UPI Autopay for App Subscriptions: The India Playbook

Card-gated free trials structurally fail in India, where credit-card penetration is roughly 8%. This is how UPI Autopay e-mandates power recurring app subscriptions — the real ₹15,000 cap, the ₹1 lakh exception, and how to build an India subscription flow that actually converts.

Why do card-based free trials fail in the Indian market?

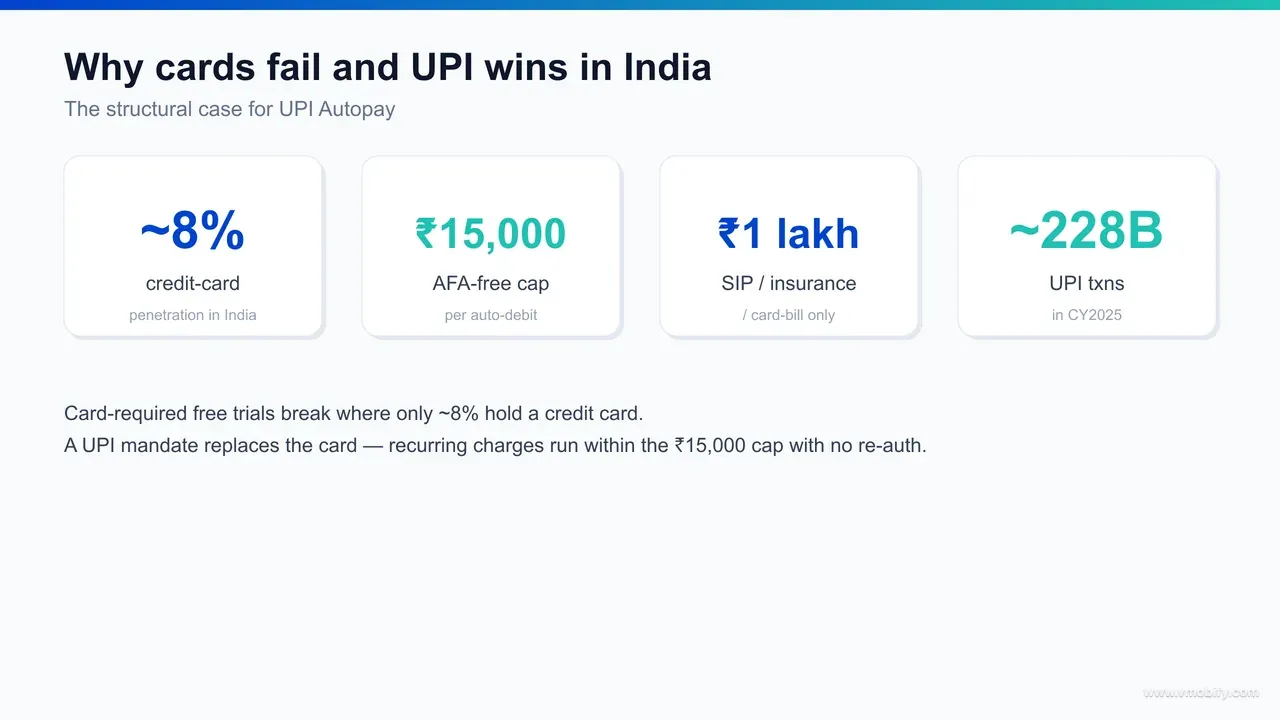

Card-gated free trials fail in India for a structural reason that no amount of paywall design can fix: only around 8% of Indians hold a credit card, so the majority of your addressable users cannot complete a checkout that demands one. The "add your card now, we'll charge you after the trial" pattern that works in the United States quietly excludes most of the Indian market before the user ever sees your product's value.

The numbers are stark. India's credit-card penetration sits at roughly 8%, far below the levels in mature subscription markets, per TransactBridge's analysis of why low card penetration is a barrier for global companies entering India. When your trial flow requires a card to start, you are not running a trial — you are running a filter that removes the bulk of your funnel at the worst possible moment.

It got harder, not easier, in 2021. The Reserve Bank of India's e-mandate framework took effect that October and broke the card-on-file auto-renewals that global subscription apps relied on — the disruption that briefly tripped up recurring billing for services like Netflix, Spotify and Prime in India, as ClearTax documented at the time. Cards in India are now both rare and operationally awkward for recurring charges.

Across our 300+ apps managed since 2013, the single most common India monetisation mistake we see is a globally designed paywall shipped unchanged into India: a card field, a 7-day countdown, and a conversion rate a fraction of what the same product earns elsewhere. The fix is not a better card form. It is to stop requiring a card at all and meet users on the rail they actually use.

What is UPI Autopay and how does it work for subscriptions?

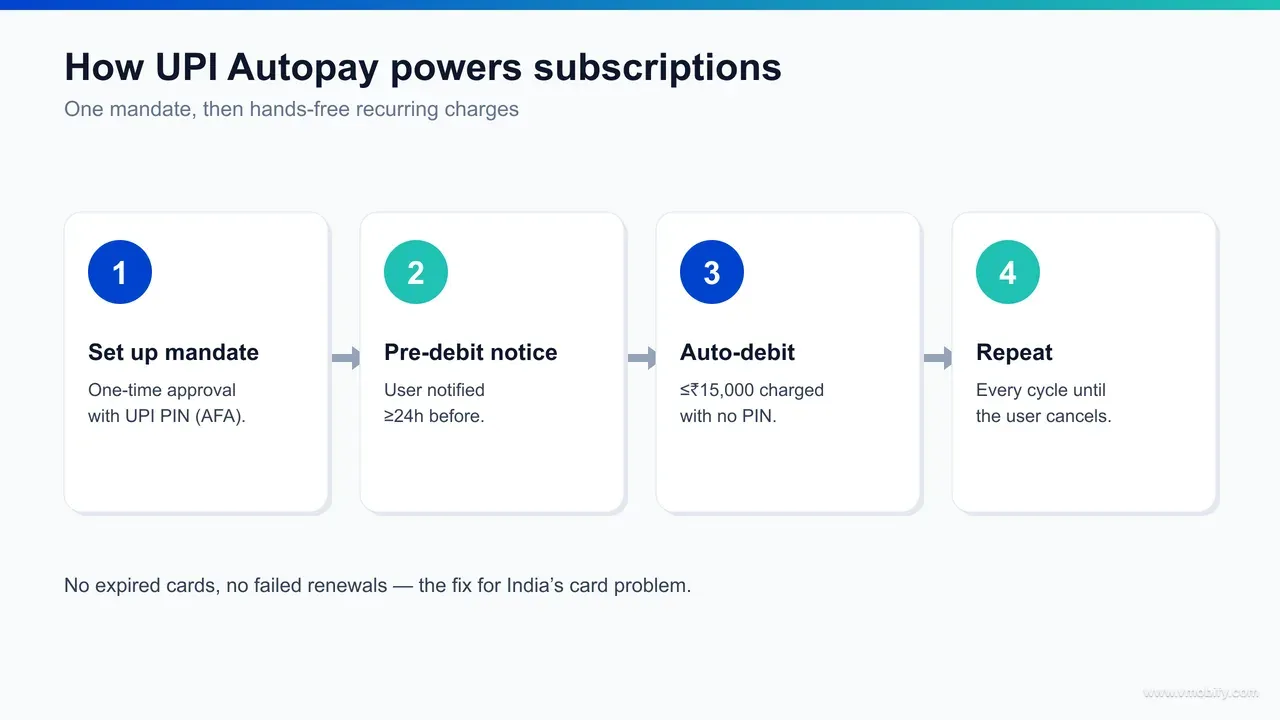

UPI Autopay is the National Payments Corporation of India's recurring-payments feature built on top of UPI: a user approves a one-time e-mandate from their UPI app, and from then on you can auto-debit their account on a set schedule without them re-authorising each charge. It is the India-native answer to the card-on-file subscription — but tied to a bank account the user already operates, not a card they probably do not own.

The mechanics are straightforward, and they map cleanly onto a subscription lifecycle:

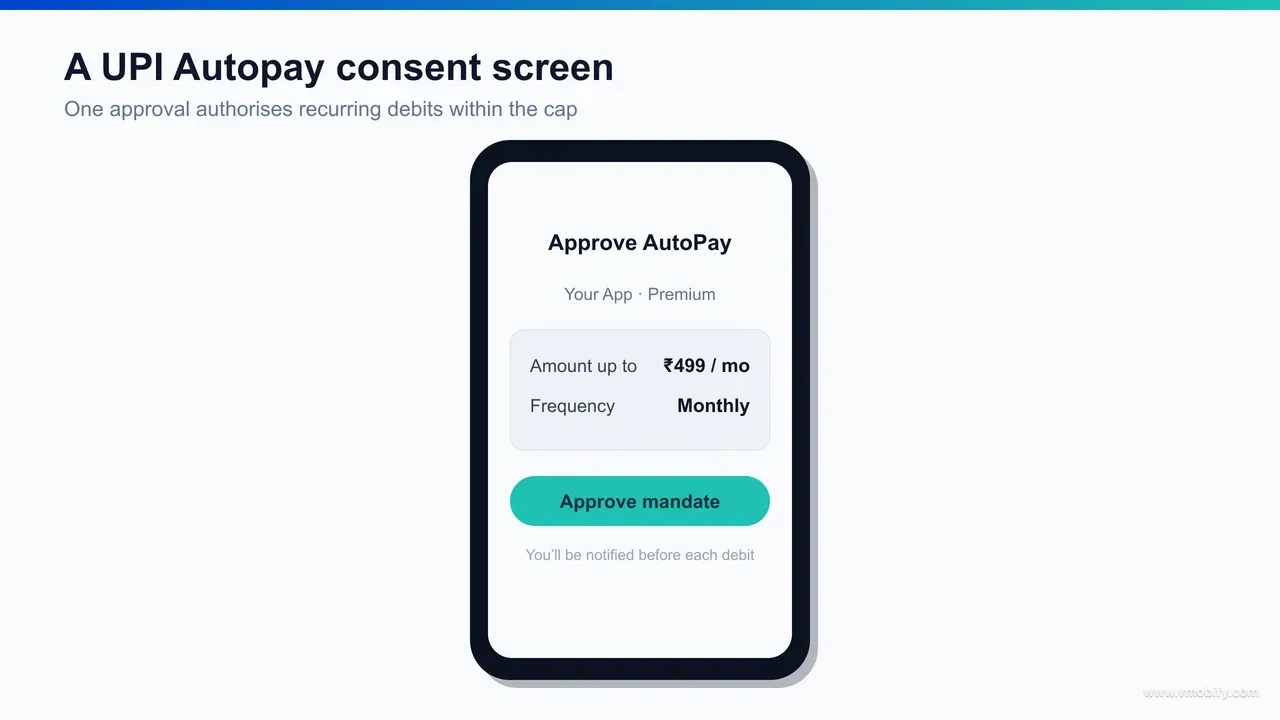

- Mandate setup: at checkout the user is shown the mandate terms — amount, frequency and validity — and approves it once inside their UPI app (PhonePe, Google Pay, Paytm and the rest) with their UPI PIN.

- Pre-debit notification: before each scheduled charge, the user receives a notification at least 24 hours in advance, so the renewal never arrives as a surprise. This is a regulatory requirement, per NPCI's UPI Autopay documentation.

- Auto-debit: on the due date the amount is debited automatically. Below the additional-factor-of-authentication threshold, no PIN re-entry is needed; above it, the user authenticates the charge.

The crucial difference from a card subscription is where the approval lives. A card mandate asks a user to trust you with card credentials they rarely use; a UPI mandate asks them to approve a recurring debit inside the bank-grade app they already open several times a day. The trust surface is one they understand, which is a meaningful conversion advantage at the moment of commitment. If you are thinking through the wider monetisation architecture this sits inside, our guide to app subscription monetisation strategy covers how trials, plans and renewals fit together.

What is the UPI Autopay limit without a PIN — and the ₹1 lakh exception?

For ordinary app subscriptions, UPI Autopay can auto-debit up to ₹15,000 per transaction without the user re-entering their UPI PIN; a separate ₹1 lakh limit exists but applies only to specific categories like mutual-fund SIPs, insurance premiums and credit-card bill payments — not general app subscriptions. Getting this distinction right matters, because conflating the two is the most common error in writing about UPI recurring payments.

Here is the history, exactly. When the RBI e-mandate framework on recurring transactions came into force in October 2021, the additional-factor-free (AFA-free) cap — the amount that can be auto-debited without a fresh authentication on each charge — was set at ₹5,000 per transaction. That cap was later raised to ₹15,000 per transaction, which is the figure that governs recurring app subscriptions today. Any single auto-debit at or below ₹15,000 goes through with no PIN re-entry; above it, the user must authenticate the individual charge.

The ₹1 lakh figure is a different rule for a different purpose. In December 2023 the RBI raised the per-transaction limit to ₹1 lakh specifically for mutual-fund subscriptions (SIPs), insurance premium payments and credit-card bill payments — a targeted exception for high-value, low-fraud-risk categories, as Business Standard reported. It is not a general uplift, and it does not apply to your streaming, productivity or content subscription. If you are building a normal app subscription, the number you design around is ₹15,000, not ₹1 lakh.

For practical purposes this ceiling is generous. A ₹15,000 per-transaction headroom comfortably covers virtually every consumer app subscription price point in India, where monthly plans typically run from under ₹100 to a few hundred rupees and even annual plans rarely approach the cap. The constraint almost never binds for a subscription business — but you should still surface the mandate amount honestly at setup, because the user is approving a recurring authorisation up to that figure. NPCI's own product documentation is the authoritative reference for the current operative limits, and we recommend confirming them there before you finalise your billing copy.

How big is UPI as a payments rail in 2026?

UPI is the largest real-time payments rail in the world, processing on the order of 228 billion transactions in CY2025 — which is the entire reason building on it is a distribution decision, not just a billing one. When you accept UPI mandates, you are not asking users to adopt a new payment method; you are accepting the one they already use for everything from groceries to rent.

The scale is hard to overstate. UPI handled roughly 228 billion transactions in CY2025, a figure the Press Information Bureau highlighted as part of UPI's position as the world's largest real-time payment system. For live, month-by-month volume and value, NPCI publishes its monthly UPI metrics, which is the source to check on any given publishing day rather than quoting a stale monthly number.

This ubiquity changes the psychology of a paywall. A user staring at a card field has to go find a card, type 16 digits, an expiry and a CVV, and trust your app with all of it. A user staring at a UPI mandate taps to approve inside an app they already trust and use daily. The friction delta is enormous, and it compounds in exactly the Tier-2 and Tier-3, vernacular-first segments where India's next 200 million subscribers live — the same audience profile we cover in our work on fintech app marketing in India.

The strategic point is simple: meet users where they pay. The international subscription playbook assumes the card is the default rail. In India it is not — UPI is — and a monetisation strategy that ignores that is leaving the majority of the market unaddressed regardless of how good the product or the paywall is.

How do you set up UPI Autopay for a subscription app?

Setting up UPI Autopay means integrating a payment provider that supports UPI recurring mandates, defining your mandate parameters, presenting the consent screen at checkout, and handling the mandate lifecycle — creation, pre-debit notification, execution, and revocation — in your billing logic. The integration shape is the same regardless of which gateway you choose; what differs is the surface area each provider exposes.

- Choose a provider that supports UPI Autopay mandates: most major Indian payment gateways and aggregators expose UPI recurring mandate APIs. Confirm the provider supports mandate creation, modification and revocation, plus webhook callbacks for the debit lifecycle — not just one-time UPI collect.

- Define the mandate: set the maximum amount (at or below ₹15,000 per transaction for an ordinary subscription), the frequency (monthly, annual, as-presented), the start and end dates, and the validity window. The mandate is an authorisation up to a ceiling, so set the maximum to cover your highest plan, not just the current price.

- Present the consent screen at checkout: show clear mandate terms and route the user into their UPI app to approve with their PIN. This is the conversion moment — keep the amount, frequency and what they are subscribing to unambiguous, because a confusing mandate screen is abandoned.

- Handle the lifecycle in your billing logic: ensure the at-least-24-hour pre-debit notification fires, listen for debit-success and debit-failure webhooks, manage retries and grace periods on failure, and support clean revocation when a user cancels. A renewal that fails silently is churn you could have recovered.

One implementation note worth flagging: because the mandate is an authorisation up to a maximum, you can debit any amount at or below it on each cycle, which gives you room for plan upgrades and proration without forcing a fresh mandate — provided the new charge stays under the approved ceiling. Set the maximum thoughtfully at setup and you avoid re-authorising users every time pricing changes. The end-to-end work — provider selection, mandate design, and renewal recovery — is exactly the kind of in-app monetisation build our team runs for India-focused apps.

How does UPI Autopay compare to card e-mandates?

UPI Autopay and card e-mandates run on the same RBI recurring-payments framework — including the additional-factor-free cap and the 24-hour pre-debit notice — but UPI wins decisively in India on reach, trust and setup friction, because it is tied to a bank account nearly everyone has rather than a card most do not. The rules are shared; the practical outcomes are not.

- Addressable base: a card e-mandate is only available to the roughly 8% of Indians with a credit card (and the card-on-file recurring flows the 2021 rules complicated). A UPI mandate is available to anyone with a bank account and a UPI app — effectively the whole smartphone-paying population.

- Setup friction: a card mandate requires entering full card details and a one-time authentication; a UPI mandate is a tap-to-approve inside the user's existing UPI app. Fewer fields, fewer drop-offs.

- Trust surface: users are wary of saving card credentials in apps but comfortable approving debits in their bank-grade UPI app, which they already use daily. The mandate lives where their trust already is.

- Shared guardrails: both run under the same e-mandate rules — the AFA-free per-transaction cap and the mandatory at-least-24-hour pre-debit notification apply to each, so the user protections are equivalent regardless of rail.

There are legitimate reasons to keep cards in the mix — international users, corporate cards, and the slice of premium users who do hold credit cards and prefer them. The right posture for an India-first app is not "UPI instead of cards" but "UPI as the default, cards as an option." Offer both; lead with UPI. Pricing the plans correctly for the market is the other half of this equation, which is why this pairs naturally with app price localisation by purchasing power — the rail and the price both have to fit India, not just one of them.

Which apps are winning India subscriptions with UPI Autopay?

The apps winning India subscriptions are the ones that made UPI Autopay the default path to a paid plan rather than a fallback — from streaming and content services to, more recently, global software products localising their billing for India. The pattern is consistent: when the recurring rail matches how Indians actually pay, trial-start and renewal rates rise.

A telling recent signal is that even AI products are building India billing on UPI. When OpenAI brought its lower-cost ChatGPT Go tier to India, it leaned on UPI-based billing to make the subscription accessible to a market where cards are scarce. When a company with global card-billing infrastructure chooses UPI specifically for India, it is a clear read on what converts here.

The category that proved the thesis first was streaming. The 2021 e-mandate disruption that broke card auto-renewals for the major OTT services forced a reckoning, and the durable answer was UPI Autopay — recurring billing on a rail that did not depend on card penetration. Content, fitness, education and utility subscriptions have followed the same route since, because they share the same constraint: a mass-market India audience that pays by UPI.

In our portfolio, the India-focused subscription apps that switched their default trial path from a card field to a UPI mandate consistently saw more trials actually start — the card requirement had been silently capping the top of the funnel. The product did not change; the rail did. That is the recurring lesson: in India, the payment method is not a checkout detail, it is a growth lever.

How do you design an India subscription flow that converts?

An India subscription flow that converts leads with UPI Autopay, prices for the market, makes the mandate terms unmistakably clear, and treats the 24-hour pre-debit notice as a retention touchpoint rather than a compliance chore. The mechanics above are necessary; this is how you turn them into conversion and retained revenue.

- Make UPI the default, not an option buried under a card field: the first payment method a user sees should be the one they actually use. Cards can remain available for the minority who want them, but UPI Autopay should be the obvious, pre-selected path.

- Set the mandate maximum to cover your real range: approve a ceiling that comfortably covers your highest plan (well within ₹15,000), so upgrades and proration do not force a fresh mandate. Do not approve a mandate far above what the user will ever be charged, though — an honest, proportionate ceiling builds trust at the consent screen.

- Write the consent screen for clarity: amount, frequency, what they get, and how to cancel — in plain language, and ideally in the user's language for a vernacular audience. Confusion at the mandate screen is abandoned subscriptions.

- Use the pre-debit notice as a moment, not a nuisance: the mandatory 24-hour notification is a chance to remind the user of the value they are about to pay for — and to recover a save if they were about to churn. Pair it with smart failure-retry and grace-period logic so an involuntary failure does not become an involuntary cancellation.

Two failure modes are worth calling out explicitly because they quietly cost the most revenue. The first is conflating the caps — designing or marketing around ₹1 lakh when ordinary subscriptions live under the ₹15,000 rule — which leads to incorrect mandate ceilings and confused billing copy. The second is treating UPI as a checkout afterthought bolted onto a globally designed paywall, rather than the centre of an India-first flow; the card-first paywall with UPI tucked away underneath still leaks most of the funnel.

If you want this built and measured properly for your app — provider selection, mandate design, renewal recovery, and a paywall priced and localised for India rather than copied from a global template — that is exactly the India growth work our team runs. You can see the outcomes across our team's case work and get in touch directly. In India, the recurring rail is not a billing decision you make once and forget; it is one of the highest-impact growth choices a subscription app makes.

Frequently Asked Questions

What is the UPI Autopay limit without a PIN?+

For ordinary app subscriptions, UPI Autopay auto-debits up to ₹15,000 per transaction without the user re-entering their UPI PIN. Above that amount, the user must authenticate each individual charge. The cap was ₹5,000 when the e-mandate rules took effect in October 2021 and was later raised to ₹15,000.

How does UPI Autopay work for subscriptions?+

The user approves a one-time e-mandate inside their UPI app, specifying the amount, frequency and validity. After that, charges auto-debit on schedule, with a pre-debit notification sent at least 24 hours before each one, and no PIN re-entry needed for amounts at or below the AFA-free cap.

Why do card-based free trials fail in India?+

Credit-card penetration in India is only around 8%, so a trial that requires a card to start excludes most of your addressable users. The 2021 RBI e-mandate rules also disrupted card-on-file auto-renewals, making cards both rare and operationally awkward for recurring billing.

What is the ₹1 lakh UPI Autopay limit for?+

The ₹1 lakh per-transaction limit, raised in December 2023, applies only to specific categories — mutual-fund SIPs, insurance premium payments and credit-card bill payments. It does not apply to general app subscriptions, which are governed by the ₹15,000 cap.

How does UPI Autopay compare to card e-mandates?+

Both run under the same RBI recurring-payments framework, including the AFA-free cap and the 24-hour pre-debit notice. UPI wins in India on reach (a bank account nearly everyone has versus cards most do not), lower setup friction, and a trust surface users already use daily.

Do users get notified before an auto-debit?+

Yes. A pre-debit notification must reach the user at least 24 hours before every scheduled auto-debit, so renewals are transparent by regulation. This is also a useful retention touchpoint to remind users of the value they are paying for.

How big is UPI as a payments rail in 2026?+

UPI is the largest real-time payments system in the world, processing on the order of 228 billion transactions in CY2025. For ordinary subscription price points in India, building on UPI means meeting users on the rail they already use daily.

Sources

- NPCI — UPI Autopay product page — How UPI Autopay e-mandates work, including the pre-debit notification requirement

- NPCI — Monthly UPI metrics — Live month-by-month UPI transaction volume and value

- PIB — UPI as the world's largest real-time payment system — UPI scale and ~228 billion transactions in CY2025

- Business Standard — UPI Autopay limit raised to ₹1 lakh — The ₹1 lakh cap for SIPs, insurance and credit-card bills (Dec 2023)

- ClearTax — How the 2021 RBI e-mandate rules changed recurring billing — The October 2021 e-mandate disruption to card auto-renewals

- TransactBridge — India's low card penetration as a barrier — India credit-card penetration around 8%

- i10x — ChatGPT Go India strategy and UPI billing — A global software product launching UPI-based subscription billing in India

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy