B2B Lending App Case Study: Cost-Per-Funded-Loan Down 38%

A digital lending app for small and medium businesses was paying a fortune to acquire borrowers — and most of them never finished the application. Install-to-application sat at 14% and application-start-to-submitted at just 31%, so the blended cost-per-funded-loan was unsustainable. Over six months we rebuilt the loan-application funnel, fixed the document-upload and KYC drop-off, launched a WhatsApp win-back for abandoned applications, and re-pointed every rupee of media at the funded-loan event. Cost-per-funded-loan fell ~38%. Here is the full playbook.

What was the brief and the starting position?

A digital lending app for small and medium businesses came to us with a painful, specific problem: it was paying a great deal to acquire business borrowers, but almost none of them ever finished the loan application — so the cost of every loan it actually funded had become unsustainable. The install numbers looked respectable. The funded-loan numbers did not. Between those two figures sat a leaking application funnel that no amount of extra media spend could fix.

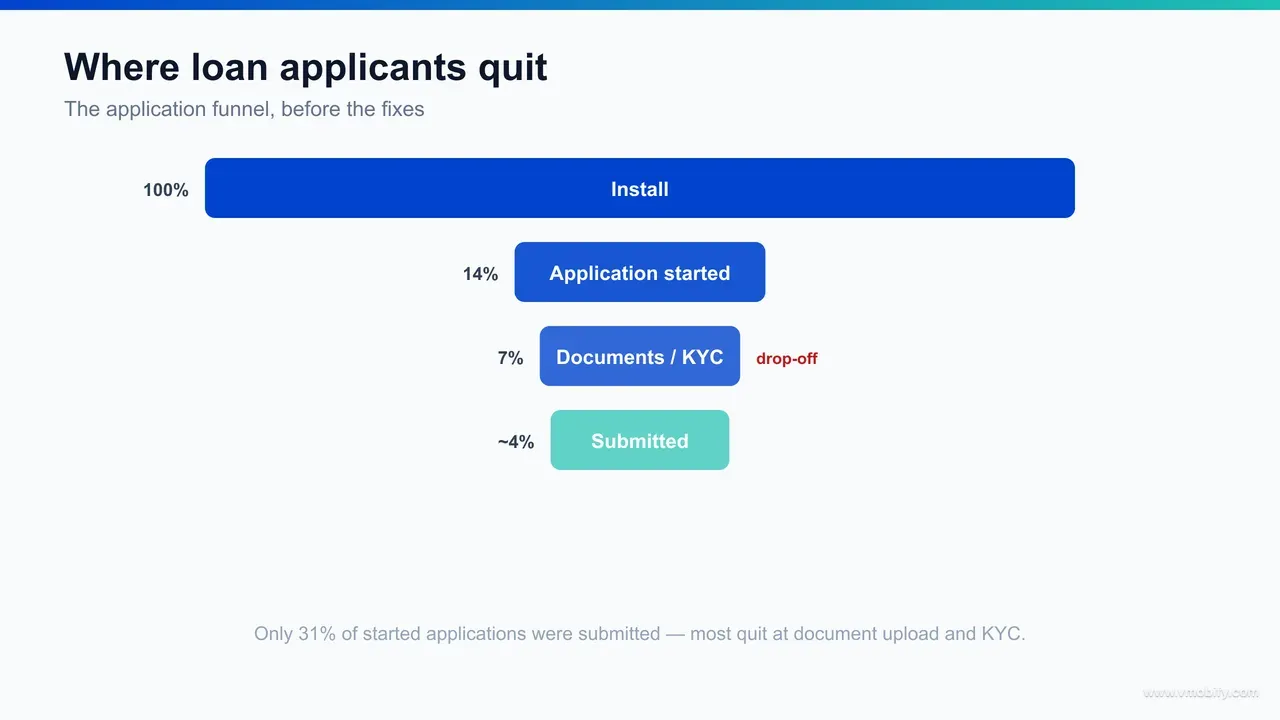

The starting position, measured honestly, was sobering. Only 14% of installs ever started a loan application — the other 86% downloaded the app, looked around, and left without entering the funnel at all. Of the minority who did start, just 31% reached a submitted application. Most of that loss was concentrated in one stretch: the document-upload, bank-statement, and KYC steps, where business owners hit friction, lost patience, or simply did not have the paperwork to hand and never came back.

Stack those two conversion rates and the maths is brutal. Out of every 100 installs, 14 started an application and roughly four submitted one — before underwriting, before approval, before a single rupee was disbursed. With a regulated lending product carrying a high cost-per-qualified-lead to begin with, the blended cost-per-funded-loan that fell out of this funnel was not a number the business could scale on.

The brief was therefore not "get us more installs". It was "make the money we already spend produce funded loans". Two levers were on the table from day one: fix the funnel so a far larger share of acquired borrowers reached a funded loan, and fix the acquisition so the borrowers we paid for were the kind who could actually qualify. We worked both at once. Across our 300+ apps managed since 2013, we have learned that in regulated fintech you almost never fix lending-app economics from the media side alone — the funnel and the targeting have to move together.

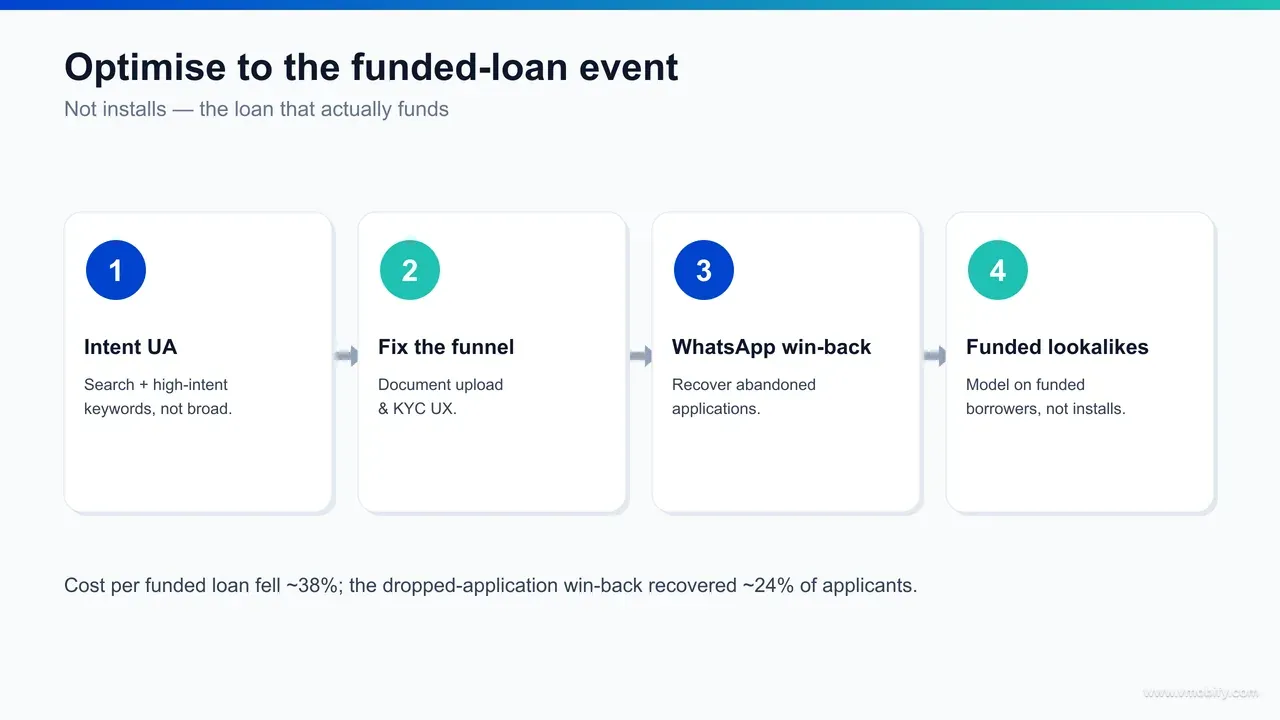

This case study documents exactly how that happened over roughly six months: how we instrumented the application funnel to find the true drop-off, how we rebuilt the document and KYC experience, how a WhatsApp win-back recovered abandoned applications, how intent-targeted UA and ASO lowered the cost-per-lead, how lookalikes on funded borrowers raised quality, and how re-pointing the whole machine at the funded-loan event took cost-per-funded-loan down roughly 38%.

Why must a lending app optimise to the funded-loan event, not installs?

In lending, the install is almost meaningless — the only event that carries revenue is the funded loan, and any acquisition system that optimises toward installs will reliably buy the wrong borrowers at an attractive-looking cost while the real cost-per-funded-loan quietly stays unsustainable. A funded loan in an SME product sits five or six steps deep: install, application-start, document upload, bank-statement and KYC, submission, underwriting approval, and disbursal. Optimising to the first of those steps optimises against the last.

The mechanism is straightforward and it traps a lot of fintech teams. When you tell an ad platform to find people who install, it gets very good at finding cheap installers — users who download readily but have weak intent, thin credit profiles, or no genuine borrowing need. Install cost looks great on the dashboard. Then those users never start an application, or start one and abandon it, and the handful who reach a funded loan have to carry the acquisition cost of everyone who did not. AppsFlyer's performance benchmarks consistently show how widely install quality varies by channel and optimisation event — a gap that is invisible until you measure to the deepest event.

Regulation widens the gap further. India's lending rules — the RBI's digital-lending framework — require genuine KYC, income or bank-statement verification, and consent at each step. That is correct and necessary, but it means a borrower cannot be "converted" with a slick screen the way a low-friction e-commerce checkout can. Every weak-intent install you buy will hit a verification wall it was never going to clear, so paying to acquire it is pure waste.

The fix is to make the funded loan — or its closest reliable proxy, the qualified submission — the event the entire acquisition system points at. When the platform learns toward users who actually submit and fund, it starts finding business owners with real borrowing intent and the documents to back it, even if their install cost is higher. The blended cost-per-funded-loan is what falls, because the denominator finally fills with borrowers who convert. We unpack the deeper ROAS-and-CAC logic behind this in our app ROAS and CAC guide; for this client it was the founding principle of the rebuild.

How did we instrument the full loan-application funnel?

Before we changed a single screen or a single campaign, we instrumented every step of the loan-application funnel as a discrete, named event — because you cannot fix a drop-off you cannot see, and the client had been flying with install and "loan disbursed" wired up but almost nothing in between. The middle of the funnel, where all the money was leaking, was a black box.

We rebuilt the event taxonomy end to end so that every meaningful transition fired its own event back to the measurement stack:

- install → application-start: the moment a borrower taps into the loan flow and enters the first field, separating genuine entrants from the large majority who never started.

- application-start → documents-begin: reaching the document-upload step at all, which exposed how many quit before even attempting paperwork.

- documents → bank-statement → KYC: each verification sub-step fired separately, so we could see precisely which one shed the most applicants rather than treating "verification" as one opaque block.

- KYC → submitted: a completed, submitted application ready for underwriting.

- submitted → approved → funded: the underwriting and disbursal outcomes that define a funded loan and its true acquisition cost.

We wired this through the attribution and analytics layer so each event could be passed back to the ad platforms as an optimisation signal later. Getting this right is not glamorous, but a mis-fired or duplicated event silently wastes the entire media budget — the platform optimises toward a phantom. Tools like Adjust and AppsFlyer make this measurable, but only if the in-app events are defined cleanly first. Our mobile app funnel analytics approach treats this instrumentation as the precondition for any optimisation work, not an afterthought.

The instrumented funnel told the story immediately. Of every 100 installs, 14 started an application; of those 14, only about four submitted; and within that start-to-submit collapse, the single heaviest loss sat at the document-upload, bank-statement, and KYC stretch — 69% of applicants who started quit before submitting. That one number reframed the whole engagement. The problem was not primarily a traffic problem. It was a funnel problem with a traffic problem stacked on top, and the funnel was the cheaper and faster of the two to fix first.

How did we fix the document-upload and KYC drop-off?

The biggest single win came from rebuilding the document-upload, bank-statement, and KYC experience — the stretch where most applicants were quitting — and it lifted application-start-to-submitted from 31% to 53% without loosening a single compliance requirement. The goal was never to remove verification; in regulated lending you cannot and should not. The goal was to remove every gram of friction that was not the verification itself.

We instrumented the sub-steps, watched real session recordings, and attacked the failure points in order of how many applicants each one cost:

- Telling borrowers what they need up front: business owners were arriving at document upload with no warning and no PAN, GST, or bank statement to hand. We added a clear, early "here is exactly what you will need" checklist so applicants could gather documents before entering the flow — and could leave and return to the same point without losing progress.

- Save-and-resume, not start-over: previously, abandoning the flow meant re-entering everything. We made the application stateful so a borrower interrupted by a customer or a meeting could resume exactly where they left off, which alone recovered a meaningful slice of mid-funnel drop-off.

- Bank-statement friction: the manual statement upload was a common quit point. We streamlined the accepted formats, added clear inline guidance on what a valid statement looked like, and reduced re-upload loops caused by unclear error states.

- KYC error states: a large share of KYC abandonment was not refusal — it was confusion. Opaque failure messages ("verification failed") were rewritten to tell the borrower exactly what went wrong and how to fix it, turning dead ends into recoverable steps.

- Progress and reassurance: a visible step indicator and short reassurance on data handling reduced the anxiety that makes people abandon a money application midway.

None of these touched the underwriting bar. Every borrower still had to clear the same KYC and verification standard required by the RBI digital-lending norms. What changed was that the borrowers who could clear that bar were no longer dropping out for reasons that had nothing to do with their eligibility. In our portfolio, fintech funnel work like this is almost always the highest-ROI lever available, because it improves every downstream cohort at once — paid, organic, and win-back traffic all convert better through a funnel that no longer leaks.

How did the WhatsApp win-back recover abandoned applications?

We built a WhatsApp-based win-back that re-engaged borrowers who had started an application and abandoned it — and it recovered roughly 24% of dropped applications, at a fraction of the cost of acquiring a fresh borrower. An abandoned application is the single most valuable re-engagement audience a lending app has: the person has already shown intent, already entered the funnel, and already cleared the hardest hurdle, which is deciding to apply at all. Walking away from that audience is walking away from money already paid for.

WhatsApp was the right channel for the Indian SME borrower specifically. Business owners live in WhatsApp, open rates dwarf email, and a conversational nudge feels closer to how they already do business than a push notification or a cold call. The win-back ran on a few disciplined principles:

- Trigger on the exact drop-off step: the message referenced where the borrower stopped — "you were one step from submitting; you just need your last bank statement" — because a specific, helpful nudge converts far better than a generic "come back".

- Solve the reason they quit, not just remind: if they stalled at document upload, the message told them precisely which document was outstanding and that they could resume without re-entering anything, leaning directly on the save-and-resume work from the funnel rebuild.

- Timing windows that matched intent: the first nudge went out while intent was still warm, with a short follow-up sequence — not an endless drip that would feel like harassment on a money product.

- Consent and compliance: messaging ran on opted-in templates within WhatsApp Business policy and the consent the borrower had already given, which matters doubly in regulated lending.

The compounding effect was significant. Recovering ~24% of abandoned applications meant a quarter of the funnel's biggest leak was being recaptured at near-zero marginal acquisition cost — these borrowers had already been paid for once. Stacked on top of the funnel fixes, the win-back turned the document-and-KYC stretch from the funnel's worst section into one of its more recoverable ones. The diagram below shows where applicants were dropping and where the win-back intercepted them.

How did intent-targeted UA and ASO lower the cost-per-lead?

We replaced the old broad install campaigns with intent-targeted user acquisition — search and high-intent keywords — and a focused ASO programme on the terms business owners actually type, and together they cut blended cost-per-qualified-lead by roughly 35%. The previous approach had been buying volume: broad app-install campaigns optimised to the install, which is exactly the trap the second section of this case study describes. The borrowers it bought were cheap and rarely qualified.

The intent-led rebuild concentrated spend where genuine borrowing demand already exists:

- Search and high-intent keywords: a business owner searching "business loan", "working capital loan", or "MSME loan" is mid-funnel by definition — they have a need and are looking for a lender. Pointing acquisition at that moment of intent, via Google App Campaigns fed with high-intent search signals and tight keyword themes, brought in borrowers materially more likely to start and submit an application than broad-audience installers.

- ASO for the borrowing vocabulary: we re-architected the store listing to index for the full semantic field of SME borrowing — "business loan", "working capital", "MSME loan", "loan for shop", "GST business loan" and the long tail around them — so organic discovery captured high-intent searchers the app had been invisible to. Every organic install from these terms arrived pre-qualified by intent and cost nothing in media.

- Listing conversion to match the intent: the screenshots and short description led with the borrowing job-to-be-done — fast working-capital, clear eligibility, transparent terms — so the high-intent traffic the keywords delivered actually converted to installs rather than bouncing.

- Geographic and segment focus: spend concentrated where the qualifying borrower density was highest rather than spraying nationally, keeping cost-per-qualified-lead down by not paying to reach segments that rarely funded.

The result was a different kind of traffic, not just cheaper traffic. Blended cost-per-qualified-lead fell about 35%, and — more importantly — the leads were borrowers who progressed through the now-rebuilt funnel rather than stalling at the first verification wall. Our user acquisition and app store optimisation teams run intent-led UA and ASO as one system for precisely this reason: in a high-intent category like lending, who you bring in determines how the entire funnel below performs.

How did lookalikes on funded borrowers improve borrower quality?

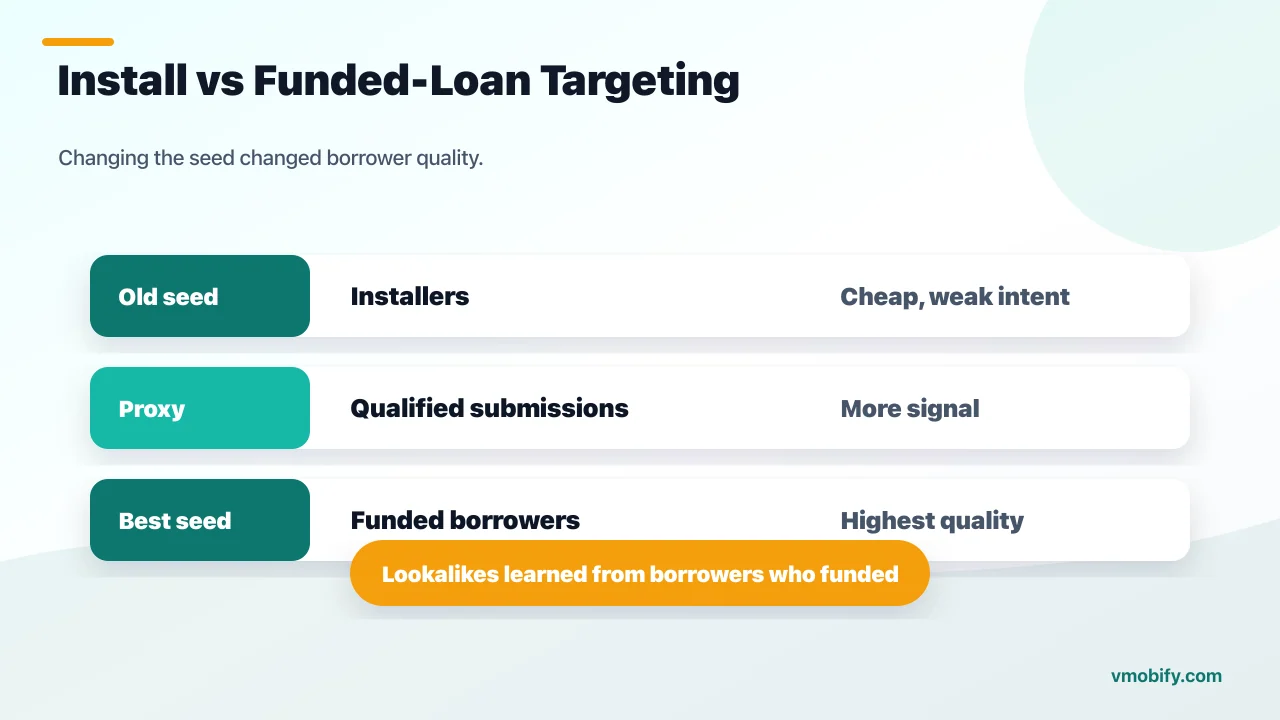

The quality lever that mattered most was building lookalike audiences on funded borrowers — the people who had actually qualified and taken a loan — rather than on installers, which is what the account had been doing by default. A lookalike audience is only ever as good as the seed it learns from, and seeding on installs teaches the platform to find more installers. Seeding on funded borrowers teaches it to find more borrowers who fund. That distinction is the whole game.

The mechanism is intuitive once you see it. The old broad campaigns, optimised to installs, effectively told the ad platforms: "find me more people like the ones who downloaded the app." But the people who downloaded the app were overwhelmingly the ones who never applied — so the lookalike compounded the original problem, scaling up the exact low-intent profile that was clogging the top of the funnel. We inverted it:

- Seed on funded loans, not installs: once enough funded-loan events were flowing back through the rebuilt event taxonomy, we used that cohort as the lookalike seed. The platform began finding business owners who resembled real, qualified, funded borrowers — by behaviour, segment, and profile.

- Layered seeds for volume and quality: where the funded-loan cohort was too small to scale alone early on, we used qualified-submission as an intermediate, higher-volume seed that still sat far deeper than install — then tightened toward funded as data accumulated.

- Exclusions that protected the seed: we suppressed existing borrowers and known low-quality segments so the lookalike kept learning from clean signal rather than re-targeting people who would never qualify.

- Continuous reseeding: as the funded cohort grew, we refreshed the seed so the audience tracked the borrowers who were actually converting under the new funnel, not a stale snapshot.

The effect showed up as a rising share of acquired users who qualified and funded — quality, not volume, was what moved. This is a pattern we see across fintech accounts in our portfolio: the lookalike seed is one of the highest-impact and most-overlooked settings in the entire media stack. Get the seed wrong and you scale your worst cohort efficiently. Get it right and the platform does your borrower-qualification work for you. We go deeper on this in our fintech app marketing guide for India.

How did aligning spend to the funded-loan event change the economics?

The change that tied everything together was aligning paid spend to the funded-loan event itself — feeding funded loans (and qualified submissions as a proxy) back into the ad platforms as the optimisation signal, so the algorithms learned toward borrowers who fund instead of users who install. The funnel fixes, the win-back, the intent UA, and the lookalikes were each necessary; this is what compounded them into a 38% cost-per-funded-loan reduction.

Once the event taxonomy was firing reliably and funded volume was sufficient for the platforms to learn, we shifted optimisation down the funnel in deliberate stages:

- From install to qualified-submission: the first step away from install-optimisation. Submission is far closer to revenue than install, fired at enough daily volume to train on early, and immediately pulled acquisition toward borrowers who completed the application rather than ones who bounced.

- From submission to funded-loan: as funded volume grew, we moved the core campaigns onto the funded-loan event — or value-based bidding on loan value where the data supported it — so the platforms optimised toward the borrowers who actually disbursed, the only event with revenue attached.

- Budget reallocation by true cost: with cost measured at the funded-loan rather than the install, channels and campaigns re-ranked. Sources that looked cheap on install cost but produced no funded loans were cut; sources with higher install cost but strong funded-loan economics were scaled.

- One scoreboard for the whole team: media, product, and funnel work were all judged against cost-per-funded-loan, so no one could "win" by lowering install cost while quietly raising the real cost of a loan.

This is the difference between optimising toward money and optimising toward vanity. An install-optimised account can show a falling install cost while the cost-per-funded-loan rises — and the business slowly bleeds. A funded-loan-optimised account ties every rupee of spend to the event that pays for it. The flow below shows how the funded-loan signal feeds back into acquisition; once that loop closed, the blended cost-per-funded-loan fell month over month even as volume held. It is the same discipline behind our ROAS and CAC framework: measure to the deepest event, and let everything upstream reorganise around it.

What were the final results across the funnel and CAC?

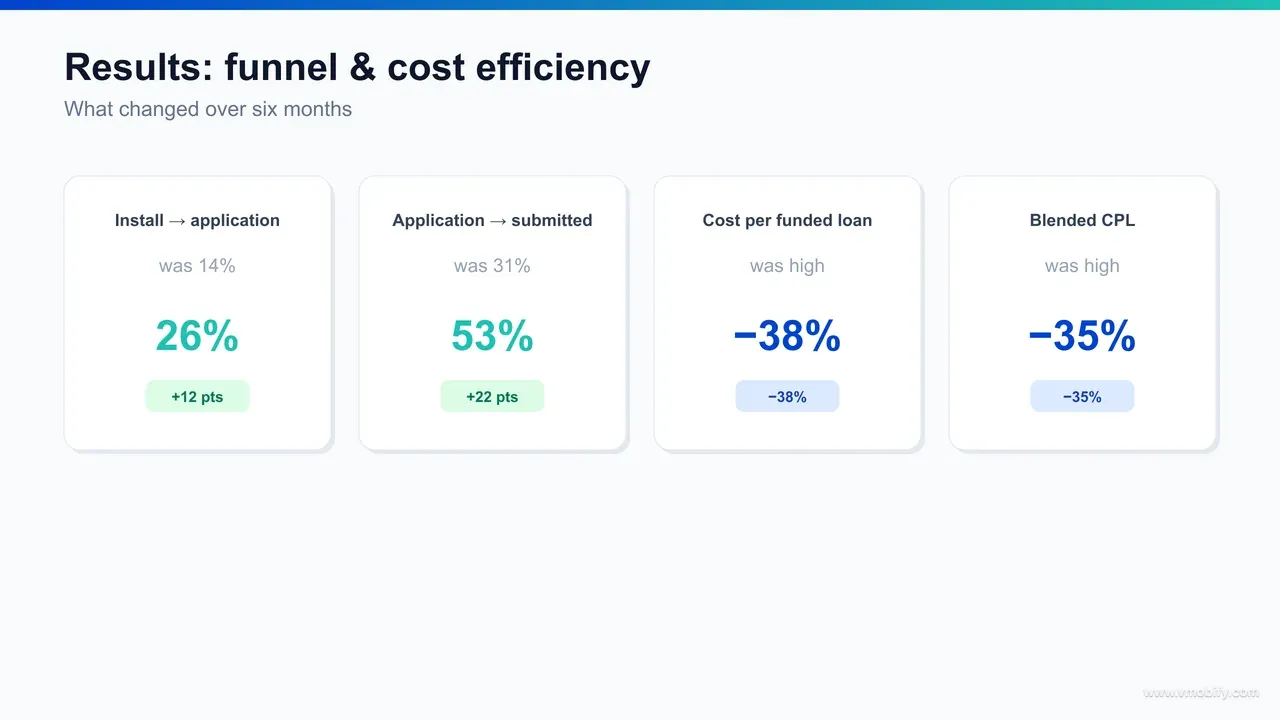

Over roughly six months, install-to-application-start went from 14% to 26%, application-start-to-submitted from 31% to 53%, the WhatsApp win-back recovered ~24% of abandoned applications, intent UA and ASO cut blended cost-per-qualified-lead ~35%, and the combined effect took cost-per-funded-loan down approximately 38%. The consolidated numbers:

- Install to application-start: 14% to 26% — nearly double the share of installs that enter the loan funnel at all.

- Application-start to submitted: 31% to 53% — the document, bank-statement, and KYC rebuild doing most of the lifting.

- Document-and-KYC drop-off: from a 69% start-to-submit drop-off to 47%, most of it at that stretch — the funnel's worst section, materially recovered.

- Abandoned-application recovery: ~24% of dropped applications won back through the WhatsApp win-back, at near-zero marginal acquisition cost.

- Blended cost-per-qualified-lead: down ~35% via intent-targeted UA, high-intent search, and ASO for the SME-borrowing keyword set.

- Cost-per-funded-loan: down ~38% — the headline business outcome, and the metric the whole engagement was built to move.

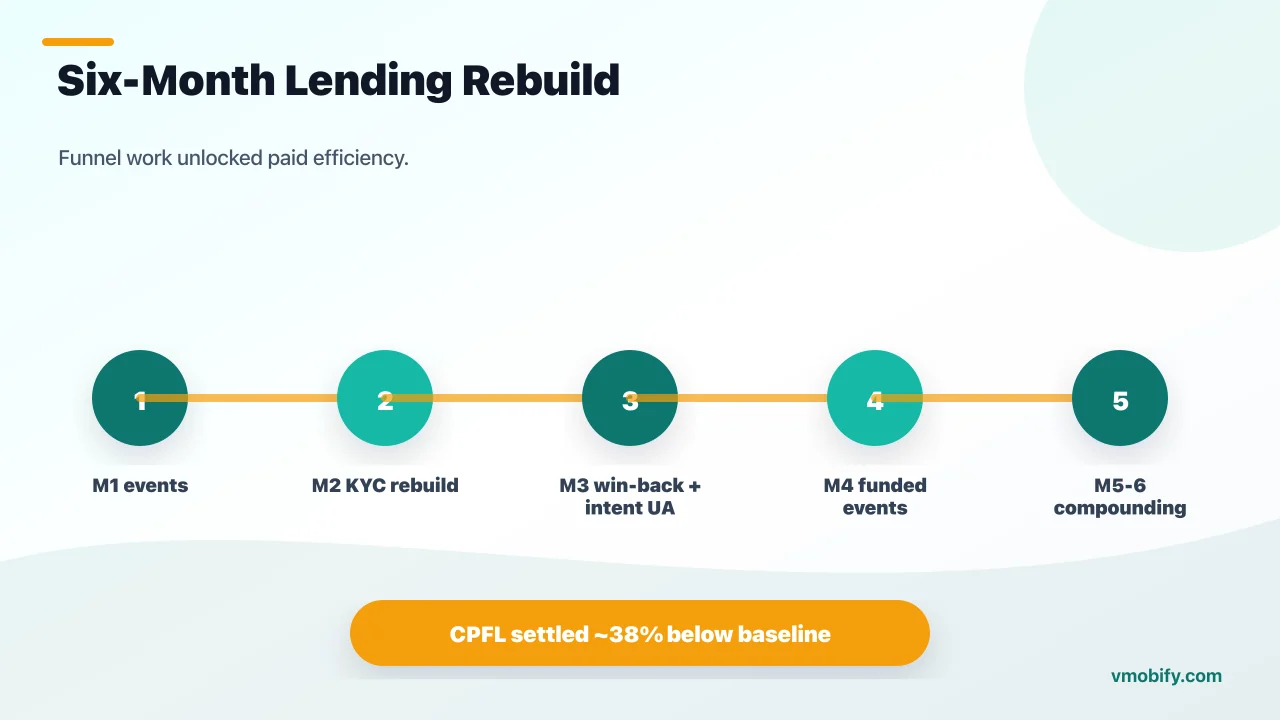

The shape of the six months mattered as much as the endpoint:

- Month 1: full funnel instrumentation. Every application step wired as a discrete event and verified end to end. The document-and-KYC stretch identified as the primary leak within the 69% start-to-submit drop-off.

- Month 2: the document, bank-statement, and KYC rebuild ships — checklist, save-and-resume, clearer error states. Application-start-to-submitted begins climbing.

- Month 3: WhatsApp win-back goes live against abandoned applications; intent-targeted UA and ASO replace broad install campaigns. Cost-per-qualified-lead starts falling.

- Month 4: the inflection. Funded-loan events flow back into the platforms; optimisation shifts from install to submission and toward funded. Lookalikes reseed on funded borrowers.

- Month 5-6: compounding. Funnel gains, win-back recovery, intent traffic, and funded-loan optimisation reinforce one another. Cost-per-funded-loan settles ~38% below the baseline at held volume.

Two lessons future fintech teams should internalise. First, the economics of a lending app are won in the funnel and at the funded-loan event, never at the install — the single biggest gain here came from making more of the borrowers you already paid for reach a funded loan. Second, the levers compound — a fixed funnel makes the win-back convert better, intent traffic makes the funnel convert better, and funded-loan optimisation makes the whole system buy better borrowers. You can see the same systems thinking across our portfolio of case studies.

What makes this lending-app playbook repeatable?

This playbook is repeatable across lending and regulated-fintech apps because it is a system, not a set of tactics — the loan product, the keyword set, and the verification steps change between clients, but the structure that took cost-per-funded-loan down 38% does not. The repeatable spine has five parts, in order.

- Instrument to the deepest event first: wire every step from install to funded loan as a discrete event before changing anything. You cannot optimise what you cannot see, and the middle of a lending funnel is where the money leaks. This is the non-negotiable precondition.

- Fix the funnel before you scale the spend: a leaking funnel makes every acquired borrower more expensive. Fixing the document-and-KYC drop-off improved paid, organic, and win-back cohorts simultaneously — the highest-ROI work available, and it is almost always cheaper than buying your way around the leak.

- Recover the intent you already paid for: abandoned applications are the most valuable re-engagement audience a lender has. A channel-appropriate win-back — WhatsApp for the Indian SME borrower — recovers them at a fraction of fresh acquisition cost.

- Acquire on intent, seed on funded borrowers: intent-targeted UA and ASO bring in borrowers with real need; lookalikes seeded on funded loans, not installs, scale the right profile. Who you bring in determines how the whole funnel performs.

- Point every rupee at the funded-loan event: hold media, product, and funnel to one scoreboard — cost-per-funded-loan — so cheaper installs never disguise a more expensive loan.

Each part reinforces the others, which is why the result is a system rather than a stack of disconnected wins. The flow below shows the closed loop: acquire on intent, convert through a fixed funnel, recover abandons, feed funded loans back into the platforms, and reseed the lookalike on the borrowers who funded. Run that loop and the blended cost-per-funded-loan keeps falling.

Who ran this, and how would it map to your app?

Vmobify has managed app marketing for Indian and global publishers since 2013, across 300+ apps in fintech, gaming, OTT, edtech, news, and utility — and the reason this lending playbook transfers is that we treat funnel, product analytics, and media as one system rather than three separate budgets. In regulated fintech especially, you cannot fix the economics from the media side alone, and we do not try to.

- We optimise toward money, not vanity: every campaign points at the deepest meaningful event — here, the funded loan. Optimising to installs is how agencies produce big, cheap, useless numbers; optimising to funded loans is how you build a lending business. That discipline anchors our user acquisition practice.

- Funnel and acquisition move together: we instrument the full application funnel, fix the drop-offs, and only then scale spend — because a fixed funnel makes every acquired borrower cheaper across every channel at once.

- India is our home market: the team works out of India, understands the SME borrower, the WhatsApp-first communication habit, and the regulatory frame around lending and KYC — context international agencies spend their first quarter relearning.

- ASO and paid UA are one system: we run app store optimisation and paid acquisition together, so intent-led organic and intent-led paid reinforce each other rather than competing for the same borrower at two different costs.

- The portfolio compounds: funnel-optimisation muscle built on one fintech app transfers to the next, and lending learnings cross-pollinate with payments, broking, and insurance work across the portfolio.

If you are scaling a lending, payments, or broking app in India — and you are paying too much for borrowers who never finish the application — this playbook adapts to your product. The loan type, the keyword set, and the verification steps change; the instrument-fix-recover-acquire-optimise structure does not. Talk to Vmobify's growth team to see how it would map to your funnel, or read our fintech app marketing guide for India for the broader strategy behind it.

Frequently Asked Questions

What was the headline result of this lending-app case study?+

Cost-per-funded-loan fell roughly 38% over about six months. That came from fixing the loan-application funnel (install-to-application 14% to 26%, application-start-to-submitted 31% to 53%), a WhatsApp win-back that recovered ~24% of abandoned applications, intent-led UA and ASO that cut blended cost-per-qualified-lead ~35%, and re-pointing all paid spend at the funded-loan event instead of the install.

Why is optimising to installs so dangerous for a lending app?+

In lending the install carries no revenue — a funded loan sits five or six verification steps deeper. Optimising to installs trains the ad platforms to find cheap installers with weak intent who never pass KYC, so install cost looks great while the real cost-per-funded-loan stays unsustainable. The fix is to optimise toward the funded loan, or a qualified-submission proxy, so the platform finds borrowers who actually fund.

How did fixing the document-upload and KYC steps lift conversion so much?+

Most of the document-and-KYC abandonment was friction, not ineligibility. Telling borrowers up front exactly what they would need, adding save-and-resume so an interrupted application was not lost, streamlining bank-statement upload, and rewriting confusing KYC error messages lifted application-start-to-submitted from 31% to 53% — without loosening any compliance requirement.

Why use WhatsApp for the abandoned-application win-back?+

Indian SME business owners live in WhatsApp — open rates dwarf email and a conversational nudge fits how they already do business. Triggering on the exact drop-off step, solving the specific reason they quit, and using opted-in templates recovered roughly 24% of abandoned applications at a fraction of fresh acquisition cost, since those borrowers had already been paid for once.

What does seeding lookalikes on funded borrowers actually change?+

A lookalike is only as good as its seed. Seeding on installs teaches the platform to find more installers — the low-intent profile clogging the funnel. Seeding on funded borrowers teaches it to find more people who resemble real, qualified, funded borrowers, which raised the share of acquired users who qualified and funded. Quality, not volume, was the lever that moved the economics.

Can this playbook work for a payments, broking, or insurance app instead of lending?+

Yes, with adaptations. The product, the keyword set, and the verification steps change, and the north-star event changes — a funded loan becomes a funded account, a first trade, or a policy purchase. The structure stays the same: instrument the full funnel, fix the drop-offs, recover abandons, acquire on intent, and optimise every rupee toward the deepest revenue event.

How long did the results take, and do they hold without continuous spend?+

The full effect landed over roughly six months, with the inflection around month four once funded-loan events were feeding the platforms. The funnel fixes, the win-back, and the ASO gains are durable and keep working without active media. The paid efficiency needs ongoing optimisation — creative, intent keywords, and continuous reseeding of the funded-borrower lookalike — to hold as auctions and the borrower mix shift.

Sources

- AppsFlyer — App Marketing Performance Index — Benchmarks showing how widely install quality and downstream conversion vary by channel and optimisation event

- Adjust — Mobile Measurement Blog — Guidance on in-app event instrumentation and optimising to deep funnel events

- Google Ads — App Campaigns Help — Official App Campaigns setup, event optimisation, and high-intent targeting documentation

- RBI — Master Directions (Digital Lending) — Primary source on India digital-lending, KYC, and consent requirements

- AppsFlyer — Fintech App Marketing Resources — Fintech-specific benchmarks on acquisition cost and deep-funnel conversion

- Think with Google — App Marketing Insights — Google research on intent-led acquisition and value-based bidding

- AppTweak — ASO Research Blog — Independent ASO benchmarks for keyword indexing and category-rank dynamics

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy