisition machine that works but a retention problem that does not — users who pay once and vanish, autopay adoption stuck in single or low double digits, a churn curve that cliffs after the first transaction — this playbook adapts to your vertical. Talk to Vmobify's growth team to see how it would map to your app.

Frequently Asked Questions

How much did month-1 repeat-payment rate actually improve, and over what time?+

Month-1 repeat-payment rate rose from 27% to 43% over roughly four months — a 16-percentage-point lift. It came entirely from lifecycle CRM and UPI Autopay adoption, with no change to acquisition spend. The biggest single driver was bill-due reminders landing at real billing moments with a one-tap path to pay.

Why is UPI Autopay adoption such an important retention metric for a bill-payment app?+

Because an autopay user is retained by design. Once a recurring bill runs on a UPI e-mandate, the payment happens automatically every cycle without the user choosing your app again — so churn risk drops to near zero for that biller. Moving adoption from 11% to 29% shifted a large slice of the base from at-risk-every-month to retained-by-default, which is the most durable gain in the whole programme.

Why use WhatsApp instead of push notifications for bill-due reminders?+

Push delivery and open rates in India are structurally weak — capped notification permissions, aggressive battery managers on budget Android devices, and notification fatigue. WhatsApp, as an opt-in Business channel, lands in the inbox Indian users actually check, with far higher open rates for time-sensitive transactional messages. We used push for active opted-in users and WhatsApp as the primary rail, especially for Tier-2/3 users.

How did the 30/60/90-day win-back sequences work, and how many users did they recover?+

They recovered roughly 22% of lapsed users by escalating gradually: a gentle utility-led reminder at day 30, a value reminder plus a small time-bound incentive at day 60, and the strongest single offer at day 90 before suppressing non-responders to protect channel quality. Recovering a once-transacted user is far cheaper than acquiring a fresh install because they have already cleared KYC, payment setup, and the trust barrier.

Did you raise retention by spending more on acquisition or on cashback?+

Neither. Acquisition spend never changed — this was purely a retention engagement. And rewards were engineered for habit, not bribery: bounded milestone rewards, payment streaks, and occasional scratch-cards rather than blanket per-transaction cashback. In a low-margin payments category, a cashback war is unsurvivable, so the gains came from timing, relevance, autopay, and channel discipline.

Why did vernacular messaging matter so much for the results?+

Because the bulk of India's next-wave bill-payers do not read marketing English comfortably and live inside WhatsApp. A reminder or autopay nudge in Hindi, Tamil, Telugu, Marathi, or Bengali on a trusted channel converted several times better than an English push that users ignored. The vernacular WhatsApp layer carried a disproportionate share of the 16-point repeat-rate gain, concentrated in Tier-2/3 cohorts.

Can this retention playbook work for a SIP, lending, or subscription app instead of bill payments?+

Yes, with adaptations. The biller categories, keyword set, and regulatory framing change, but the structure holds: instrument the lifecycle, segment by recency and product, be present at the moment of natural intent, move users from manual to automatic (autopay / e-mandate), run graduated win-back, and match channel and language to the user. Any recurring-payment category lives or dies on the second transaction.

Sources

- AppsFlyer — App Retention Benchmarks — Cross-category retention benchmarks including finance-app D30 retention ranges

- NPCI — UPI Autopay Product Overview — Primary source on the UPI Autopay / e-mandate framework in India

- NPCI — UPI Autopay (recurring e-mandates) — UPI Autopay e-mandate framework: pre-debit notifications and per-transaction caps

- Braze — WhatsApp Business Platform — Channel research on WhatsApp open rates and lifecycle messaging

- MoEngage — App Retention Benchmark Report — India-focused retention and re-engagement benchmarks across verticals

- Amplitude — Retention Rate Analysis — Cohort retention curve methodology and benchmarks

- AppsFlyer — Remarketing & Re-engagement — Reference on the economics of re-engaging existing users versus acquisition

- NPCI — UPI Product Statistics — Transaction-volume context for the Indian recurring-payments base

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy