How Spotify Grew: A Personalisation & Freemium Teardown

Spotify grew from a regional European startup into a service with hundreds of millions of monthly active users and hundreds of millions of paying subscribers — and it did it with a compounding system, not a single hack. This is a teardown of the freemium funnel, the personalisation engine, the Wrapped content loop and the localisation playbook, with the transferable lesson for your own app at the end of every section.

What did Spotify's growth actually look like?

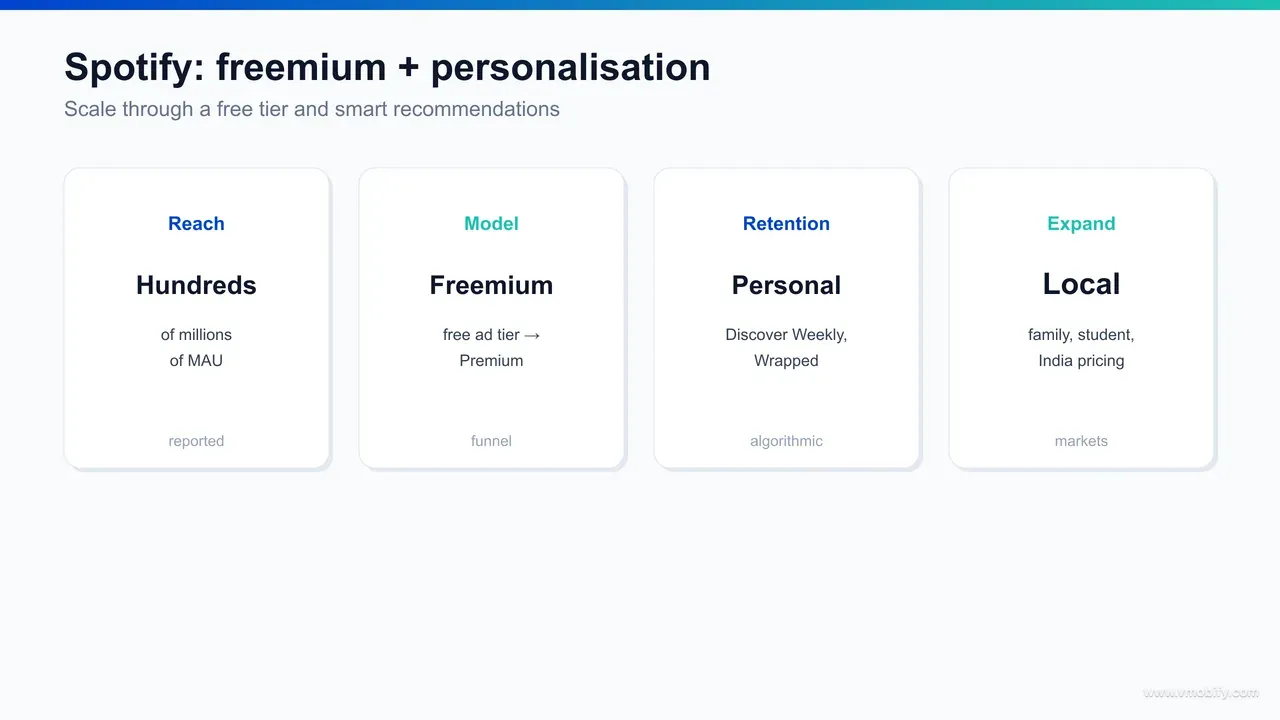

Spotify grew from a regional European music startup into a global service with hundreds of millions of monthly active users and hundreds of millions of paying Premium subscribers — and the striking part is that this was not built on a single growth hack but on a compounding system in which a free tier, a personalisation engine, a content loop and disciplined localisation each fed the next. The headline numbers — reported in the hundreds of millions on both the monthly-active and paid-subscriber lines — are widely cited in Spotify's own quarterly disclosures and in the music-industry press, and they describe a curve that kept climbing long after most consumer apps would have plateaued.

It helps to be precise about what those figures are. As tracked across years of reporting in Music Business Worldwide and the subscriber tallies in Billboard's industry coverage, Spotify's monthly active user (MAU) base and its Premium subscriber base have both climbed into the hundreds of millions, with the free tier consistently larger than the paid one. We are deliberately not inventing a more granular quarter-by-quarter breakdown here, because the shape matters more than the decimal: a service that grows a vast free audience and steadily converts a large minority of it to paid is describing a funnel, not a fluke.

The choice of metric is itself instructive. Spotify has long reported MAU and Premium subscribers as twin headline numbers, and the relationship between them is the whole story — the free base is the reservoir, the subscriber base is what gets pumped out of it, and the conversion rate between the two is the lever the company has optimised for over a decade. That is a fundamentally different growth philosophy from "spend more to acquire more paid users", and it is why this teardown sits in the retention category rather than the acquisition one.

Why does one streaming app deserve a full teardown? Because the primitives underneath it — a free tier that forms a habit, a recommendation feed that earns the return visit, a once-a-year content moment that markets the product for free, and a pricing ladder tuned per market — are available to almost any consumer app, and most teams assemble them badly. Spotify is the clearest worked example of the same components arranged into a loop that compounds. Across our 300+ apps managed since 2013, the question we hear most from founders is "how do we get users to keep coming back without burning the acquisition budget?" — and Spotify is the answer drawn at scale.

The rest of this teardown works through the system one layer at a time, and every section ends with the transferable lesson — the part you can take back to your own roadmap. Treat the numbers above as the why; the sections below are the how.

How does freemium convert free listeners into Premium subscribers?

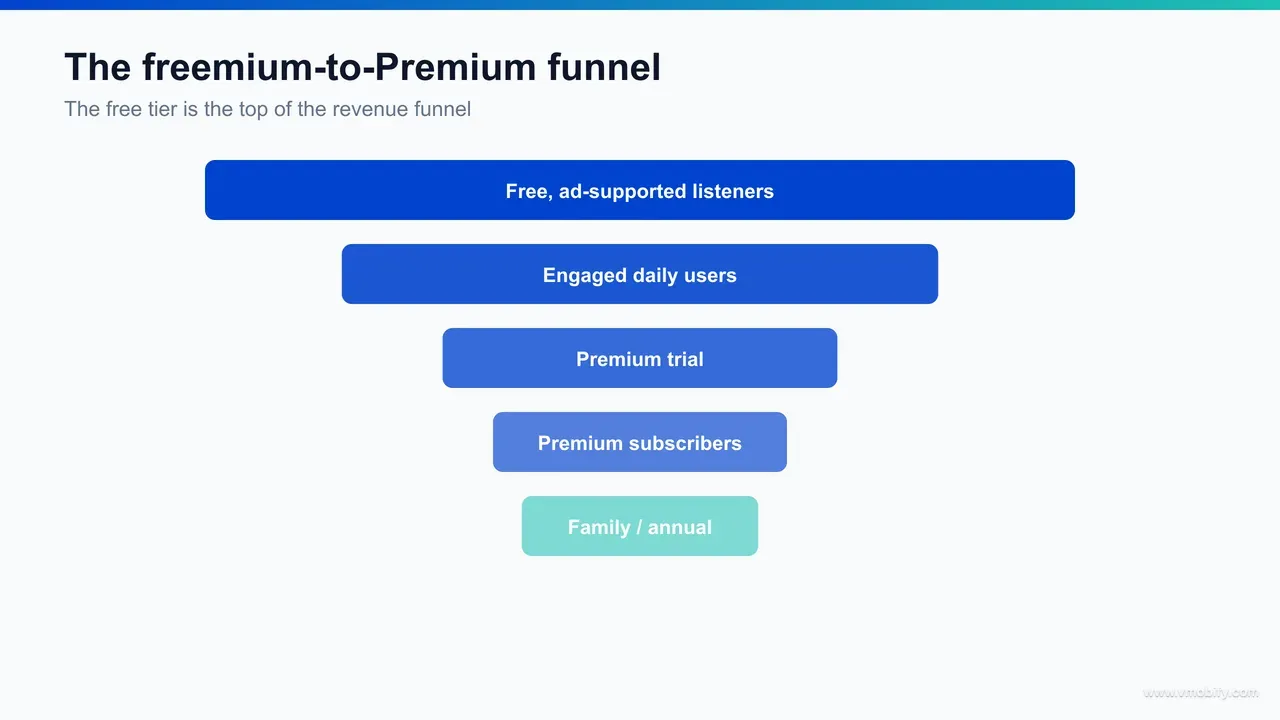

Freemium converts because the free, ad-supported tier is genuinely useful enough to build a daily listening habit at near-zero acquisition cost, and a retained listener who already opens the app every day is a far cheaper and easier sell on Premium than a stranger reached through paid media. The free tier is not a crippled demo designed to frustrate people into paying; it is a complete product whose deliberate frictions — ads between tracks, shuffle-led playback on mobile in the classic model, limited skips — are mildly annoying without being prohibitive. That balance is the entire design.

The logic is sequential. A listener arrives, often through word of mouth or a shared playlist link, and uses the free tier for nothing. Over weeks the app accumulates their taste data and becomes the default place they listen — the habit forms. Only then does the upsell land, and it lands on someone who already values the product daily. Selling a £/$ subscription to a person who opens your app every morning is a categorically easier conversion than selling to a cold prospect, which is why retention sits upstream of monetisation rather than beside it. As the product-led growth case studies collected by Lenny's Newsletter repeatedly show, the free tier's job is to manufacture the habit; the paid tier's job is to remove friction from a habit that already exists.

The free tier also does double duty as an acquisition channel and a revenue line at once. Ad-supported listening is not pure cost — it earns advertising revenue that helps fund the catalogue, so even non-converting free users contribute. And every free user is a potential sharer: a free listener who sends a playlist link to a friend is a zero-cost acquisition event. This is the dynamic every team running paid user acquisition eventually learns to respect — organic, product-driven distribution scales in a way that auction-priced installs never will, because the marginal cost of the next word-of-mouth user trends toward zero while the marginal cost of the next paid install only rises.

Conversion itself is then engineered with trial offers, contextual prompts and the simple accumulated weight of friction. After enough mid-listen ad breaks, a £/$ monthly price to make them disappear reads as a fair trade rather than a paywall — because the value was already proven. The discipline is that the prompt to upgrade reflects real, felt friction the user wants gone, not an artificial wall thrown up to coerce. We dig into this structure in our work on retention-led monetisation, and Spotify is its canonical example.

The transferable lesson: build a free tier good enough to form the habit, because a user with no habit never converts. Then price your paid tier against friction the user genuinely wants removed, and time the upsell to land on people who already return daily — not on strangers who have not yet felt the value. Sell on top of a habit, never instead of one.

How does personalisation like Discover Weekly and Wrapped drive retention?

Personalisation drives retention because a feed tuned to your individual taste gives you a reason to return that no competitor with the same catalogue can replicate — the music is a commodity available everywhere, but a recommendation engine that knows you is not, and that switching cost is what keeps listeners loyal. Spotify's central strategic insight was that in a world where every service licenses broadly the same songs, the durable moat is not the catalogue but the layer of software that understands what each person wants to hear next.

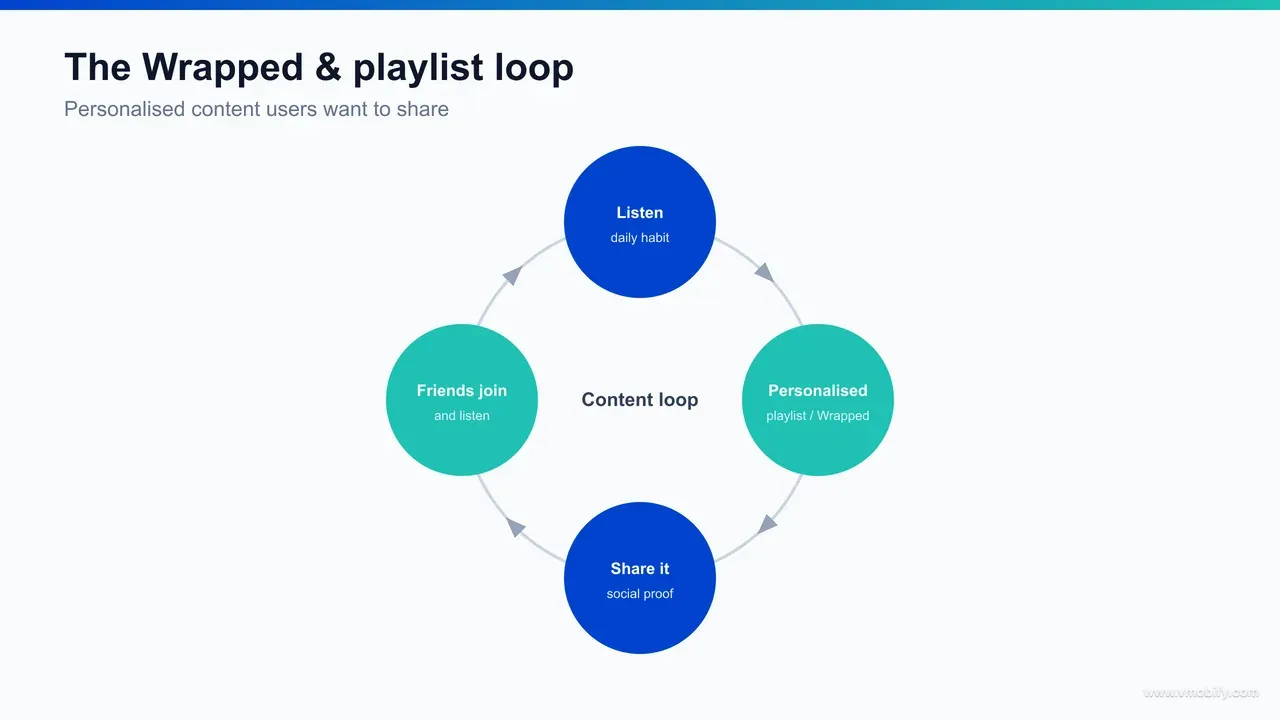

Discover Weekly is the flagship of this. A personalised playlist refreshed every Monday, built from each listener's history and the listening patterns of people with similar taste, it manufactures a recurring weekly appointment — a reason to open the app on a fixed cadence that has nothing to do with any specific release. The genius is the regular reset: like the weekly leaderboard in our Duolingo retention teardown, a predictable refresh creates a low-stakes habit loop ("it's Monday, my new playlist is ready") that pulls return visits without nagging. Around it Spotify has layered a whole family of algorithmic surfaces — Release Radar, Daily Mixes, the mood-and-moment Daylist, algorithmic radio and autoplay — each a different angle on the same engine.

The compounding effect is the part teams underrate. Every minute a listener spends in the app feeds the model, which makes the next recommendation better, which earns more listening, which sharpens the model further. This is a textbook data-driven growth loop: usage is not just an output, it is the input that improves the product for that exact user. The longer someone stays, the better Spotify gets at serving them specifically — and the more painful it becomes to start over on a rival service that knows nothing about them. Personalisation turns tenure into a moat.

Wrapped — the year-in-review that hands each listener a personalised summary of their year in music every December — is the same engine pointed at a different job. Where Discover Weekly drives weekly retention, Wrapped drives an annual emotional spike and, as the next section covers, an enormous viral moment. Both work because they reflect something true and specific about the individual: their actual taste, their actual year. As reporting in Spotify's own newsroom on these features makes clear, the personalisation is the product, not a feature bolted onto it. In our portfolio, the apps with the stickiest retention curves are almost always the ones where the experience visibly adapts to the individual rather than serving everyone the same screen.

The transferable lesson: find the part of your product that can be made meaningfully personal, and make returning to it a recurring appointment. A feed, a digest, a recommendation refreshed on a predictable cadence converts usage into a self-improving loop and builds a switching cost no competitor can copy by licensing the same content. Personalise the return visit, and tenure starts working for you. Our wider app retention strategy guide lays out how to instrument and design that loop from scratch.

How do family and student plans expand paying accounts?

Family and student plans expand the paying base by segmenting price to the willingness-to-pay of cohorts the standard individual plan would otherwise miss — a discounted student rate captures price-sensitive young users at the exact moment the habit forms, while a family plan raises revenue per household and builds in social accountability that lifts everyone's retention. Both are price-discrimination done in a way that grows the pie rather than cannibalising the full-price individual plan.

The student plan is a long-game acquisition play disguised as a discount. Students are price-sensitive but high-frequency listeners with decades of paying ahead of them, and capturing them cheaply while the habit is forming means converting them to the full-price plan later is almost automatic — they have already built years of taste data, playlists and switching cost inside the product. Discounting the entry price for a cohort that would not pay full freight, but would happily pay something, converts a non-customer into a paying one without touching what everyone else pays. As the streaming-economics coverage in Music Business Worldwide regularly notes, the student tier is among the most efficient subscriber-acquisition mechanisms a streaming service has.

The family plan does something subtler. By bundling several accounts under one household at a per-person price well below the individual rate, it lifts total revenue per household even as it lowers the per-seat price — a household paying for a family plan typically contributes more in absolute terms than a single individual subscription would. More importantly it manufactures retention through social entanglement: when several family members have their own libraries, playlists and recommendations inside one plan, cancelling becomes a household negotiation rather than a one-tap decision. The switching cost is now shared across people, which makes churn structurally harder. It is the same effect as the collaborative-playlist and household dynamic — more people invested in the same product means each is less likely to leave.

There is a defensive angle too. Family plans blunt the incentive to share a single login across a household — instead of one account quietly serving five people, the household pays for a plan that legitimises and monetises that exact behaviour. Converting account-sharing freeloading into a paid family plan is a quiet but meaningful expansion of the paid base. In our portfolio we have seen subscription apps unlock a second leg of growth simply by adding a tier matched to a cohort the single-price plan was silently excluding — students, households, teams — rather than by chasing more top-of-funnel installs.

The transferable lesson: a single price leaves money and users on the table at both ends. Segment your pricing to capture cohorts the standard plan misses — a discounted tier for the price-sensitive who would otherwise never pay, a bundled tier that raises revenue per account while building shared switching costs — and design each tier so it expands the base rather than discounting the users who would have paid full price anyway.

How did localisation and India pricing unlock emerging markets?

Localisation unlocked emerging markets because Spotify refused to export a single Western price and product everywhere — it tuned price, payment methods, catalogue and editorial to each market, and in price-sensitive geographies like India it priced aggressively low and offered flexible plans so that a subscription cost what the local market could actually bear. The principle is that global scale is not built by charging Stockholm prices in Mumbai; it is built by meeting each market where it is.

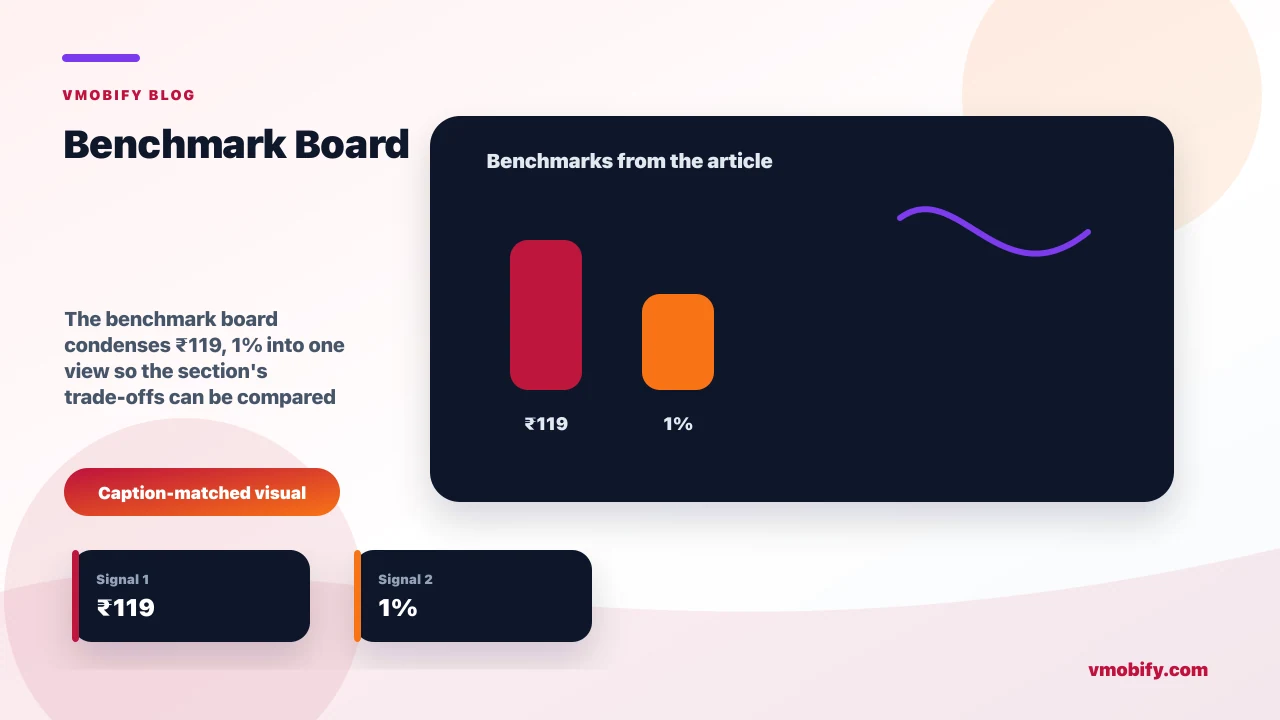

India is the clearest example. As widely reported when Spotify entered the market, the company launched with pricing far below its Western tiers — daily, weekly and monthly options at price points measured in tens of ₹ rather than hundreds, designed for a market where the willingness-to-pay curve and the prevailing data-and-payments reality are completely different. A monthly plan that costs a fraction of the US Premium price, plus micro-duration plans payable for a single day or week, meets a price-sensitive, mobile-first audience on its own terms. Charging ₹119 a month where the US charges several times that in dollars is not leaving money on the table — it is the only way to build a paying base of meaningful size in that market at all.

Pricing is only the visible half. Localisation also meant integrating the payment methods people actually use — in India, UPI and mobile wallets rather than the credit cards a Western default assumes — because a subscription a user cannot easily pay for is a subscription they will not buy, however cheap. It meant local-language editorial playlists, regional-music catalogues and home-screen content tuned to local taste, so the product felt native rather than imported. A listener in a new market who opens the app to find their own region's music front and centre is a listener who stays; one who finds only Western charts churns.

The strategic payoff is reach that compounds. Emerging markets are where the next several hundred million smartphone users are coming online, and a freemium product priced and built for those markets captures that growth in a way a premium-priced, English-only product never could. This is the same lesson every team scaling user acquisition into new geographies learns: the creative, the price and the onboarding all have to be localised, or your funnel leaks at the exact point a new market enters it. Across our 300+ apps managed since 2013, the single most common emerging-market mistake we see is exporting one global price and wondering why conversion collapses outside the home market.

The transferable lesson: do not export one price and one experience worldwide. Set price to local willingness-to-pay, support the payment rails people actually use, and localise the content and onboarding so the product feels native in each market. In price-sensitive, mobile-first geographies, an aggressively low local price that builds a large paying base beats a premium price that builds none.

What is transferable to your app — and what is not?

What transfers is the system and the sequencing behind it — a free tier that forms a habit, a personalisation loop that earns the return visit, a content loop that markets the product for free, and tiered local pricing that expands the base — but the surface specifics (a music catalogue, a December Wrapped campaign, a ₹119 price) do not transfer on their own, and copying them without the underlying logic usually fails. The mistake teams make is cloning Wrapped without first having a year of engagement worth wrapping.

Start with what genuinely transfers. The first principle is freemium as a habit-forming reservoir: a free tier whose job is to build a daily behaviour cheaply, with monetisation timed to land on already-retained users. The second is personalisation as a moat — the part of your product that can be made meaningfully individual, refreshed on a predictable cadence, so usage becomes a self-improving loop and tenure becomes a switching cost. The third is the content loop: the moment where users' own activity becomes shareable, identity-expressing content that does your acquisition for you. The fourth is price segmentation by cohort and by market. These four are portable to a wide range of consumer apps, and we run exactly this diagnosis with retention clients — instrument the engaged cohort, find the behaviour that predicts staying, and build the loop around it.

Now what does not transfer cleanly. The viral magnitude of Wrapped is partly a function of music being an unusually strong identity signal — people share their music taste more readily than, say, their spreadsheet usage. Your content loop has to be built on whatever identity or achievement signal your product genuinely produces; a forced "year in review" on a product nobody has an emotional relationship with reads as hollow. Likewise, Spotify's ability to invest in a world-class recommendation engine reflects scale, data and engineering depth a pre-product-market-fit app does not have — and trying to build the full apparatus before you have a core experience worth returning to is optimising on top of nothing.

The deepest non-transferable point is frequency and taste-dependence. Spotify's playbook rewards a high-frequency, taste-driven product where personalisation has rich signal to work with and daily use is natural. The more your product resembles that — content, media, social, learning — the more of this transfers wholesale. The further it sits from it — a low-frequency utility, a one-off transactional tool — the more you should take the discipline (free-to-habit, personalise the return, segment price) and leave the specific mechanics. The same caveat governs the Duolingo gamification playbook: the system is general, but its fit depends on whether your product earns frequent use.

The transferable lesson: take the method, not the motifs. Build a habit-forming free tier, a personalised return-visit loop and a content loop on top of a real identity or achievement signal — and adapt each to your product's actual frequency and data, rather than cloning a music app's surface and hoping the magic comes with it. The teams that succeed adapt the system; the ones that fail copy the screenshots.

What are the limits and risks of copying this playbook?

The biggest limit is fit — the playbook assumes a high-frequency, taste-rich product, and it strains on low-frequency or thin-data apps — and the biggest risks are brutal content economics that can crush margins, a free tier so generous nobody converts, personalisation that narrows into a filter bubble, and a viral moment that cannot be manufactured on demand. Spotify's system is powerful precisely because it fits its product and its market; transplanted carelessly, each component has a failure mode.

The margin risk is the one founders most underestimate. Spotify operates in a business where the cost of goods — music licensing and royalties paid to rights holders — consumes the majority of revenue, which is why even at enormous scale the model has historically run on thin margins. The transferable warning is that freemium only works if the marginal cost of serving a free user is low enough that the free base is not a bottomless cost centre. If every free user costs you real money to serve and few convert, the funnel that built Spotify will instead bleed your runway. Model your free-tier unit economics before you fall in love with the funnel.

The second risk is the generosity dial. A free tier good enough to form a habit but not so good that nobody upgrades is a genuinely hard balance, and erring either way is fatal: too crippled and the habit never forms, too generous and the habit forms but never pays. Spotify spent years tuning exactly which frictions (ads, shuffle, skip limits) sit on the free tier, and getting that calibration wrong is one of the most common ways freemium products quietly fail. Treat the free/paid boundary as a continuously-tuned experiment, not a one-time decision — the discipline behind sustainable monetisation generally.

The third risk lives inside personalisation itself. An engine optimised purely for "more listening" can narrow a user into a repetitive loop, starve discovery, and disadvantage smaller or newer creators who the algorithm never surfaces — a filter-bubble dynamic that draws real criticism in music as it does in every recommendation-driven product. Personalisation that optimises only the short-term engagement metric can quietly erode the long-term value and trust that retention actually depends on, the same metric-tunnel-vision trap any team faces when a single number becomes the target. The defence is to measure personalisation against long-run retention and satisfaction, not only against minutes-listened today.

Finally, the viral content loop is not a tap you can open at will. Wrapped's annual dominance is the product of years of brand-building, a genuinely strong identity signal and relentless format refinement — a team that ships a "year in review" expecting instant virality, on a product users have no emotional relationship with, will be disappointed. In our portfolio we have repeatedly seen content-loop attempts fall flat not because the mechanic was wrong but because there was no underlying engagement or identity worth sharing. The loop amplifies value that already exists; it cannot conjure it.

The transferable lesson: pressure-test fit and economics before you build. Confirm your free-tier marginal cost is survivable, tune the free/paid boundary as a live experiment, measure personalisation against long-run value rather than only engagement, and remember that a content loop amplifies real value but cannot create it. Used on the right product with honest economics, this playbook compounds; used on the wrong one, each component becomes a liability.

How do you apply one Spotify lesson this quarter?

Pick one lesson and ship it properly rather than rebuilding the whole system at once: identify the single behaviour that predicts whether your users stay, wrap it in one personalised return-visit loop refreshed on a predictable cadence, and measure the result against your week-four retention cohort — not against installs or same-week opens. One well-executed loop beats four half-built Spotify features every time.

Here is a concrete quarter-long sequence you can actually run:

- Weeks 1-2 — find your retention-predicting behaviour: instrument your engaged cohort and isolate the one repeated action that most separates retained users from churned ones. For Spotify it is listening sessions; for your app it is something specific you have to find in the data, not guess. If you cannot answer this, fixing your instrumentation is the first project.

- Weeks 3-4 — make a free tier that forms the habit: audit whether your free or trial experience is good enough to build that behaviour, and whether your frictions sit in the right place — annoying enough to motivate upgrade, light enough to let the habit form. Tune the free/paid boundary deliberately rather than inheriting a default.

- Weeks 5-8 — build one personalised return-visit loop: a weekly digest, a personalised feed, a recommendation refreshed on a fixed cadence — whatever makes returning an appointment tied to the user's own taste or progress. The predictable refresh is the mechanic; the personalisation is the moat. Ship one, not five.

- Weeks 9-10 — design one shareable artefact: find the moment where a user's own activity can become identity-expressing content (a milestone, a summary, a result) and build that one artefact for the feed it will live in. Keep it honest — it has to reflect something the user is genuinely proud of.

- Weeks 11-12 — measure against retention, not vanity: read the week-four retention cohort for users exposed to the new loop versus a control, and check conversion among already-retained users rather than installs. Keep what lifts genuine return frequency and paid conversion; cut what only moved a same-week number.

The order matters. Most teams start at the flashy end — they clone a Wrapped-style campaign or a Discover Weekly clone in week one — and skip the analytics work that tells them which behaviour to reinforce. That is how you end up with a beautifully designed loop pointed at an action nobody values. Spotify's advantage was never the playlist; it was the discipline of knowing exactly which behaviour to deepen — listening — and building free-tier habit, personalisation and content loops all in service of it.

If you want help running that diagnosis — finding your retention-predicting behaviour, calibrating the free tier, designing the personalisation and content loops, and measuring them against cohorts rather than vanity metrics — that is exactly the work our team does. Across our 300+ apps managed since 2013, the highest-return retention project is almost always this one. Read our app retention strategy guide for the full framework, or talk to us directly about your app's freemium and personalisation loop.

Frequently Asked Questions

How did Spotify grow so fast?+

Spotify grew through a compounding system rather than a single hack: a free, ad-supported tier that builds a listening habit cheaply, deep personalisation (Discover Weekly, Wrapped) that earns return visits, shareable playlists and Wrapped that act as a viral content loop, and tiered local pricing that expands the base. The result is a base of hundreds of millions of monthly active users and hundreds of millions of paid subscribers.

How does Spotify make money from free users?+

The free tier earns advertising revenue between tracks, so non-converting listeners still contribute, and it doubles as an acquisition channel because free users share playlists. Its main job, though, is to form the habit so that retained listeners convert to Premium far more cheaply than cold prospects reached through paid media.

Why is Spotify personalisation so important?+

Because the music catalogue is a commodity available on every service, the durable moat is the software that knows your taste. Discover Weekly, Daylist and algorithmic radio refresh on a predictable cadence to manufacture return visits, and the longer you use Spotify the better it gets at serving you specifically, which builds a switching cost rivals cannot copy.

What is Spotify Wrapped and why does it work?+

Wrapped is the annual year-in-review that packages each listener’s year of data into designed-to-be-shared cards. It works because music taste is a strong identity signal, so people share it readily — turning a year of private listening into a viral content loop that drives new installs and reactivations at almost no media cost.

How did Spotify price its plans in India?+

Spotify entered India with pricing far below its Western tiers — monthly plans in the tens of ₹ plus flexible daily and weekly micro-plans — and integrated local payment methods like UPI and wallets. Meeting a price-sensitive, mobile-first market at its own willingness-to-pay was the only way to build a meaningful paying base there.

Can any app copy the Spotify playbook?+

The method transfers — a habit-forming free tier, a personalised return-visit loop, a content loop and segmented local pricing — but the fit depends on frequency and data. High-frequency, taste-rich products (media, content, social, learning) gain the most; low-frequency utilities should take the discipline but leave the specific mechanics, and everyone must model free-tier margins first.

What does Vmobify do to help with retention and freemium?+

Our team instruments your engaged cohort to find the behaviour that predicts retention, then helps calibrate the free/paid boundary, design the personalisation and content loops, and measure them against week-four cohorts rather than vanity metrics. See /services/monetization and /services/user-acquisition, plus our guides on app retention strategy and growth loops.

Sources

- Lenny's Newsletter — product-led growth and freemium case studies — Freemium conversion logic and habit-first product strategy

- Music Business Worldwide — Spotify subscriber and streaming economics — MAU and Premium subscriber trajectory, student-tier and pricing economics

- Billboard Pro — music industry and streaming analysis — Subscriber tallies and the annual Wrapped social moment

- Spotify Newsroom — official product announcements — First-party context on Discover Weekly, Wrapped and personalisation features

- Spotify Investor Relations — quarterly results — Reported monthly active user and Premium subscriber figures

- AppsFlyer — State of App Marketing and Performance Index — Acquisition-cost benchmarks that make the freemium case

- Nielsen Norman Group — UX research — Evidence base for personalisation, friction and return-visit UX

About the author

Amol Pomane — Founder, Vmobify

Amol leads Vmobify, a mobile app growth agency that has driven 30M+ downloads and ranked 54K+ keywords across 300+ apps since 2013. He writes about ASO, paid user acquisition, retention, and the operational reality of scaling mobile apps in India and global markets.

Free Growth Audit

See exactly how to scale your app with 13+ years of expertise behind you.

Get My Strategy